CoreCivic, Inc. (NYSE:CXW) recently delivered better than expected quarterly revenue, and noted new contracts signed in the year 2023. I believe that further partnerships with federal agencies, know-how accumulated for close to 40 years, and further investment in public infrastructure could accelerate future net sales growth. There are obvious risks from changes in the public regulation or lower government funding, however the company appears undervalued.

Business Model

Formed in 1983, CoreCivic is a diversified entity that offers government solutions through three segments: CoreCivic Safety, CoreCivic Community, and CoreCivic Properties. With 40 years of experience, it is the largest owner of correctional facilities in the United States.

Through educational and rehabilitation programs, medical services, and employment programs, the company seeks to reduce recidivism as well as to facilitate the successful reintegration of offenders into society.

CoreCivic operates close to 44 correctional and detention facilities, either as direct owner or through long-term leases, including third-party facilities managed by the company. In addition, it integrates the operating results of TransCor, a government transportation subsidiary, in this segment.

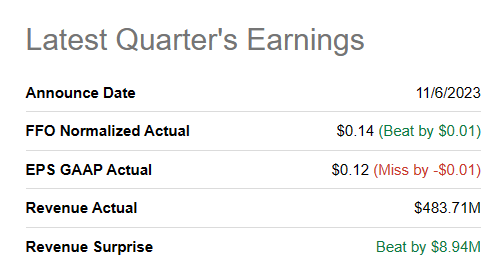

The company also manages 23 residential reentry centers. This segment also encompasses the operational results of the company’s electronic monitoring and case management service. It owns and leases 8 real estate properties to government agencies. Each segment contributes to its operational diversification and satisfaction of various needs in the correctional system. I believe that it is the right time to have a look at the company not only because of its recent quarterly earnings surprises, but because of new contracts signed in 2023. The company reported quarterly revenue more than expected, close to $483 million, and EPS GAAP of $0.12 per share.

Source: SA

Balance Sheet

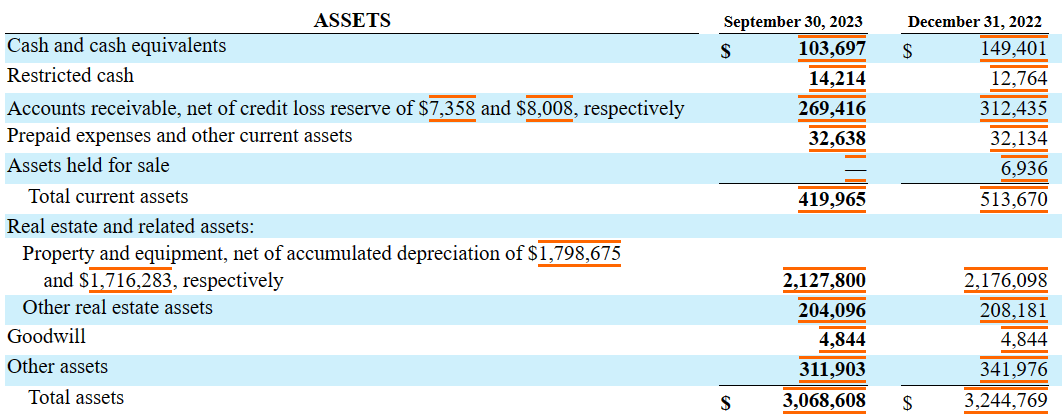

As of September 30, 2023, the company noted cash of $103 million, restricted cash close to $14 million, accounts receivable of worth $269 million, and prepaid expenses and other current assets of about $32 million. Total current assets are equal to $419 million, which are larger than the current liabilities. I do not really see a liquidity crisis here.

Property and equipment, which is the largest asset, stands at $2.127 billion. Total assets were equal to $3.068 billion, and the asset/liability ratio is above 1x, so I believe that the balance sheet is stable.

