All financial numbers in this article are in Canadian dollars unless noted otherwise.

(A Lengthy) Introduction

If there’s one thing we have discussed a lot this year, it’s energy. Energy is a cornerstone of my long-term investment thesis, as I believe that we are in a new era where subdued long-term supply growth meets consistent demand growth.

Essentially, since 2020, my optimism about oil and gas has grown significantly.

Initially fueled by the anticipation of post-pandemic demand driving up oil prices, my skepticism towards the renewables trend contributed to my preference for oil and gas investments.

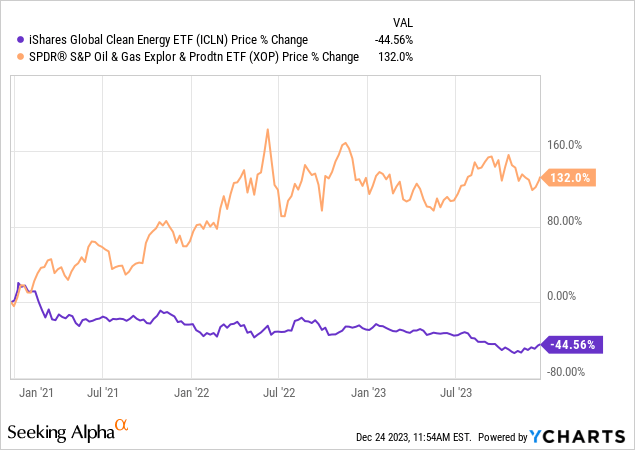

Over the past three years, clean energy stocks have lost roughly 44% of their value, excluding dividends, while oil and gas drillers have gained over 130%.

Data by YCharts

Don’t get me wrong, I’m not against clean energy – not at all. My concern lies in the forced global energy transition, leading to subdued investments in oil and gas despite robust demand.

Companies now prioritize free cash flow for stability and reduced vulnerability to oil price crashes. Most companies, that is.

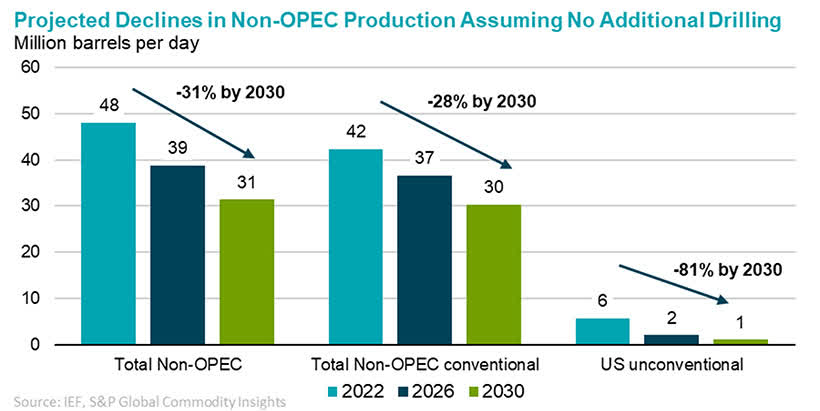

Furthermore, U.S. shale production is losing steam, and estimates suggest a potential 81% decline by 2030 without new drilling. This shift has global implications, impacting supply growth and giving OPEC, especially Saudi Arabia, significant pricing power, which they have used this year by cutting output.

International Energy Forum

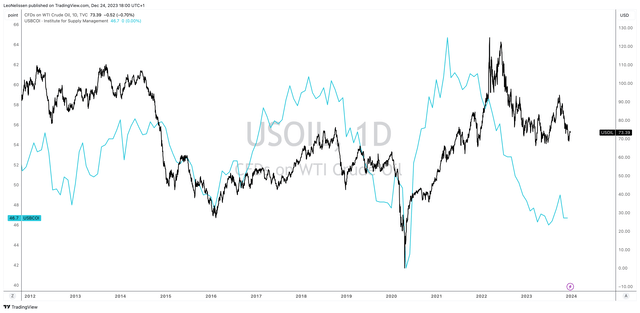

While it is certainly possible that oil prices could continue to decline if economic growth keeps deteriorating, I believe that oil prices will remain elevated for many years to come, with a high probability of triple-digit dollar oil prices in a scenario of strengthening economic growth.

Right now, WTI (CL1:COM) is trading above $70 despite the fact that the ISM Manufacturing Index has been in contraction territory every single month this year.

TradingView (WTI, ISM Index)

I believe that if the supply situation were different, oil would be trading barely above $50 right now.

