Investment update

As a value investor, I want to maximise the yield (FCF/earnings/dividend) on my investment, whilst paying a low as multiple possible to acquire high-quality assets. I then want my company to compound the earnings produced on my shareholder equity to the nth degree, without delay. In saying that, the combination of (1) valuation, plus (2) earnings and asset factors are essential in first buying companies. Increasing size may be different— (2) is more important a decision rule in this case. For re-entry into a position, it is both.

Readers may recall I was long Avantor, Inc. (NYSE:AVTR) common stock across most of 2020–2023. The investment thesis hinged on 3 critical facts:

- AVTR’s highly diversified top line, no account >4% of sales,

- Deep customer networks forged in multiple industries,

- Multiple sources of value therefore, backed by robust-looking business returns.

Several headwinds have plagued the company in ’23. The major inflection point, a significant change in its end-markets revealed in Q2 earnings, discussed in my last publication. Consequently, the economics have since changed, and my rating also changed on the firm to neutral as a result.

The post earnings drift since the company’s Q3 ’23 numbers haven’t lifted the bid on its market value, indicating the market expects a flat period of business for AVTR moving forward. Based on rigorous analysis of the economic facts, the investment outlook appears to mirror this view.

The revised thesis is premised on four economic assumptions that reconciles the investment to economic realities:

(i). Earnings produced on equity capital are flattening, along with growth;

(ii). Highly leveraged, balance sheet saddled with debt;

(iii). This leverage is what drives AVTR’s returns on equity. The ratio of profits to sales, or sales to assets is not;

(iv). Still priced at 37x trailing earnings, 16x forward EBIT, 2.7x book value.

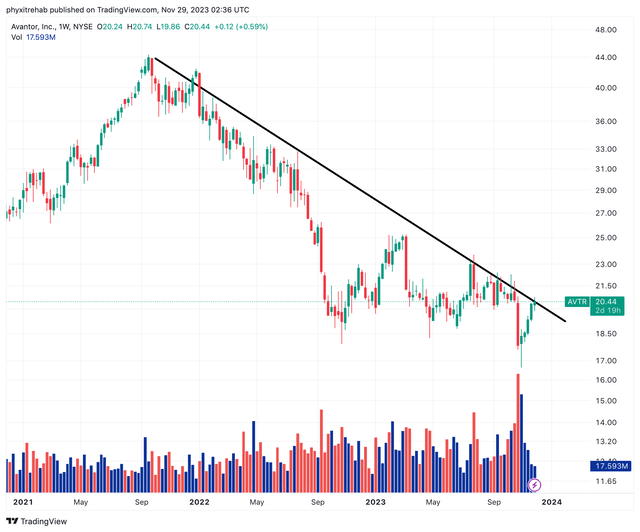

Figure 1.

Source: Tradingview

This report will emphasize these points in full detail. Most critically, you are paying exorbitant multiples but receiving flat growth and flat implied returns on equity to buy AVTR today. Put that in perspective. In my opinion, AVTR has far more to do in order to attract serious investment at these prices. Net-net, I reiterate AVTR as a hold.

Critical factors supporting hold thesis

1. Q3 earnings takeouts

Q3 financials were in line with guidance but signified a difficult period nonetheless, continuing a period of challenging business in 2023. Sales and earnings trends are both down, coming off a strong 2020–2022 period.

The critical issues are as follows:

- Sales + earnings— The company put up Q3 net sales of $1.72Bn, a 7.3% decrease from the same stretch in 2022. It pulled this to adj. EBITDA of $317.8mm, sporting an 18.5% margin. Earnings continued to slide and were booked at $108.4mm, well down vs. $167.0mm in Q3 last year. Management’s adjusted earnings mirrored this trend, tallying $171.6mm against the prior year’s $231.2mm.

- Financial health + cash flows— AVTR also realized $231mm in operating cash flow on FCF of $193mm for the quarter. With all the earnings compression mentioned thus far, the company’s cash flow situation hasn’t mirrored this trend. The percent of quarterly cash flows backing revenues has averaged 12.1% since Q2 2022, and was 13.4% in Q3. It left the quarter running net leverage of 3.9x (net-debt / adj. EBITDA), having repaid >$650mm debt this YTD.

- Looking forward— Management’s revised outlook puts organic revenue growth at negative 6% to negative 5% for the full year. The market has captured this well in AVTR’s market value. All-in revenue growth is slated to range from negative 8.5% to negative 7.5% vs. 2022, on adj. EBITDA margins of 18-19%, down around 50 basis points.