Source: 10-Q

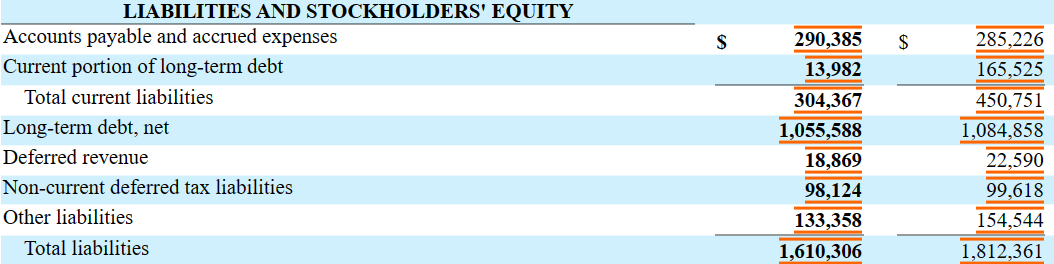

The total amount of debt is not small, so I believe that investors may welcome some research about the interest rates being paid. Long-term debt stands at close to $1.055 billion, with the current portion of long-term debt close to $13 million. Other liabilities are non-current deferred tax liabilities worth $98 million and accounts payable and accrued expenses worth $290 million.

Source: 10-Q

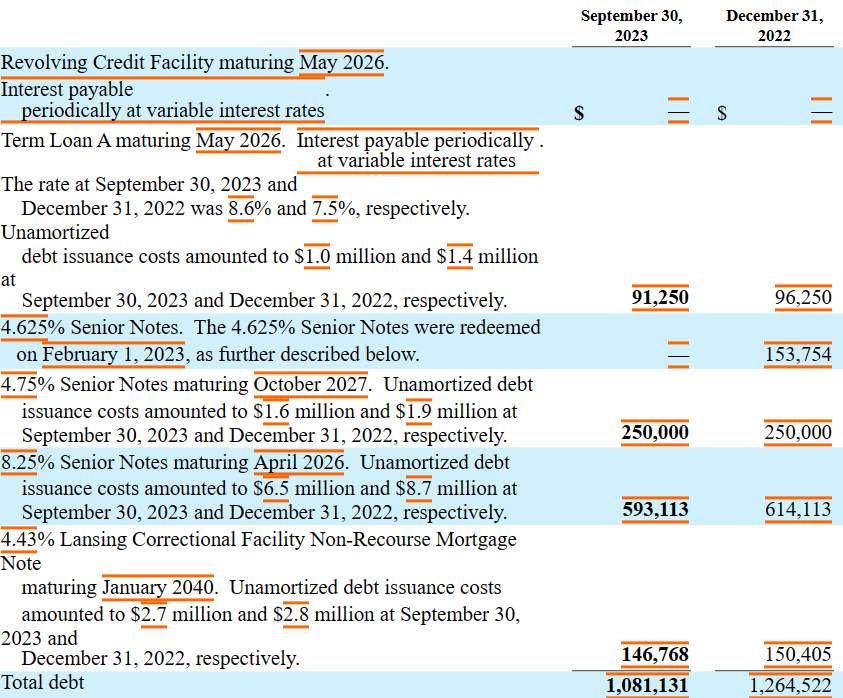

I am not really concerned about the total amount of debt because the company works for the government, which usually pays business providers. With that, it is worth mentioning the cost of debt to understand what could be the most reasonable WACC for my DCF. The company signed agreements, including 8.25% senior notes due 2026 and 4.75% senior notes due 2027. With these figures in mind, I believe that assuming a WACC around 4% and 10% would be conservative.

The indentures related to our 4.625% senior notes due 2023 (until their repayment and satisfaction on February 1, 2023), 8.25% senior notes due 2026, and 4.75% senior notes due 2027, collectively referred to herein as our senior notes, and the indentures related to our New Bank Credit Facility, together with our senior notes, our Credit Agreements, contain restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Source: 10-k

