Shares of Equitrans Midstream (NYSE:ETRN) have had a stellar twelve months, rising about 50% as its major expansion pipeline project is set to finally begin operations in coming months. Once it actually begins operations and begins contributing to ETRN’s cash flow, I anticipate further upside for shares, and that could also be the catalyst for management to sell the company. Either as a stand-alone entity or through M&A, I see a potential 50% return over the next two years.

Seeking Alpha

Equitrans is a relatively small natural gas-focused midstream company, but the conversation about the stock begins and ends with its multiyear, multibillion pipeline project through West Virginia. Fortunately for the company, West Virginia Senator Joe Manchin, as a key swing vote, is among the most powerful elected officials in the country. So, as part of the 2023 debt ceiling deal, the Mountain Valley Pipeline (MVP) received expedited approval. This provision in the May agreement is why shares immediately spiked.

In Q3, Management guided to MVP coming online during Q1, ending a multiyear saga, at a total cost of $7.2 billion. This was slower than initially hoped because there was difficulty in securing the labor with a peak of 4,500 workers on the project. ETRN owns 49% of the pipeline and operates it. Given that initial pushback, there has been some lingering concern that MVP’s start date could slip further. That is why I was very encouraged to see that on January 3, Equitrans reiterated its Q1 estimated start date in a filing to the SEC.

That updated filing gives me comfort that ETRN will deliver on its Q1 start date. Beyond MVP, Equitrans has several associated growth projects; however, it has already curtailed one, Southgate, from $468 million to $370 million with operations expected to being in mid-2028. Project delays and cost inflation are likely contributing to the company’s decision to pare back growth projects beyond MVP. Still, MVP alone will bring $220 million of incremental annual EBITDA to ETRN while its associated Hammerhead pipeline should bring in $70 million. Assuming a 9-month contribution, they should provide about $210 million of incremental EBITDA to Equitrans in 2024, which will be critical for debt reduction as management aims to bring debt down to 4x EBITDA from 6x today.

Aside from MVP, Equitrans is performing fairly well. In Q3, transmission volumes rose 12% to 4,510BBtu/day in Q3. Its operations are supported by a 13-year average life on its gathering contracts and 11-year average life on transmission and storage contracts. About 71% of service revenue comes from firm fee reservations. This provides an important baseline for steady and predictable cash flow. As you can see below, these contracts run fairly steadily over the next four years.

Equitrans

One concern I monitor is whether throughput is significantly below the “minimum volume commitment” (MVC) in these contracts. That suggests that when contracts expire, the pipeline operator will struggle to sign new contracts and that revenue could fall. ETRN’s long-life on its contracts diminishes this risk. Even more encouragingly, its gathering unit had just $2 million of MVC shortfall payments, about 1% of total, not a material concern.

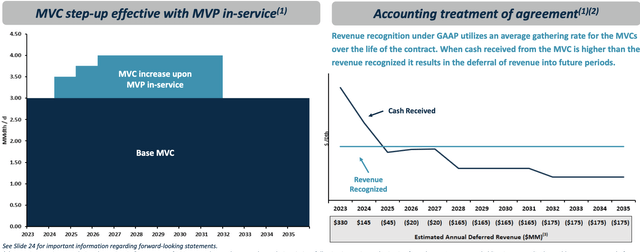

Moreover, the MVP will provide Utica natural gas producers the ability to sell into the high-growth Southeast, which should improve the realizations they receive, encouraging more production and further increasing utilization and rates on Equitrans’ system over time. Its Utica gathering assets can send 2bcf/day to MVP with EQT (EQT) signed for 11 more years at 1.29bcf/day. EQT is a key operator for Equitrans. Starting this year, EQT’s MVC increases once the mountain valley pipeline begins operations. I would note that this contracted was structured with EQT paying more cash upfront than in later years, which helped to minimize the debt ETRN needed to take on to build MVP. As such, beyond 2027, cash flow growth will likely underperform EBITDA growth. Given its balance sheet, this trade-off of less debt today for less revenue in the future was a sound one for Equitrans.