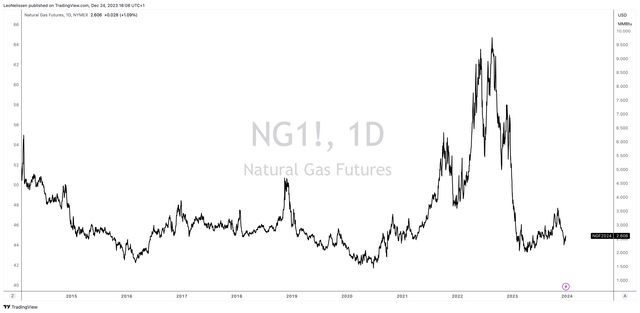

With that said, the situation for natural gas is a bit different, as natural gas supply growth is faster. This commodity is more abundant and way more volatile than oil.

NYMEX Henry Hub benchmark natural gas prices are at just $2.60 per MMBtu due to weak economic growth, mild weather, and higher-than-expected inventories.

TradingView (NYMEX Henry Hub)

However, on a long-term basis, I am very bullish on natural gas.

This is what I wrote in a recent article (emphasis added):

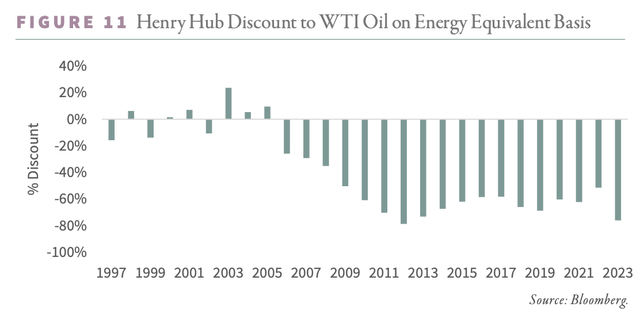

Energy experts Goehring & Rozencwajg believe that natural gas prices in the United States are way too cheap, according to global energy prices.

In fact, G&R believes that natural gas prices in the U.S. are trading at an 80% discount to global energy prices.

Goehring & Rozencwajg

Although a discount is warranted due to America’s deep natural gas reserves and cheap production methods, it is likely that this discount will decline.

The initial expectation of convergence in North American natural gas prices with international prices faced delays due to a mild winter and a fire at the Freeport LNG export terminal in 2022.

These events, along with increased U.S. inventories, led to an 80% decline in North American natural gas from the 2022 peak.

However, these challenges are deemed temporary, with excess inventories being addressed and operators planning to add six bcf/d of new LNG export capacity in 2024.

Furthermore, G&R’s models now suggest that shale production is likely plateauing, and the discount to world prices will narrow, possibly disappearing.

The models predict that North American natural gas is on the verge of entering a structural deficit for the first time in 20 years, potentially prompting regulatory actions to limit exports and stabilize prices.

Based on these numbers, Henry Hub natural gas prices of at least $10/MMBtu could become the new normal.

This brings me to the star of this article, an oil and gas producer from Canada, which has everything I’m looking for in an energy stock:

Deep reserves.

Very efficient operations.

A healthy balance sheet.

A focus on shareholder distributions.

It’s also one of the few companies focused on fast growth, which bodes very well for future free cash flow and shareholder benefits.

That company is ARC Resources Ltd. (OTCPK:AETUF, TSX:ARX:CA), a company I believe most won’t be familiar with.

So, let’s dive right into it and discuss why I put this stock on my watchlist, as I believe it would be a great addition to my portfolio.

One Of The Best In Its Industry

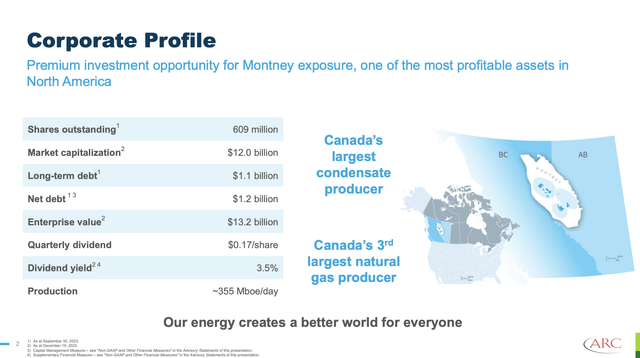

Arc Resources is one of Canada’s largest oil and gas producers, with a market cap of roughly $12 billion. That’s roughly US$9 billion.

It produces close to 360 thousand barrels of oil equivalent per day (MBOE/d), which makes it one of the biggest producers in all of North America.