Source: 10-Q

Expectations Include Growing Net Sales Growth And Net Margin Growth

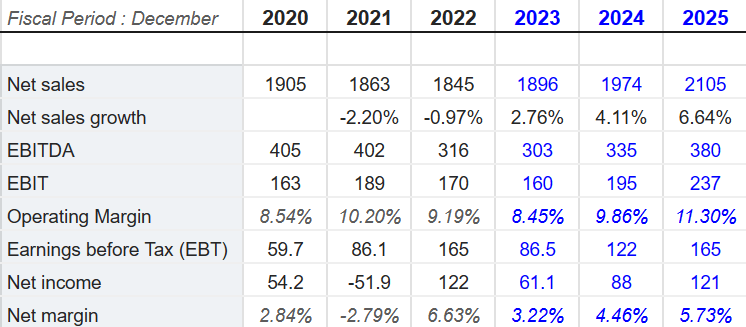

I believe that the expectations of other analysts are beneficial, and are worth having a look. Analysts are expecting net sales growth and net margin growth. 2025 net sales are expected to be close to $2.105 billion, with net sales growth of close to 6.7%, 2025 EBITDA of close to $380 million, and 2025 net income close to $121 million.

Source: S&P

Partnerships, Marketing, And Occupancy Increases Could Lead To Sales Growth

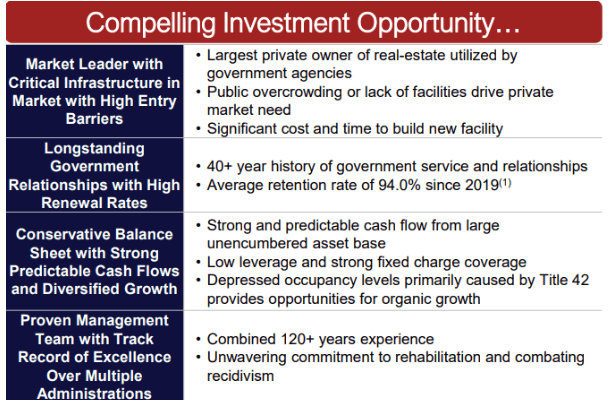

The company’s business strategy focuses on consolidating its position as one of the leading providers of correctional services in the United States. With a significant participation in private prison beds, the aim is to maximize the occupancy of existing facilities, including those currently inactive. Through the partnership development department, the company focuses on marketing services to government agencies at the federal, state, and local levels.

Given the number of years working with the government and the track record reported by the management team, I would expect net sales growth in the coming years. The following is a slide from a previous presentation given by management.

Source: IR Presentation

Additionally, the company is committed to innovation and expansion, exploring opportunities to develop properties and offer non-residential solutions. The interdepartmental approach encompasses management, residential reentry, and real estate services, adapting to changing market needs. With federal customers such as ICE, USMS, and BOP, which continue to be essential pillars of revenue, I believe that we can expect further business growth.

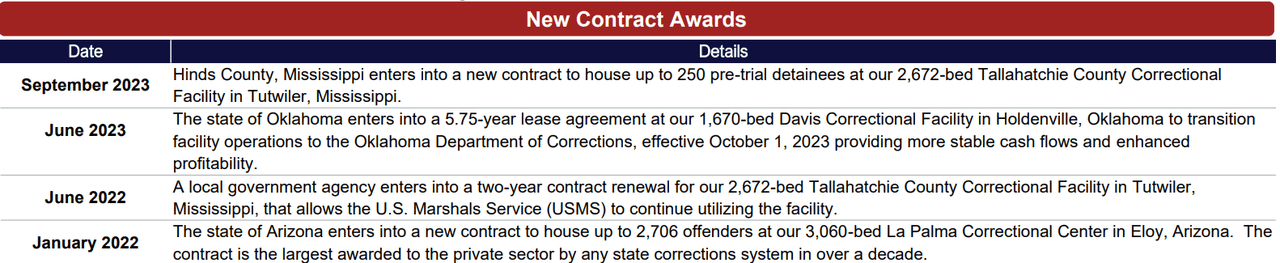

New Contracts Signed In 2023 And 2022 As Well As The Aging Infrastructure Crisis Will Most Likely Bring Net Sales Growth

Like many other infrastructures in the United States, America’s prisons seem to be old, and need new capital expenditures. Given their expertise in the sector, CoreCivic may enjoy a beneficial time period in the coming years.