Equitrans

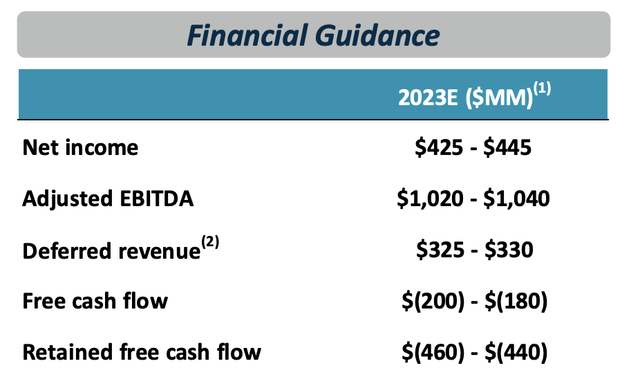

Based on its Q3 results, management now expects about $1.03 billion in EBITDA with about a $190 million free cash flow burn. Excluding MVP, 2023 retained free cash flow is about $285 million, which speaks to the size this project.

Equitrans

MVP is going to transform ETRN’s financials, boosting results by about 20%, and as such, I expect markets to assign relatively little weight to Q4 results, instead focusing on MVP’s start date, 2024 guidance, and debt reduction plans. Once MVP is up and running, it should contribute $120-140 million in free cash flow to ETRN in my view, giving it a $400 million retained free cash flow run-rate. I expect about 65-75% of this annual rate to be realized in 2024, depending on the speed of the ramp to full operations. Additionally, when MVP is up and running, that entity can issue debt, and the proceeds will be dividended up to its owners with Equitrans receiving about $900 million. It can use that to reduce its debt load, likely allowing it to pay off its 2024 and 2025 maturities and even tender for longer-term debt, giving it some much-needed breathing room.

Equitrans

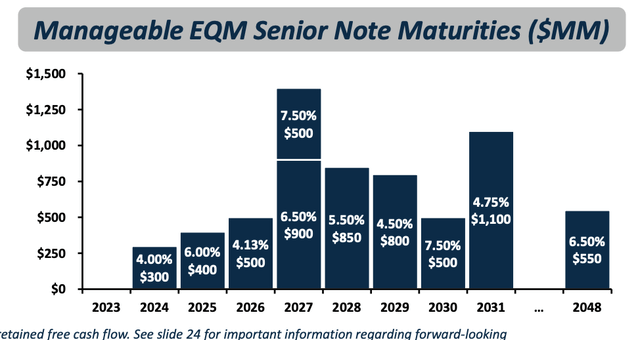

Currently, ETRN has $7 billion in net debt. ETRN should do about $1.27 billion in EBITDA in 2024, and about $1.35 billion in 2025 when it has a full year of MVP. That means ETRN can carry about $5.4 billion in debt. Management expects to get to its leverage target 2 years after MVP is operating, or Q1 2026. With about $800 million in retained cash flow and $800 million of debt paydown from MVP, I view this as plausible. At that point, there will be scope for ETRN to meaningfully increase its dividend, which already yields over 5.8%, and buy back stock.

Equitrans largely bet the company on MVP, carrying a significant debt load, for a pipeline asset that transforms its Utica operations with an asset that will be a critical pipeline supplying the Southeast’s energy needs for decades. Thanks to the debt ceiling agreement, this gamble is set to pay off handsomely, and shareholders have already seen significant gains this year.

There are also reports that Equitrans is considering selling itself, as a major interstate pipeline could attract interest from MLPs, private equity, or infrastructure funds. I would expect ETRN to wait for the pipeline to officially begin operations before engaging in a sale to close any remaining valuation gap, which is still fairly substantial.

Including preferred equity, ETRN has roughly a $12.1 billion enterprise value. At run-rate EBITDA once MVP has commenced, it is being valued at 9x EV/EBITDA. For comparison, MPLX (MPLX) and Williams (WMB) are both over 11x EBITDA. Given its smaller scale, by 2026 if ETRN gets to 10x EBITDA, that implies about $1.8 billion more in equity value or 40% upside to ~$14.50. Combined with its dividend, that is an over 50% two-year return. That makes shares extremely compelling in my view.

Equitrans has been a strong performer in 2023 as investors began pricing in the launch of MVP. However, given just how transformative this is to the company’s financials, and it swinging to a significant retained cash flow position, I see further upside, which I expect to be realized as lingering uncertainty over the official launch date disappears. I expect a material two-year run in shares, which could be realized more quickly if a sale occurs, though I expect that to be after Q1, if it happens. Either way, ETRN is a compelling buy opportunity.

Read the full article here