The company produces in the Montney Formation, which is a part of Canada’s famous Western Canadian Sedimentary Basin (“WCSB”), an area with some of the world’s biggest fossil fuel reserves.

ARC Resources

The company is so large that it is Canada’s 3rd-largest natural gas producer.

Note that oil accounts for just a quarter of its total production. The remaining production comes from natural gas and higher-margin natural gas liquids (“NGL”).

As we can see below, over the past ten-ish years, the company has divested a lot of non-core assets to focus on the best growth plays in the Montney Formation.

As a result, with fewer plays, it still managed to boost production from $110 MBOE/d to 350 MBOE/d.

ARC Resources

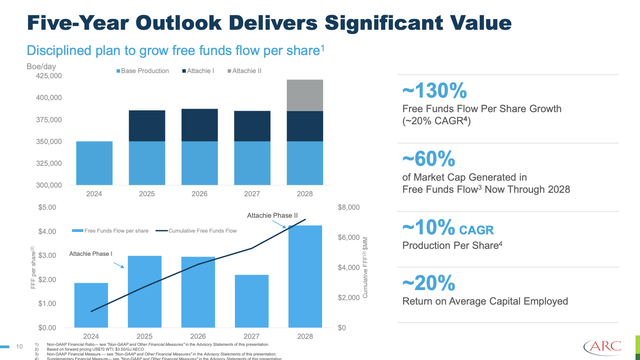

What fascinates me about ARC is its long-term plan. After divesting non-core assets, it is now working on an ambitious five-year plan.

ARC, in its ambitious five-year plan spanning from 2024 to 2028, envisions a strategic approach that emphasizes capital efficiency, sustainable growth, and substantial returns for its shareholders.

At the core of ARC’s strategy is a commitment to a capital-efficient program designed to foster long-term per-share growth. The company aims to strike a balance between investing in its valuable assets and ensuring a meaningful return of capital to shareholders.

ARC’s production guidance for 2024 is set between 350,000 to 360,000 BOEs per day. This projection factors in the anticipated expiry of an ethane sales contract in the second quarter, which is expected to reduce reported NGL production by approximately 5,000 barrels per day on an annualized basis.

To counter this, ARC plans to reinject ethane into the natural gas stream, resulting in higher revenue from the sales of higher heat-content gas.

With this in mind, as we can see below:

The company aims to grow per-share production by 10% per year.

Free cash flow per share is expected to grow by 20% per year (dependent on prices).

The company aims for a 20% return on average capital employed.

ARC Resources

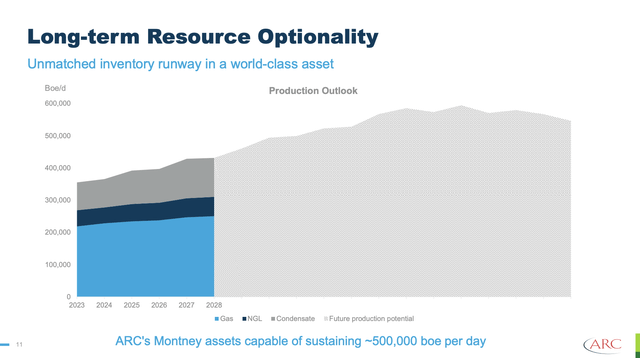

In other words, while other players are reducing future growth plans, ARC is eager for rapid production growth – even after 2028, as we can see in the chart below.

Unless its peers follow and boost production as well, ARC is in a fantastic spot to benefit from higher production and better (expected) pricing on a prolonged basis.

ARC Resources

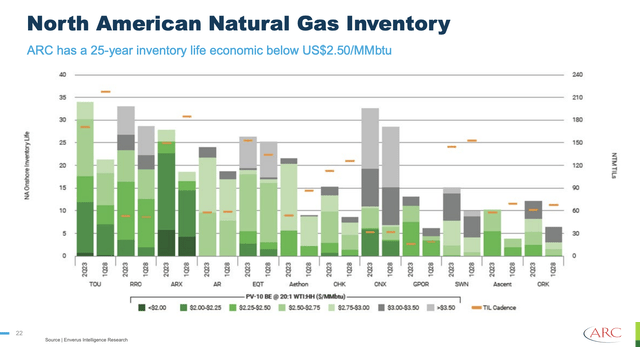

However, unlike most peers, the company is in a good spot to boost production. It has massive reserves!

The company currently has a 25-year inventory life that is breakeven below US$2.50 Henry Hub. This makes ARC a standout player in its industry.

