Micron Technology, Inc. (NASDAQ:MU) stock has put up an impressive rally, surging by 70% after bottoming in late 2022. Micron had a challenging phase due to the economic slowdown and other macroeconomic factors. Its revenues crashed by 50% during the brutal tech-market earnings-recession phase, a dynamic further exacerbated by China chip bans and other detrimental elements.

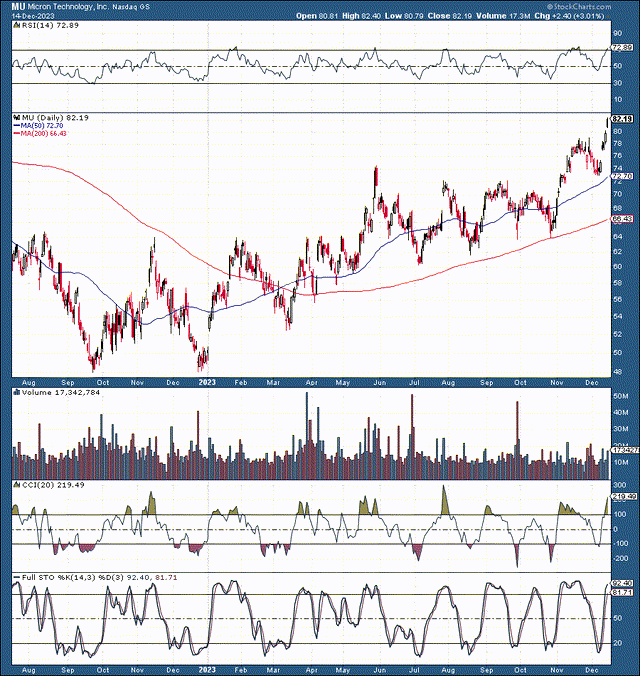

MU (StockCharts.com )

However, Micron has turned around, and the stock has made considerable gains. Moreover, momentum remains strong, with Micron bumping up against 52-week highs. Also, Micron’s revenues should recover to pre-earnings recession levels next year (fiscal 2025). Micron recently increased guidance, implying it should beat upcoming earnings estimates in several days (December 20th).

Micron’s earnings should also be boosted due to the AI boom and its industry-leading memory and storage solutions. Micron’s stock is relatively inexpensive in light of its robust revenue growth prospects and substantial profitability potential. Therefore, Micron’s stock can continue trending higher in the intermediate and long term.

Higher Revenue Guidance is Highly Positive

Micron recently increased its fiscal Q1 2024 revenue guidance. Due to the improving supply/demand and pricing dynamic, the chip giant expects revenue to be around $4.7B, from a previous guidance of $4.2B to $4.6B. Wall St. analysts expected $4.4B. The new guidance implies Micron can beat the prior estimate by about 7%, which is significant.

Also, Micron likely would only revise guidance if it was confident it could beat by at least 7%. Therefore, the company may report even better results than expected. A 10% revenue beat seems reasonable in this scenario, suggesting Micron could report revenues in the $4.8-4.9 billion range. This result would be highly favorable, implying Micron could continue outpacing depressed guidance as we advance.

Upcoming Earnings – Why Micron Could Outperform

Last quarter (fiscal Q4 2023), Micron beat revenue estimates by about $85 million, and the company reported better than anticipated EPS. Now, consensus estimates are for a non-GAAP EPS loss of $1.02 on revenues of $4.62B.

Yet, due to the increasingly favorable supply/demand pricing dynamic, the AI effect, and other constructive factors, Micron could report revenues around $4.8B, roughly 5% above current estimates. Moreover, Micron’s EPS could also improve more than anticipated, enabling Micron to report a smaller-than-expected loss, which should reflect favorably on Micron stock. Also, this phenomenon would illustrate that Micron’s future earnings need higher revisions, leading to a higher multiple and a rising stock price as we advance.

Micron’s AI Effect – Constructive Tailwind

Micron has significant AI potential, which should reflect favorably on its growth, profitability, and stock price. Micron’s AI smart manufacturing is leading to historic levels of output, yield, and quality in its industry-leading memory and storage solutions. Micron’s memory and storage solutions enable endpoint generative AI experiences. Micron’s high-performance memory and storage solutions also drive practical AI business applications like recommendation engines for e-commerce and IP-friendly generative AI models. Due to its market-leading position, Micron should continue riding the AI wave in its industry. This dynamic should lead to better-than-anticipated growth, higher levels of profitability, and a significantly higher stock price in future years.

Micron Stock: Deceptively Cheap

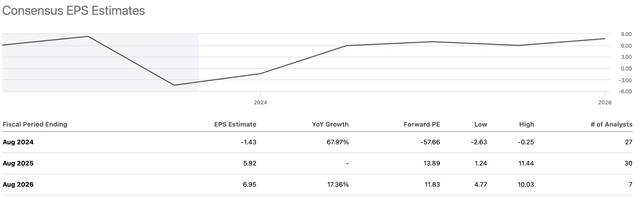

Micron’s stock is deceptively cheap here. Despite fiscal 2023 and 2024 EPS turning negative, we should see a robust earnings recovery in the years ahead.

EPS estimates (SeekingAlpha.com )

Next year’s consensus estimate is for about $6 in EPS. However, due to the improving supply/demand pricing dynamic, the AI effect, and other constructive elements, Micron could report substantially higher EPS next year and in future years. We have a wide estimate range for next year, with high-end EPS estimates shooting above $11. Micron could earn about $8 next year, implying its stock trades at about ten times forward EPS estimates.

This valuation is cheap for Micron, as it can grow EPS in the future. Due to the economic recovery and a more accessible monetary environment, Micron can potentially achieve $10 in EPS in fiscal 2026, continuing considerable EPS growth in future years.

Where Micron’s stock could be in the future:

| Year (fiscal) | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue Bs | $35 | $38 | $42 | $45.5 | $49 | $53 |

| Revenue growth | 52% | 9% | 10% | 9% | 8% | 8% |

| EPS | $8 | $10 | $12 | $14.2 | $16.4 | $19 |

| EPS growth | N/A | 25% | 20% | 18% | 16% | 15% |

| Forward P/E | 15 | 16 | 17 | 18 | 17 | 16 |

| Stock price | $150 | $192 | $241 | $295 | $323 | $352 |

Source: The Financial Prophet.

Micron Risks

Despite my bullish analysis, Micron faces risks due to competition, geopolitical threats, supply/demand and pricing dynamic, and other variables. Moreover, a slowing global economy or a recession would likely impact Micron negatively. Also, Micron may not achieve the level of growth my estimates project, and its profitability may not expand as quickly as expected. Additionally, Micron’s P/E multiple may remain depressed due to product cycles, competition, and other variables. Investors should examine these and other risks before investing in Micron.

Read the full article here