Earlier this year (June 2023), I wrote an article on City Office REIT (CIO) and City Office REIT, Inc. RED PFD SER A (CIO.PA) recommending avoiding the common equity exposure and instead highlighting the value potential that lies within the preferred shares.

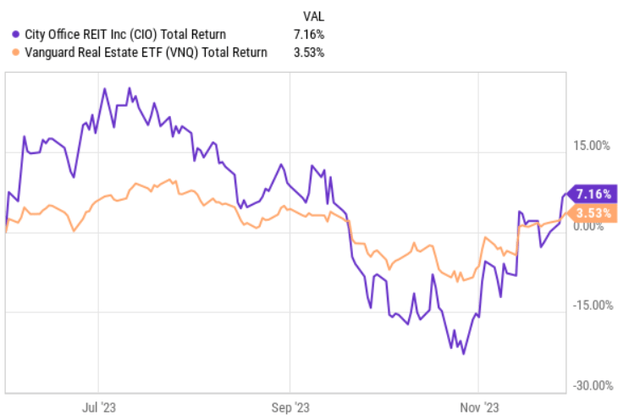

Ycharts

Since then CIO’s stock has experienced a rather volatile ride but on a total return basis has registered slightly better performance than the overall REIT market.

In the meantime, the preferred exposure has warranted a more balanced ride with a total return level at ~7% over the same period starting from June 2023.

Relatively recently, CIO issued Q3, 2023 results, which, in my opinion, optically embody mixed signals and deserve a careful look.

The initial buy rating for CIO’s preferred shares was mainly based on the following three factors:

- Ample liquidity – Due to ~ $100 million in the unutilized credit revolver and $52 million of cash on hand, CIO has greatly mitigated any refinancing risk until 2025. Plus, considering the embedded optionality in the credit revolver, CIO holds the right to extend the refinancing date of the first major maturity until 2026. Ultimately, this provides a time to strengthen the balance sheet and, most importantly, under this period there is a high likelihood of the interest rates going down, which, in turn, could reduce the pressure on cash flows stemming from more expensive refinancings.

- Strong cash retention – In May 2023, CIO cut its dividend by 50%, which effectively now allows CIO to retain ~$11 million of cash each quarter. This level of cash retention is sufficient to organically repay the outstanding debt in 2023 and a significant chunk of 2024 debt maturities.

- Improving fundamentals – Looking back at the most recent quarterly results starting from late 2020, we can see a gradual improvement in almost all operating metrics (e.g., tripling of portfolio utilization rate, positive same-store NOI growth).

Thesis update and synthesis of Q3, 2023 results

As stated earlier, the overall Q3, 2023 results are not that straightforward.

In my view, there is no point comparing Q3’23 with the Q3’22 situation given that during this time period CIO has made significant divestments and deconsolidation of several notable JVs. A more relevant measure of the recent results would be the prior quarter (Q2’23) so that we could observe more directly the rate of change effects across the key operating metrics.

Let’s start with some negatives:

- The FFO per share decreased by $0.01.

- The in-place occupancy ratio dropped by 2 basis points, reaching 85.4%.

- Weighted average remaining lease term decreased by 0.1 years landing at 4.8 years.

Plus, these results do not reflect the consequences of WeWork’s (OTC:WEWKQ) bankruptcy. As of Q3’23, WeWork accounted for 3.1% of CIO’s net rentable area.

Yet, according to James Farrar – CEO & Director as per the most recent earnings call, the locations, which are currently occupied by WeWork are relatively attractive and marketable for other potential tenants:

Fortunately, WeWork leased at our most desirable assets and locations. Each of the three properties and newly construction in a flagship type location for WeWork. In the event, they vacate any of these locations we already have strong interest from leading co-working operators and are ready to move quickly. Alternatively, we have the option of pivoting to leasing to conventional tenants given the demand for premium buildings.

With this being said, we have to be pragmatic and factor in a notable probability that CIO could suffer some further temporary pressures on the underlying cash flows, while new tenants are being attracted.

