Introduction

I seek new investment opportunities from my dividend growth portfolio. The information technology sector is attractive after it performed poorly in 2022 and recovered in 2023. Despite higher rates, we see these stocks being relatively resilient. Therefore, I am willing to add companies in the sector even if the forecast is for a prolonged period of higher rates. I will require an attractive valuation that suits the current business environment.

One exciting company in particular is Intuit (NASDAQ:INTU), which offers a suite of software solutions for the mass population and small businesses. The advantage here is that the company is answering a basic need that every person is dealing with- personal finance. Therefore, it may be more resilient during a harsher business environment as the need to have your finances in order increases.

Seeking Alpha’s company overview shows that:

Intuit provides financial management and compliance products and services for consumers, small businesses, self-employed, and accounting professionals in the United States, Canada, and internationally. The company operates in four segments: Small Business and self-employed, Consumer, Credit Karma, and ProTax. The Small Business & Self-Employed segment provides QuickBooks and Mailchimp services. The Consumer segment provides TurboTax income tax preparation products and services. The Credit Karma segment offers consumers a personal finance platform that provides personalized recommendations of home, auto, and personal loans, as well as credit cards and insurance products. The ProTax segment provides Lacerte, ProSeries, and ProFile.

Fundamentals

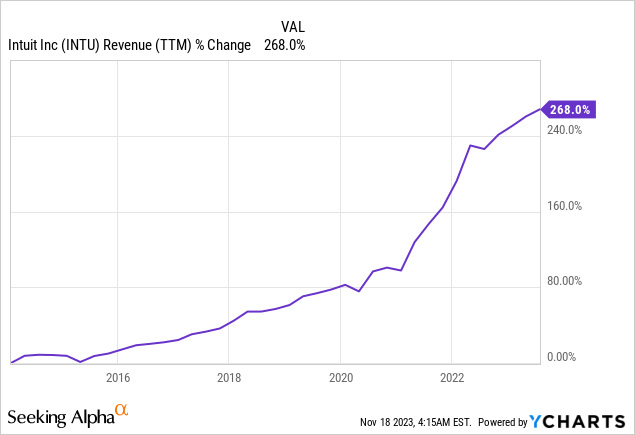

The revenues of Intuit have increased by 268% over the last decade. Intuit has been using a hybrid strategy combining aggressive acquisitions together with organic growth. It has created an ecosystem of services that support one another and make more customers to one another. In 2020, the company acquired Credit Karma and Mailchimp for $7.1B and 12B, respectively. It is now integrating them into its personal and business platforms. In the future, as seen on Seeking Alpha, the analyst consensus expects Intuit to keep growing sales at a high CAGR of ~12% in the medium term.

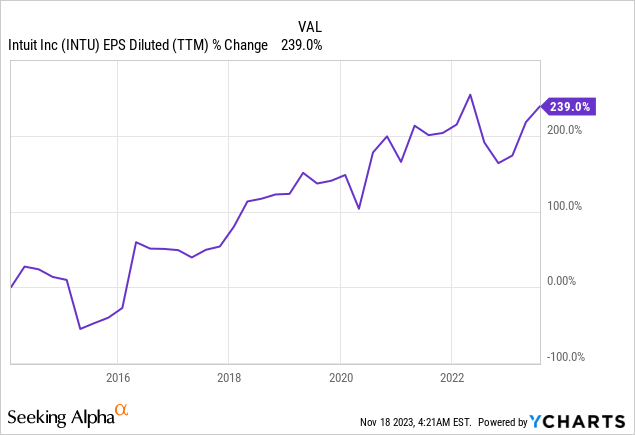

Intuit’s EPS (earnings per share) has grown slightly slower at 239% over that decade. The company’s EPS increased slowly despite a slight decrease in the company’s share count. The reason for that is the decrease in operating margin. The margin decreased from over 30% in 2014 to 22% in 2023. The decline in margins came following the 2020 acquisitions, and the company is working to lower costs as it integrates them and leverages synergies. In the medium term, as seen on Seeking Alpha, the analyst consensus expects Intuit to keep growing EPS at a healthy annual rate of ~14%.