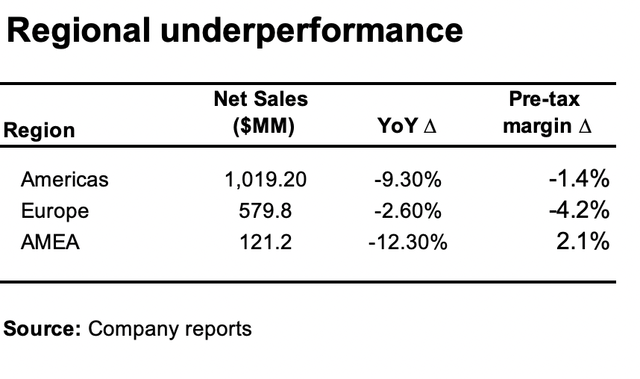

Alas, we have a situation of weakening financials and projected losses moving forward. Moreover, the company’s regional performance was down in Q3, with a significant sales pullback in AMEA and the Americas (Figure 2).

Figure 2.

BIG Insights

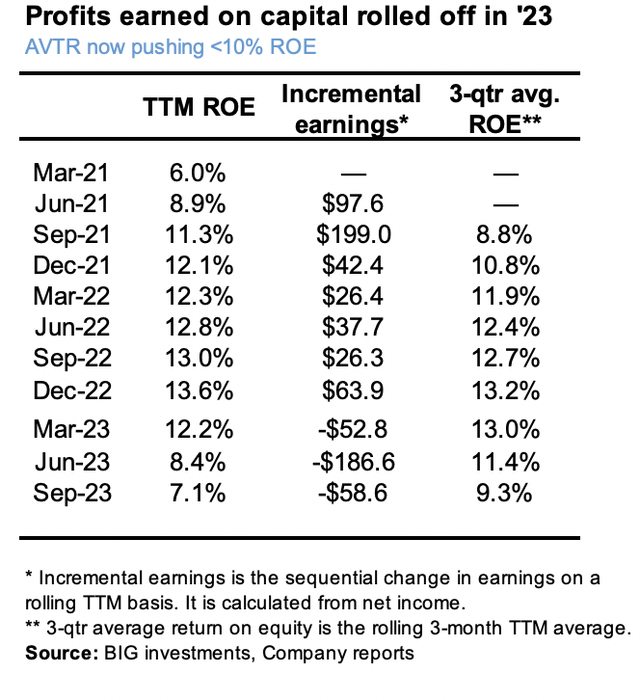

2. Tightening returns on investor capital

Profits earned on equity capital employed in the business were strong across the 2021–’22 period, thanks to Covid-related tailwinds. AVTR kept a 10-13% 3-quarter rolling avg. ROE across this period. It also expanded its book value per share by 44% since 2021, and earnings at a 3-year CAGR of 39%.

These figures have tightened sharply in ’23, however, as seen in Figure 3:

- The company earned 7.1% on $7.54/share of equity value in Q3, down from highs of 13.6% on $7.20/share in Q4 ’22 (TTM values),

- Incremental earnings have rolled over from a period of sturdy growth in 2021–’22, contracting by around $295mm cumulatively since FY’22 yearend. Markets have discounted this accordingly.

What were strong growth figures suddenly aren’t as appealing when compared to net assets employed. Comparing growth to returns on equity not only examines profitability, more importantly, it confirms if growth is/will be value-creative to the investor. Indeed, negative growth can still produce value, so long as the returns on equity are high.

As seen, with AVTR we have a situation of (i) declining growth and profitability, and (ii) earnings no longer creating value for shareholders (TTM ROE = 7.1%). Until this changes, my judgment is the market will continue to trade AVTR sideways.

Figure 3.

BIG Insights

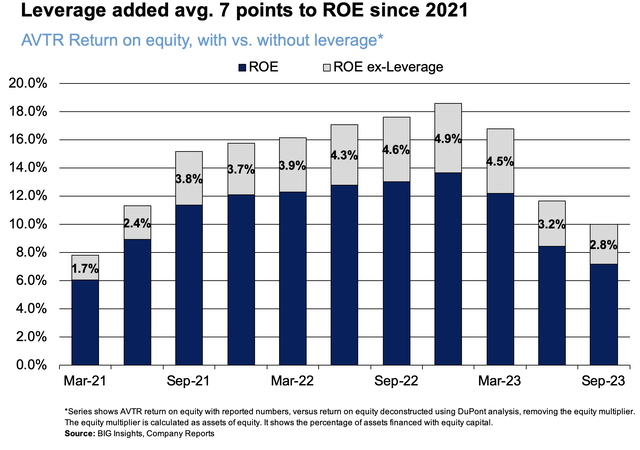

3. Leverage over-represented, with declining FCF per share

Observations of the balance sheet: Total liabilities of $7.6Bn is comprised of $5.2Bn long-term debt and shareholder equity of $5.1Bn. It has $850mm of notional interest rate swaps as of Q3 has cash flow hedges to interest rate risk. Still, debt>equity, meaning the company’s assets are highly levered.