On the positive side:

- On a same-store or like for like basis, CIO managed to increase the NOI by 2.2%, which on a YTD basis translated to 4.4%. If we adjusted for the decrease in the occupancy rate, the figure would have been even better.

- On the balance sheet end, there was a further reduction of net debt at an amount of ~$7 million.

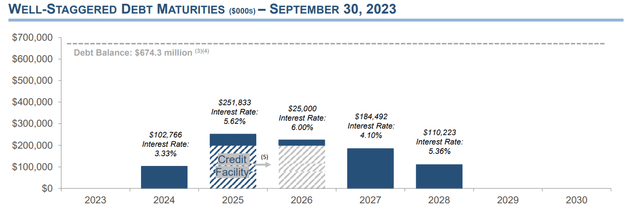

Let’s now take a bit more granular look at the debt financing activity, since that has been one of the key drivers behind the significantly depressed share price.

First, during Q3, CIO managed to complete a renewal of two specific mortgages that comprised the remaining chunk of 2023 debt maturities. The most important thing here is that refinancings were structured in a manner that extended the associated mortgages for five years until 2028. This confirms two elements: 1) it is possible to access financing 2) the loan tenures do not necessarily have to be short-term, which, in turn, removes concerns about refinancing risk over the foreseeable future.

Second, CIO secured swap agreements on these mortgage extensions, fixing the interest rate at 7%. Again, this is not considerably above the current weighted average interest rate, which stands at ~4.2%.

Third, the next major loan maturity is now set to take place in mid-2024 in relation to the non-recourse property loan for a Portland-based office facility with an outstanding principal of $21 million. However, considering that already in December 2022, CIO recognized a full impairment (or write down) of this property, there is no motivation for CIO to keep extending the loan. Especially if there is no underlying cash flow (i.e., the property is vacant). What this means is that it is highly likely that CIO will just hand back the keys to the lender and write down the relevant debt amount as well (i.e., deleveraging the balance sheet without any sacrifices made on the FFO generation front).

As a result, the current debt maturity structure seems to be improved, providing additional safety for preferred shareholders. In other words, there are no remaining debt maturities in 2023 and the amount that is associated with 2024 proceeds is relatively minor if adjusted for the Portland facility. For example, considering that CIO is able to retain about ~$39 million of FFO (based on the annualized Q3’23 FFO result and after a 30% FFO payout), the ~$80 million debt maturity in 2024 could be partially repaid so that only ~$40 million would have to be rolled over, which is totally doable against the backdrop of two aforementioned refinancings and the existing FFO generation.

City Office REIT – Investor Presentation

Plus, if we take a look at 2025 and assume that CIO will exercise its right to defer the refinancing of its credit revolver until 2026, the overall refinancing risk is certainly not that high. It should provide sufficient wiggle room for CIO to accumulate FFO and further capitalize on a rather consistent recovery trend in the underlying operations, thereby de-risking the refinancing event in 2026.

Lastly, at the end of Q3’23, CIO had almost the exact same liquidity profile relative to the prior quarter – i.e., ~ $90 million of undrawn credit and cash reserves of $52 million.

The bottom line

Taking into account the positive factors on the financing front and that the debt maturity structure has further improved, the preferred shares, in my view, are still a rather attractive investment. They currently yield ~10% and are protected by a strong liquidity position, very conservative FFO payout (at 30%), and distant debt rollover profile.

When it comes to CIO’s common equity exposure, in my opinion, the investment case is still not there. While the financials have improved and the like-for-like performance is still solid, the issue with WeWork and potential consequences of further debt refinancing (via higher interest costs) could put additional downward pressure on the FFO.

Granted, if we experience some decline in the SOFR and the market starts to more aggressively recalibrate the expectations on declining interest rates, CIO’s common stock would very likely surge. So, going short CIO would entail a very speculative bet.

My conservative view is that CIO’s preferred exposure is still a buy.

Read the full article here