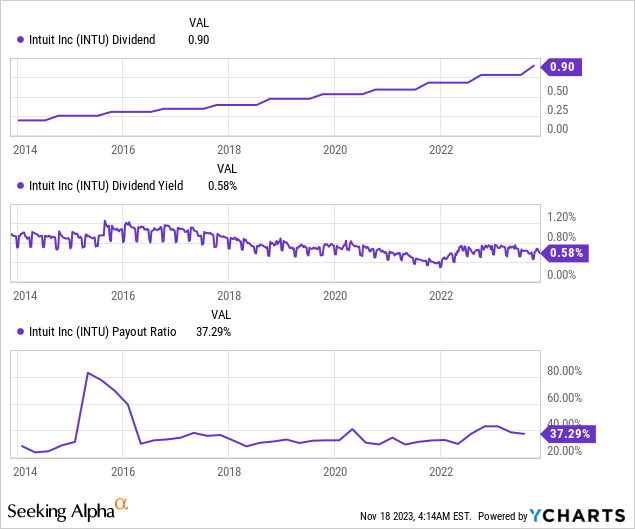

The company is a relatively new dividend-paying company. It started paying a dividend eleven years ago and has been increasing the annual payment yearly since then. The company offers what I believe to be a safe payment due to the low payout ratio staining at 37%. However, due to the current valuation and the low payout ratio, the dividend yield stands at 0.6%, which is low in the current environment. Since there is room for dividend growth, long-term investors may still consider Intuit for their portfolio.

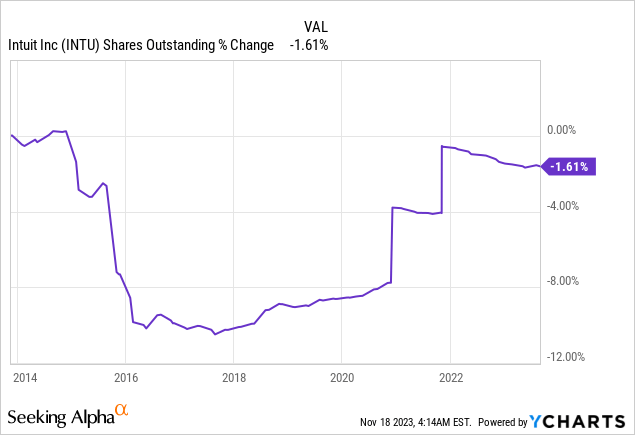

In addition to dividends, companies return capital to shareholders via buybacks. These share repurchase programs support EPS growth by reducing the number of shares. Over the last decade, Intuit has repurchased shares and decreased the share count by only 1.6%. The reason is that it used shares to acquire companies and pay employees. The fact that it maintained a stable share count is positive because it avoided shareholder dilution.

Valuation

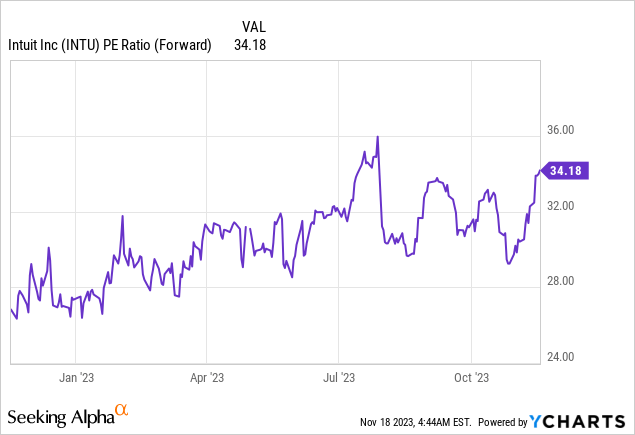

Intuit’s P/E (price to earnings) ratio stands at 34 when using the 2024 EPS forecast, which means that the shares are expensive. The current valuation is almost the highest we have seen over the last twelve months. Despite interest rates climbing, the premium has increased, and the company is now more expensive than most large-cap software companies such as Microsoft and Salesforce. Therefore, the shares do not look attractive at the moment.

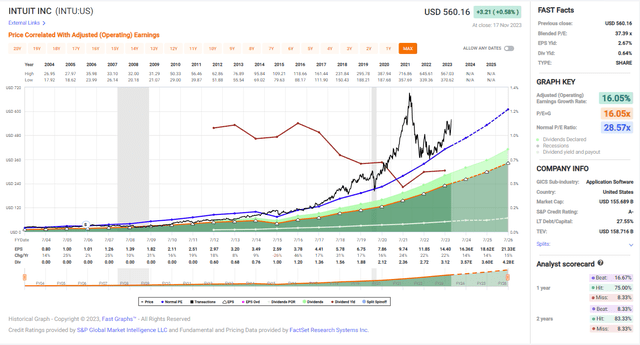

The graph below from Fast Graphs also emphasizes how expensive the shares of Intuit are. The company is trading for 34 times forward earnings, while the average P/E ratio of the company stands at 28.6 over the last two decades. Moreover, the company has grown during that time at a CAGR of 16%, and the expectations today are for a 14% CAGR. Lastly, the company operates in a higher interest rate environment, making it hard to justify the valuation. To conclude, I believe shares are overvalued with little margin of safety.

