One of the biggest winners so far this year has been Amazon (NASDAQ:AMZN). The retail and technology giant has seen its shares soar by more than 61% over the past twelve months. The company has reported headline beats on both the top and bottom lines in all three quarters during 2023, and the name looks poised to enter 2024 in great shape. Today, I’d like to discuss why there is still reason for optimism, even after such a large rally.

Amazon’s Q3 report was another home run, with the company handily surpassing Street revenue and earnings estimates. All three of its revenue segments saw top line growth in the low double digits, with Amazon Web Services (“AWS”) revenue growth finally stabilizing. Each segment reported sizable increases in operating margins as compared to a year ago, with the North American segment going from negative 0.5% to positive 4.9%, International nearly erasing an 8.9% negative margin, and AWS increasing its margins by 4 percentage points to over 30% again. In the end, Amazon generated nearly $10 billion in profits in Q3 2023, up from less than $2.9 billion in the year-ago period.

In the short term, one of the biggest tailwinds I’m watching is in regard to currencies. The Dollar Currency Index has lost more than 2.5% since Amazon’s last earnings report. Management had only guided to a slight favorable sales impact from foreign exchange for Q4, but where we stand today that number could approach $2 billion. With analysts expecting around $165.9 billion for sales in the current quarter, towards the high end of the company’s guidance for $160 billion to $167 billion, every little bit helps to avoid a revenue miss.

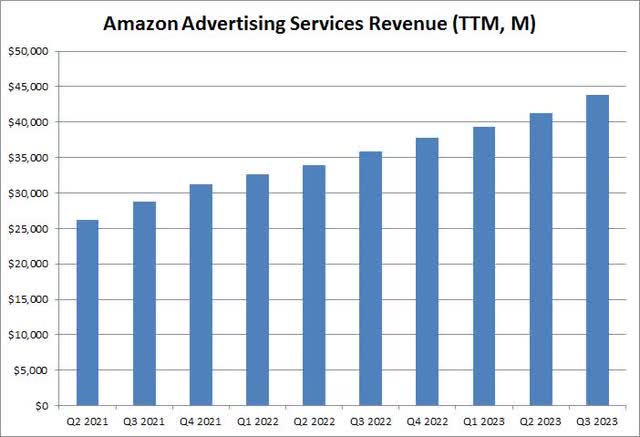

One area that Amazon has done exceptionally well in recently is advertising services. Just a few years ago, the company didn’t even bother breaking out the numbers here because they weren’t that material to the overall business. However, ad revenue in Q3 of this year was more than $12 billion, a new quarterly record, growing more than 25% over the prior year period. As the chart below shows, this segment is on the doorstep of doing $50 billion in trailing twelve-month (“TTM”) revenue, a number that could be hit in 2024.

Amazon Ad Revenue (Company Earnings Reports)

Perhaps the most important thing recently is Amazon’s financial discipline. The company went on a dramatic post-Covid spending boom to grow, with capital expenditures significantly outpacing operating cash flow. In Q2 2022, Amazon reported a free cash flow of negative $23.5 billion for the trailing twelve-month period. However, the latest results showed a positive free cash flow of more than $21 billion for the last four reported quarters. Rising interest rates have helped the income statement a bit as well, with net interest expense declining by about $400 million over the past 5 quarters. Amazon might even report net interest income in 2024, a meaningful improvement from the roughly $1.5 billion run rate annual expense it was seeing just a handful of quarters ago.

In recent months, energy prices have come well off their yearly highs, and that’s certainly been a help to headline inflation numbers. As the chart below shows, gas prices have dipped considerably since Amazon reported its Q3 results back in late October, and there is likely more downside to come. The company itself will likely save a bit in the coming quarters on fuel costs, but that’s probably not the biggest thing to discuss here.

US Gasoline Average (GasBuddy)

Gas prices certainly have one of the biggest impacts on US consumer inflation expectations. When you drive by a station each day and you see prices falling, you might be more inclined to spend on other items moving forward. In the last week alone, we’ve seen some very positive reports on consumers’ views regarding inflation – consumer inflation expectations hit a one-year low, and the University of Michigan monthly survey saw its lowest inflation expectation mark for the next twelve months in more than two and a half years.

The one knock on Amazon usually has to do with its valuation. On a price to earnings basis, it is not a cheap stock, going for more than 42 times the current 2024 average analyst EPS estimate. That’s substantially higher than most of its large-cap tech peers that go from 20-30 times their respective estimates over a similar time. However, Amazon’s forward P/E has actually improved by about 10 points over where it was a year ago, and the overall situation surrounding the name seems to be much better now.

If you didn’t buy at this time in December 2022 because a forward P/E of 52 scared you off, well, you certainly missed a large rally. Moving forward, investors might be more willing to pay that kind of premium if they know that the Fed won’t raise rates any further, with the potential for interest rate cuts in 2024 and beyond. If Amazon can hold even a 35 forward P/E with an expectation of $5 in 2025 (current street average is $4.66), that would imply shares a year from now could trade at $175, or almost 19% upside from here.

For the reasons discussed today, I am upgrading Amazon shares to a buy. While there has already been a large move in the stock, I think we could see further gains in 2024 as the market gears up for a Fed pivot as inflation comes down even more. Lower consumer inflation expectations could mean stronger retail sales, and Amazon is working to further improve its margin structure. With AWS nearing $100 billion in yearly revenue and the advertising business also soaring to new heights, I think we could see double-digit upside here if this recent progress continues.

Read the full article here