ARC Resources

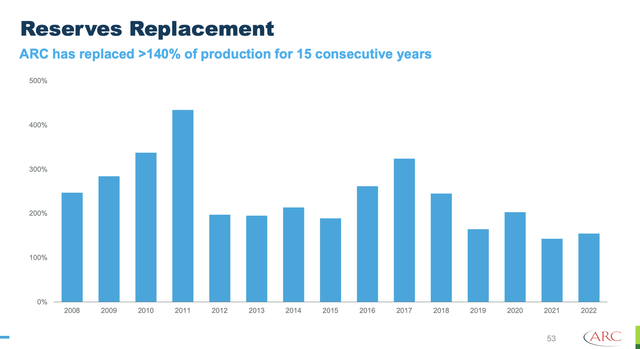

On top of that, the company consistently expands its reserves. ARC has replaced more than 140% of production for 15 conservative years.

ARC Resources

Furthermore, in 2024, ARC plans to invest $1.8 billion, a reduction of about $200 million compared to 2023, adjusting for its Attachie growth capital.

The company attributes this efficiency to two key factors:

a lower corporate decline in 2024, necessitating fewer wells to offset production declines and

a concerted effort to further reduce nonproductive capital, particularly at Kakwa.

ARC forecasts little change in its cost structure for 2024. Operating and transportation costs are expected to remain relatively unchanged year-over-year, hovering around $10 per BOE combined.

This stability underscores the resilience of ARC’s business model, as the company asserts it can sustain production in the range of 350,000 to 360,000 BOE per day and fund the current dividend with organic cash flow even in a challenging environment with WTI at US$45 a barrel and $2 AECO per Mcf.

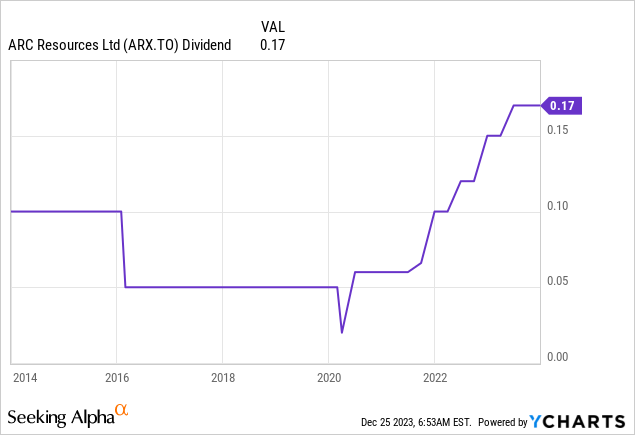

Bear in mind that the base dividend is $0.17 per share per quarter. This translates to a yield of 3.5%. This dividend is protected at US$45 WTI and just CAD$2 AECO, which is very low!

Note that the company has realized an average premium to AECO prices of 20% over the past decade. I expect that to hold, as it is using liquid natural gas opportunities in North America, which comes with additional pricing benefits.

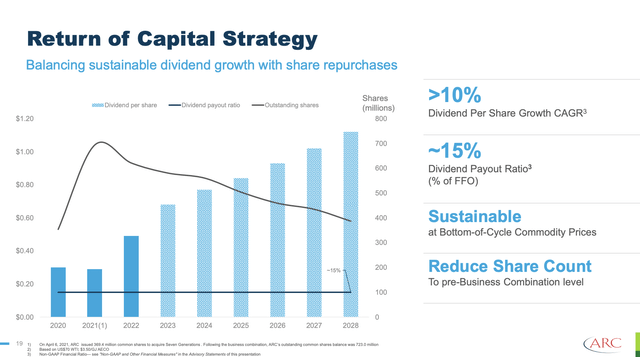

Since 2020, the company has consistently grown its dividend and is expected to keep doing this for many more years to come.

Data by YCharts

Also note that the company wants to grow the dividend along with its business, not the price of oil.

This is very important to keep in mind, as it is using per-share production and free cash flow growth to sustainably grow the dividend.

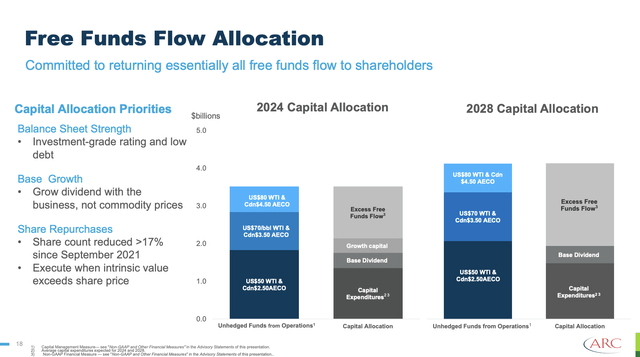

Excess free cash is distributed using buybacks.