The equity multiplier (assets/equity) measures what percentage a company’s assets are equity financed. The lower the better. Why? A higher slice of total assets are equity-linked. Second, when a company uses debt to finance its investments, it increases its total assets without a corresponding increase in shareholders’ equity (higher multiplier). From 2020–2023 on a rolling TTM basis, AVTR averaged a 3x equity multiplier, settling at 2.5x in Q3. This critical piece of evidence clarifies a few things:

- The average 12–13% of earnings on equity from 2021–’22 is more like 3–4% when removing the leverage effect (Figure 4),

- AVTR is a low-margin, low capital turnover business. The ratio of sales to assets/capital is small. For example capital and asset turnover of c.0.55x and 0.64x in Q3 respectively doesn’t overcome the single-digit net margins each period. Even the use of leverage doesn’t magnify these numbers. Hence, adjusted returns on capital are small, slipping to 2.8% without leverage last quarter, vs. 10% overall.

- The takeaway: The growth outlook is weaker for AVTR explicitly from earnings power and asset factors. Capital tied up in the business is inefficient and isn’t compounding earnings on equity without leverage effects. Using debt is a strategic play—provided the core business is matching up with the rates of return. Not the case here.

In my opinion, this could explain why investors have cut through the company’s previous market highs and looked back to 2019 levels of business in pricing AVTR

Figure 4.

BIG Insights

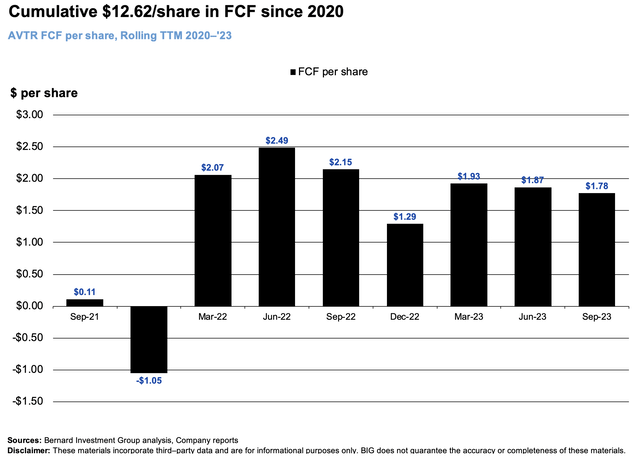

Long-term FCF per share in tact: Despite tightening investor returns, AVTR is still spinning off reasonable free cash flow to its shareholders.

Since 2020, it has cumulated $12.62 per share in FCF, producing $1.8/share in the last 12 months. This is a 9% trailing FCF yield at the time of publication. After an expansionary period in ’22, FCF/share is down-trending, without the corresponding returns on equity capital to suggest cash has been reinvested successfully.

Figure 5.

BIG Insights

Valuation and conclusion

Refer back to the opening sentence of this report quickly. We are looking to buy high-quality assets at sensible valuations, to grow wealth over time.

High quality, via— (i) sales + earnings growth, (ii) compounding earnings on investor equity, and (iii) receiving high and/or growing FCF per share. Sensibly priced, both relatively, and on absolute terms.

AVTR is fetching 37x trailing earnings, 15x forward pre-tax and 2.7x net asset value as I write. Here, several issues must be discussed:

- Earnings growth is skewed to the downside for AVTR moving forward in my opinion, given 1) macro headwinds, and 2) the longer-term trend. My assumptions are for 2.5–4% EPS growth out to 2026. The offer is, therefore, pay 19x for 2.5% annualized growth in earnings.

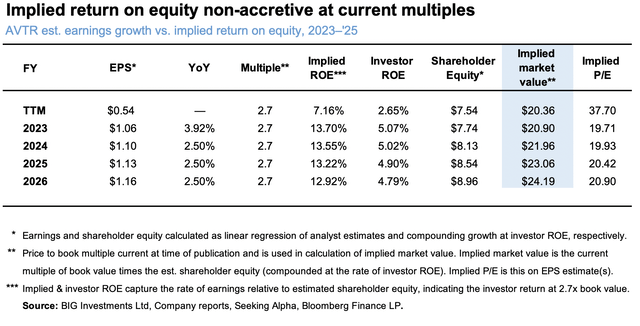

- The ask at the current market price of ~$20.40 is also 2.7x equity capital per share (20.40/7.54 = 2.7x). Paying this, the 13.7% implied ROE adjusts to a 5% ROE for the investor (Figure 6).

- At the function of 1) estimated growth, 2) net asset value assumptions and 3) today’s starting valuations, I get to $24.20 in implied market value by 2026, minimal upside on today’s prices.

Subsequently the recommendation of hold for AVTR is well supported in the economic data. Asking 37x earnings and 2.7x book value is simply too audacious with these underlying fundamentals.

Figure 6.

BIG Insights

In short, I continue to rate AVTR a hold after the latest investment updates. Growth and returns on equity capital are slipping, removing the fundamental catalysts to the firm’s economic machine. Without its use of leverage, AVTR’s corporate profits are actually quite thin, with equally flat capital turnover. All these factors combined support a reiterated hold rating for the company. Net-net, rate hold.

Read the full article here