Investment Thesis

In my prior article on Berry Global (NYSE:BERY), I emphasized that the core of the thesis lies in observing consistent positive changes quarter after quarter. This shift marks a departure from the prior capital allocation strategies that eroded value by incurring substantial debt and engaging in acquisitions that lacked long-term sustainability.

In this article, we will scrutinize whether the company remains on the right trajectory and examine the ongoing efforts aimed at positioning itself as one of the premier companies in the sector, which could bring an improvement in market perception and consequently an improvement in valuation.

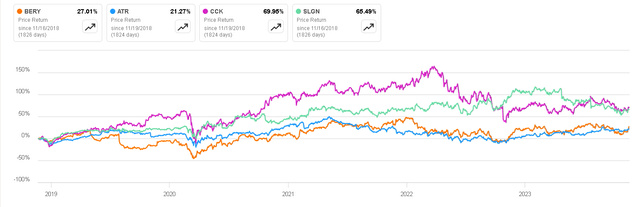

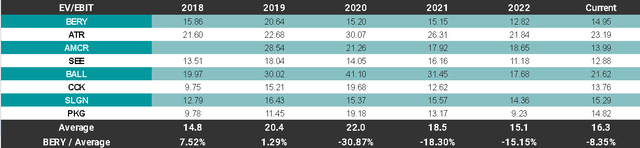

BERY’s performance vs Peers (Seeking Alpha)

FY2023 Results

On November 16, the company announced its Full Year 2023 results, in which the following points can be highlighted:

- Revenues: $12.6 billion vs $14.5 billion during FY2022, representing a year-over-year decrease of 12.6%.

Despite a significant decrease, it was already anticipated due to the prevailing disinflation and the reduction in buying volume, leading to a downward price adjustment to compensate for these effects. While the sales volume also experienced a decline during the year, this reduction was modest at 3%. In preceding years, the company achieved more substantial growth, primarily attributed to the acquisitions they made, but with new management and the entry of activist investors, the priority now is to reduce debt and return capital to shareholders, as was stated during the last conference call:

We expect to prioritize repayment of debt to meet our leverage target commitment, along with further share repurchases. We continue to believe our shares are undervalued, and our repurchases reflect our confidence in the outlook of our business and long-term strategy.

- EBITDA: $1.90 billion vs $2.10 billion during past year. This represents a margin of 14.98%, marginally higher than last year

Although still below the company’s historical average, this improvement is attributed to ongoing efforts to enhance the cost structure. Notably, the slight increase in margins is particularly noteworthy, given the necessary reduction in sales costs to align with lower raw material prices.

- EPS: $4.95 vs $5.77 last year. Represents a YoY decrease of 14% and a decrease in Net Income margins, going from 5.3% to the current 4.8%.

- Free Cash Flow: $926M vs 876M during last year. This represents a Free Cash Flow margin of 7% vs. 6% last year.

Free Cash Flow seemed to me to be one of the most positive points, since it greatly exceeded what was provided during the previous quarter, where they expected to end the year with $800M of FCF. This positive performance can be attributed to effective working capital management by the board, since they successfully reduced accounts receivable and managed inventories efficiently throughout the year.

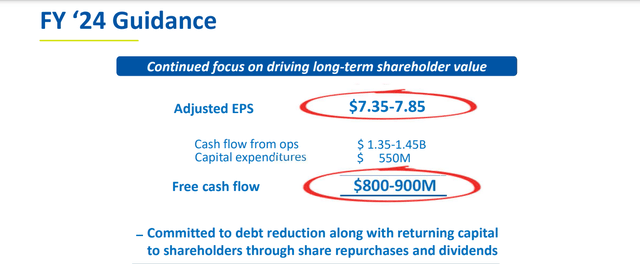

We expect free cash flow to be $800 million assuming cash flow from operations of $1.45 billion, less capital expenditures of $650 million.