ARC Resources

Since 2020, the company has grown its dividend by roughly 10% per year. It has a dividend payout ratio of just 15% (so much room for dividend growth and buybacks) and a significant reduction in its share count.

ARC Resources

As we can see in the overview above (Free Funds Flow Allocation), at US$80 WTI and $4.50 AECO, the company can generate close to $1.5 billion in free cash flow after its base dividend. That’s an additional 12% in buyback potential, excluding growth capital.

That is almost unmatched in its industry.

In 2018, that number could be north of $2 billion, or almost 17% of its market cap, due to higher production rates.

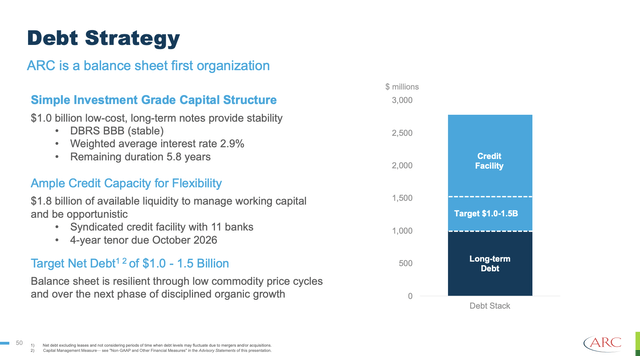

It also has a healthy balance sheet, which allows the company to prioritize shareholders over debtholders.

The company has no debt maturities until 2026. It also has no maturities between 2026 and 2031.

Even at US$50 WTI/US$3 Henry Hub, it has a net debt to FFO (funds from operations) ratio of less than 1.0x.

The company aims to keep net debt between $1.0 and $1.5 billion.

ARC Resources

Now, let’s take a look at the valuation.

Valuation

This is the tricky part, as companies that rely on the price of the commodities they produce are prone to volatile earnings.

However, I am making the case that ARC is cheap.

As I believe that both natural gas and oil prices have a bright future, the company’s aforementioned free cash flow potential makes it a great buy at these levels.

Even at these levels and based on current analyst estimates, the stock is cheap.

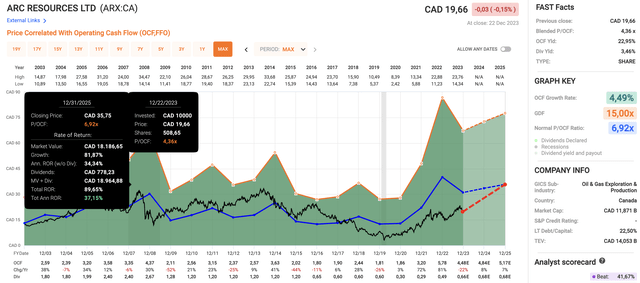

The company currently trades at a blended P/FFO ratio of 4.4x. That is below its long-term normalized valuation of 6.9x. A return to that valuation based on 22% expected FFO contraction in 2023, 7% expected growth in 2024, and 8% expected growth in 2025 would give the stock a fair price target of roughly $36 in Toronto. That is 80% above the current price.

FAST Graphs

Although I do not promise anything, I believe that once energy prices start a sustainable uptrend with support from improving economic growth, investors will rush into undervalued energy plays, causing ARC shares to trade much higher.

Hence, I am using $36 as a longer-term target.

Currently, I do not own ARC Resources Ltd. However, I am figuring out how to include it in my portfolio. I own Canadian Natural Resources (CNQ) and Devon Energy (DVN) in my dividend portfolios. I will likely sell some natural gas stocks from my trading portfolio and start one or two meaningful new energy positions in my long-term investment portfolio. One of them is likely to be ARC Resources.

Needless to say, I’ll keep readers up-to-date in 2024!

Takeaway

As global forces push for a green transition, ARC Resources Ltd. stands out as a robust player in oil and gas.

Boasting a 25-year inventory life and a strategic growth plan, ARC combines efficiency with shareholder-friendly practices.

The company’s commitment to sustainable growth, a 20% return on capital, and a resilient dividend, even in challenging conditions, make it a standout in the industry.

With a current undervaluation and a potential fair price target of $36, ARC Resources is a promising addition to my watchlist, signaling a bullish outlook on the long-term prospects of natural gas and oil.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.