Source: IR Presentation

I also believe that the recent contracts to build facilities, lease agreements, and new agreements to renew facilities in Mississippi and Oklahoma will most likely bring net sales growth. Additionally, given the skills of management while dealing with public administrations all over the United States, I would expect new agreements in the future. We are talking about more than 40 years of experience in the industry.

Source: IR Presentation

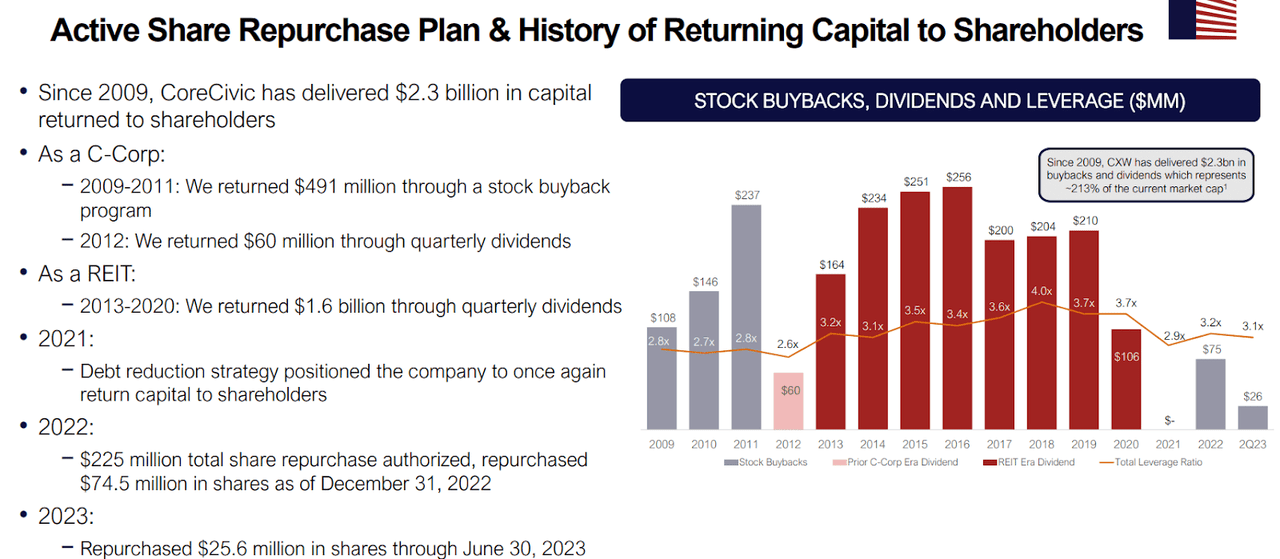

The Share Repurchase Plan May Also Bring Demand For The Stock

It is worth noting the repurchase plan and the number of purchases made in 2023 and 2022. I believe that further reduction in the share count and demand from other investors could lead to stock price increases.

Source: IR Presentation

Given My Previous Assumptions And Previous Cash Flow Statements, I Designed A DCF Model