Utilizing the generated cash, the company executed a share repurchase, retiring 7.4% of outstanding shares at an expense of $600 million. Additionally, $127 million was allocated towards dividends, reflecting a 10% increase in the quarterly payment, resulting in a current dividend yield of approximately 1.6%.

Additionally, the company reduced its net debt by more than $700M, which maintains a Net Debt/EBITDA ratio of around 3.9x and interest expenses represented 33% of FCF, a notable improvement from the historical average of 50% since 2013, addressing a serious problem the company had in this regard.

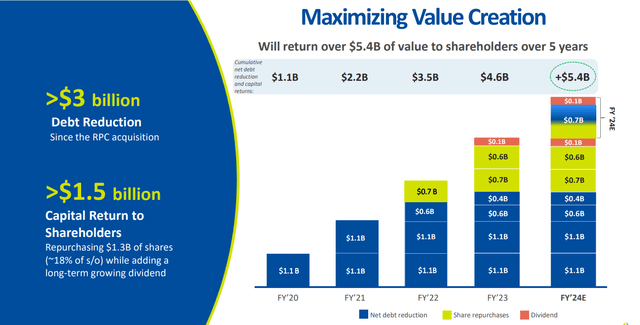

Berry Global

Looking forward, the company anticipates generating between $800 and $900 million in Free Cash Flow this year. The entirety of this cash flow is earmarked for strategic purposes, including share repurchases, dividend payments, and debt reduction. This commitment to shareholder remuneration without increasing leverage aligns with the imperative changes sought for Berry Global.

This proactive approach could potentially narrow the valuation gap with its peers, as outlined in the forthcoming analysis. Additionally, the company expects adjusted EPS to reach approximately $7.6, a slight increase from the reported $7.4 adjusted EPS this year. This projection would place the company at a forward Price-to-Earnings Ratio of 8x.

Berry Global

New CEO

Kevin Kwilinski has recently assumed the position of CEO at Berry Global, having been in the role for just 50 days. The recent conference call marked the first occasion for shareholders to hear his vision for the company’s future.

With over 30 years of experience in the packaging sector, Mr. Kwilinski began his career in 1992 at International Paper. Subsequently, he spent nearly 12 years at Graphic Packaging before being appointed CEO of Portola Packaging in 2009. His extensive experience in the sector and established reputation make him an ideal fit for Berry Global. Notably, his focus on generating value through organic growth and returning capital to shareholders aligns with the company’s strategic goals.

Through my first 50 days here at Berry, I’ve been working diligently with our team and Board to build upon Berry’s value-creating opportunities, by bringing new approaches and incremental focus to drive organic growth and process improvement led productivity gains.

Q4 Conference Call

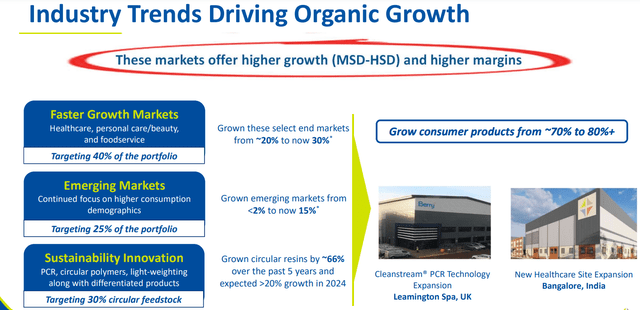

To achieve organic growth, management has identified key levers, capitalizing on the rapid expansion in the beauty and food delivery industry, along with the burgeoning growth of packaging solutions in emerging markets. While Berry Global currently holds a significant presence in North America and Europe, it has yet to fully harness the potential for growth in emerging markets, making this approach both reasonable and promising.

Moreover, the commitment to sustainable solutions remains a focal point in Berry Global’s market vision and supplier relationships. This includes initiatives such as light-weighting, discussed in a previous article, and the adoption of circular polymers. Circular polymers involve reusing or recycling the polymer in a closed-loop process, moving away from single-use disposal and aligning with the company’s commitment to sustainability.