Fast Graphs

Opportunities

AI-Driven Expert Platform expansion is a great opportunity. Intuit is positioned to capitalize on its strategic shift towards becoming a global AI-driven expert platform using generative AI. The company’s robust performance in the fourth quarter, marked by a 13% increase in full-year revenue, highlights the success of this approach. The focus on GenAI, a generative AI operating system, enables Intuit to introduce innovations at an accelerated rate. The company leverages its vast data resources, with 100 million customer profiles and 360-degree views of small businesses, to offer personalized experiences. It allows the company to provide personalized financial planning and advice.

“We are entering Intuit’s most exciting era yet and believe the next several years will be game changing.”(Sasan Goodarzi, CEO, Q4 2023 Earnings Call)

Digitization of payments and B2B transactions is another growth opportunity. Intuit’s emphasis on digitizing payments and accelerating B2B transactions presents a significant growth opportunity. The company’s innovations, such as easier discovery, auto-enabled payments, instant deposit, and expanded bill pay solutions, have led to a 22% growth in total online payment volume. With 80% of businesses still using paper checks, there is immense potential for Intuit to capture a substantial market share in digitizing B2B payments, driving further revenue growth in this business segment. This feature can be leveraged together with the AI and the Mailchimp platform.

“Today, easier discovery, auto-enabled payments, instant deposit, and getting paid upfront are all helping drive adoption of our payments offering.”(Sasan Goodarzi, CEO, Q4 2023 Earnings Call)

Another opportunity is the integration of Mailchimp into the ecosystem and achieving global growth with it. The integration of Mailchimp into Intuit’s ecosystem presents a strategic growth opportunity. The focus on developing a complete marketing automation, CRM, and eCommerce suite with payments and global expansion positions Intuit to tap into new markets and customer segments. The introduction of generative AI capabilities in Mailchimp, such as the Email Content Generator, enhances the platform’s appeal to users, accelerating customer acquisition and retention.

“We have three acceleration priorities with Mailchimp… we launched the beta of a new product announcement generator, which uses AI to automatically create an email that a small business can send to its customers.”(Sasan Goodarzi, CEO, Q4 2023 Earnings Call)

Risks

There is a high volatility in the revenues of the Consumer Group. The Consumer Group’s revenue, influenced by unique tax season dynamics, introduces volatility into Intuit’s financial performance. While the overall revenue has shown an average annual increase of 10% over the past four years, the unpredictability associated with tax seasons may impact the consistency of growth. This volatility demands a proactive approach to managing business segments affected by seasonal fluctuations to ensure sustained financial stability. Constant changes in rules and regulations force Intuit to react and impact the demand for TurboTax.

“Each tax season has been unique since the pandemic began four years ago, introducing volatility into Consumer Group results.”(Sandeep Aujla, CFO, Q4 2023 Earnings Call)

Moreover, macroeconomic uncertainty hurts the company’s growth trajectory. Intuit acknowledges the macroeconomic uncertainty and its potential impact on the fiscal environment. Despite guiding for another year of double-digit revenue growth and margin expansion in fiscal year 2024, the CEO is concerned that an uncertain macroeconomic climate may hinder growth, especially in the Credit Karma loans business. This is extremely crucial when considering the current valuation. If this risk materializes, the shares have almost no margin of safety.

“We are guiding to another year of double-digit revenue growth and margin expansion in fiscal year 2024, even with an uncertain macroeconomic environment.”(Sasan Goodarzi, CEO, Q4 2023 Earnings Call)

The Revenue decline of Credit Karma. Credit Karma, a significant component of Intuit’s revenue, faces challenges with an 11% decline in revenue in Q4. It is faster than the decline in the entire year, which stood at 9%. External factors contribute to this decline, including macroeconomic headwinds in personal loans, auto insurance, home loans, and auto loans. While Credit Karma’s core verticals have stabilized, the reliance on specific products, such as credit cards and personal loans, demands continuous adaptation to market dynamics to sustain revenue growth.

“On a product basis, the decline in Q4 was driven primarily by macroeconomic headwinds in personal loans, auto insurance, home loans, and auto loans.”(Sandeep Aujla, CFO, Q4 2023 Earnings Call)

Conclusion

To conclude, Intuit has built an ecosystem for personal finance and small business finance. In a series of acquisitions and organic growth, it has created a resilient group that grows sales and EPS steadily to deliver a growing dividend. The company has several growth opportunities around generative AI and its ability to help decision-making, plan, and streamline marketing and payments for businesses.

The company also deals with some risks to its growth. There is a primary weakness in Credit Karma as the demand for loans is lower, and the competition in the personal finance realm is harsher. Therefore, while I believe that the company is a great one, with plenty of potential, it is the valuation I am uncomfortable with. At 34 times earnings, the company is too expensive in this market environment, and I rate it a HOLD.

Read the full article here