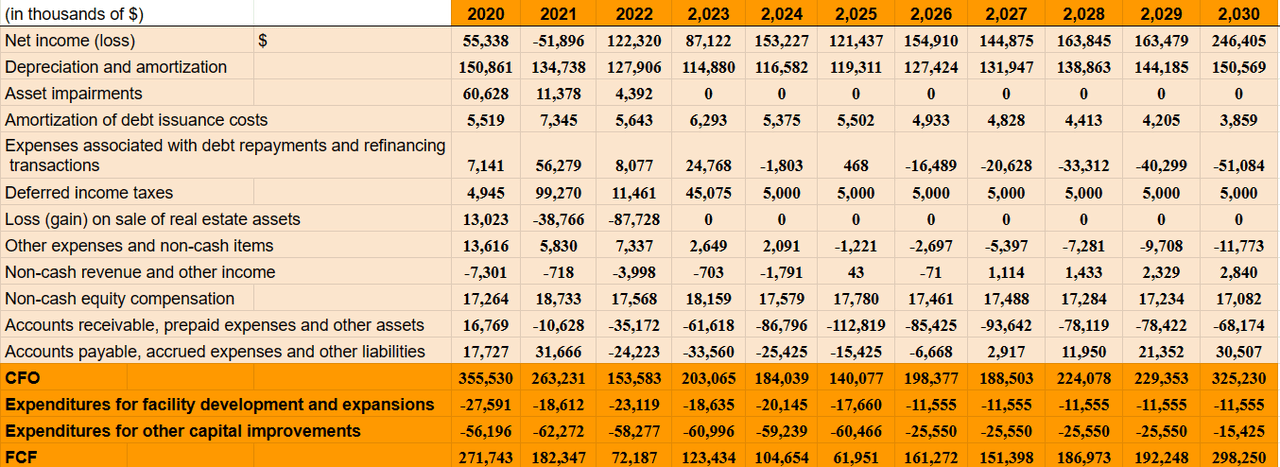

Given the previous assumptions, I included net sales growth from 2023 to 2030 and a new income / sales of around 4% and 6%. Under my forecasts, 2030 net income would be close to $246 million, with depreciation and amortization close to $150 million and no asset impairments. Let’s keep in mind that the company included asset impairments for the calculation of the net income, which I do not believe is a recurrent activity of CoreCivic.

Source: DCF

I also included transactions of about -$52 million, with deferred income taxes close to $5 million, non-cash revenue and other income of $2 million, and changes in accounts payable, accrued expenses, and other liabilities close to $30 million. Finally, with 2030 CFO of $325 million, 2030 expenditures for facility development and expansions of -$12 million, and expenditures for other capital improvements close to -$16 million, 2030 FCF would be about $298 million.

Source: DCF

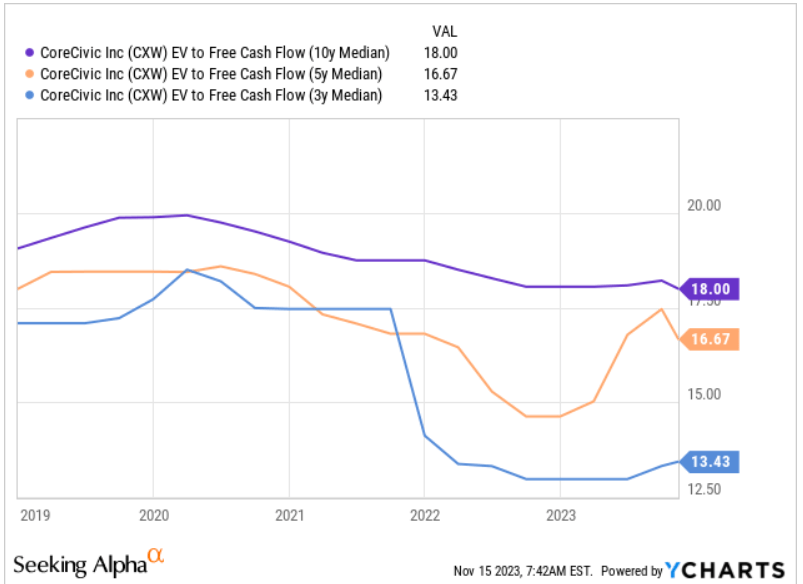

For the assessment of the exit multiple, I took into account previous trading multiples, which were close to 13x and 18x FCF. Additionally, the sector median includes an EV/EBITDA of 12x and Price /Cash Flow of 11x. With these figures, I believe that an exit multiple between 11.5x and 14.5x would make sense.