The increasing demand for sustainable packaging solutions aligns with our design capabilities, in producing and sourcing recycled resins globally. Our leadership in these areas position us for higher growth opportunities.

Q4 Conference Call

Berry Global

In summary, a change in CEO appears to bring a breath of fresh air to the company and has the potential to fortify the shift in business culture. This includes the implementation of refined policies for capital allocation and a steadfast focus on sustaining growth.

Valuation

In the following table, the disparity in valuation between Berry Global and several players in the packaging sector is illustrated. Typically, the average EV/EBIT ratio hovers around 17x, with BERY maintaining an average of 15.8x. Currently, BERY is at 15x, which appears quite reasonable. Notably, the improvement in capital allocation has effectively closed the gap observed over the past year when the company traded at less than 13x EBIT.

Author’s Representation

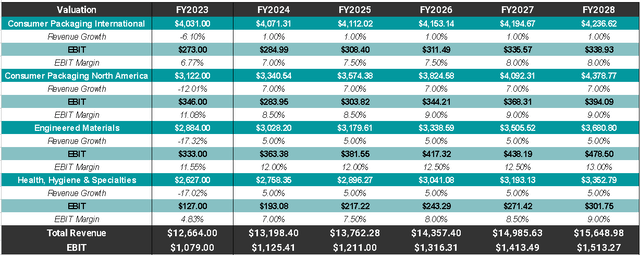

Moving on to the valuation, I aim to project the growth and margins of each segment individually, since by breaking down past growth I will be able to have a more reliable estimate of where revenues and margins could go.

- Consumer Packaging International exhibited the most resilient revenue performance during the year, albeit historically presenting a modest growth rate of around 1%, accompanied by EBIT margins hovering around 8%.

- Consumer Packaging North America experienced robust growth between 8% and 9% before the challenging FY2022, where revenues declined by 12%. Traditionally, its margins have been around 8%, with a notable trend of rising to 11% during crisis years, as observed in 2020 and 2022. I anticipate these margins will normalize in the coming years.

- Engineered Materials segment has primarily expanded through acquisitions, with organic growth typically around 5%. While its margins used to be 13%, I believe there is potential for recovery.

- Health, Hygiene & Specialties segment, which grew at rates of 5% pre-2022, has volatile margins, ranging from 7% to 16%. For the sake of consistency, I will consider the average of the last 7 years.

Author’s Representation

This projection implies an annual growth in total revenues of 4%, coupled with EBIT margins expected to revert to the nearly 10% levels sustained between 2016 and 2021.

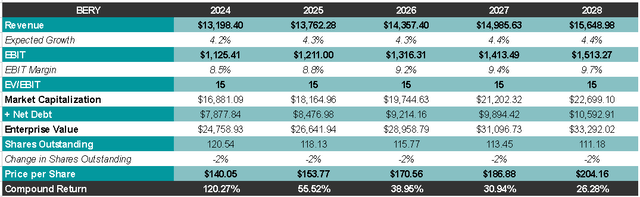

Applying the previously mentioned average multiple of 15x EV/EBIT to the estimated $1.5 billion EBIT, which aligns with the current multiple, suggests a Market Cap of $22 billion within 5 years. This equates to a per-share value of $200 USD or an annual return ranging between 20% and 25%. This anticipated return is attributed to the enhancement of margins, a moderate yet consistent growth, and the reduction of outstanding shares.

Author’s Representation

Final Thoughts

The thesis remains robust, and the positive transformation in the company is becoming increasingly evident.

Notably, there has been a shift away from issuing debt for acquisitions, resulting in a reduction of the leverage ratio, which has now dropped below 4x EBITDA for the first time in the last decade. The company continues to enhance its dividend, and shares are being repurchased at the opportune moment when the price is favorable. Coupled with an attractive valuation that promises good returns with low risk, Berry Global appears to be an excellent choice for portfolio stability.

Given these factors, I believe the company warrants a ‘buy’ rating, even following the modest price increase in the days subsequent to the annual report.

Read the full article here