Source: Ycharts Source: SA

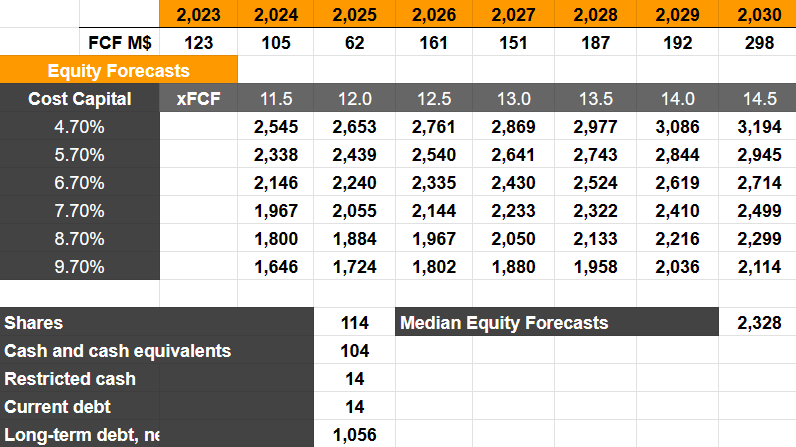

Assuming FCF between $62 million and $298 million from 2025 to 2030 and a cost of capital of about 4.7% and 9.7%, the implied equity forecasts would be close to $1.6 billion and $3.1 billion. The median forecasts stood at about $2.3 billion.

Source: Ycharts Source: DCF

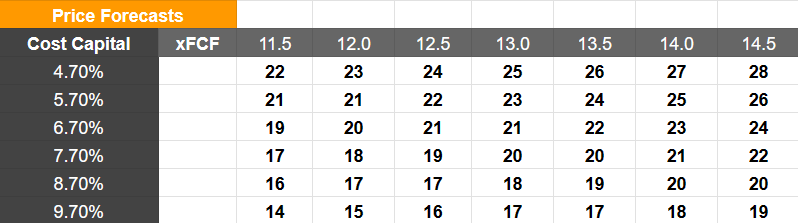

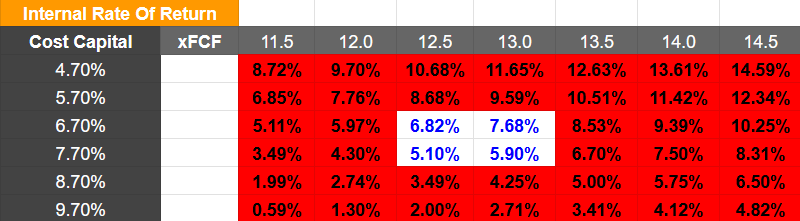

If we divide by the share count, the implied price forecast would range between $14 and $28 per share, with a median price close to $19 and $21 per share. Additionally, we would be talking about an IRR between 0.5% and 14% as well as a median internal rate of return of 5%-7%. In the light of these results, I think that the company appears quite undervalued.

Source: DCF Source: DCF

Risks

The company’s cash flow is subject to the timely receipt of funds from contracting government entities. Lack of sufficient allocations could lead to termination or delay in payment of contracts. Historically, during government shutdowns, the company is expected to fulfill contracts without immediate payment. Delays or termination of contracts could adversely affect cash flow and financial condition.

Pressures to reduce expenses can lead to the renegotiation of contractual rates or a decrease in population in facilities, affecting the renewal of contracts. Uncertainty in the federal budget and debt limits as well as government shutdowns may have adverse impacts on liquidity and financial results.

Any reductions in government spending in an effort to reduce the U.S. federal deficit could result in a reduction in the utilization of our services or additional pricing pressure. Further, there is ongoing uncertainty regarding the federal budget and federal spending levels, including the possible impacts of a failure to increase the “debt ceiling.” Any U.S. government default on its debt could have broad macroeconomic effects that could, among other things, raise our borrowing costs. Source: 10-k

Competitors

The company faces competition in the market in which it operates, from other private companies, such as The GEO Group, Inc. (GEO) and Management and Training Corporation, and government agencies. Competition is based on bed availability, costs, quality of services, design and management expertise, and reputation. It also competes with small local businesses, and could face new competitors in the future. Competitive pressure can affect the occupancy of the facilities, impacting operating income. Factors such as demand for beds, economic conditions, and demographics also influence income.

My Opinion

CoreCivic, with 40 years of experience, is a leader in correctional services in the US with fresh contracts signed in 2023. Its strong track record and partnerships with federal agencies will most likely lead to further net sales growth and FCF margin. Besides, I believe that further investment in public infrastructure could accelerate the company’s business model. Despite risks such as reliance on government funding and competition, I believe that the company remains undervalued.

Read the full article here