Introduction

I’ve been following Holley Performance Products (NYSE:HLLY) closely, and I’ve written six articles about the company on SA to date. The latest of them came out in November 2023 and back then I said that the outlook for the business was improving and that Holley was on track to achieve annualized cost savings of around $35 million.

On 8 May, Holley released its Q1 2024 financial results, and I think they were mixed as revenues went down by 7.9% year on year while net income declined by 12.2% despite cost savings. In addition, free cash flow over the remainder of the year could be limited as inventory level improvement opportunities seem depleted. I’m cutting my rating on Holley’s stock to neutral. Let’s review.

The Q1 2024 financial results

In case you are unfamiliar with Holley or my earlier coverage, here’s a short description of the business. The company specializes in the design, manufacturing, and sale of after-market performance automotive parts such as fuel injection systems, nitrous oxide injection systems, and superchargers. It’s also involved in the production of exhaust products, transmissions, and tuners among others. Holley’s target customers are car and truck enthusiasts across the USA, and Europe and the company has facilities in the USA, Canada, Italy, and China. Its brands include Brawler, NOS, Dinan, and Simpson among others.

Holley

Holley listed on the NYSE in 2021 through a merger with a special-purpose acquisition company (SPAC) and many of these brands had joined its portfolio through acquisitions in the years before that. However, the Holley’s strategy pivoted from inorganic growth to cost cutting, inventory optimization, and debt repayment in 2022 as its financial results were put under pressure by supply chain disruptions and chip shortages.

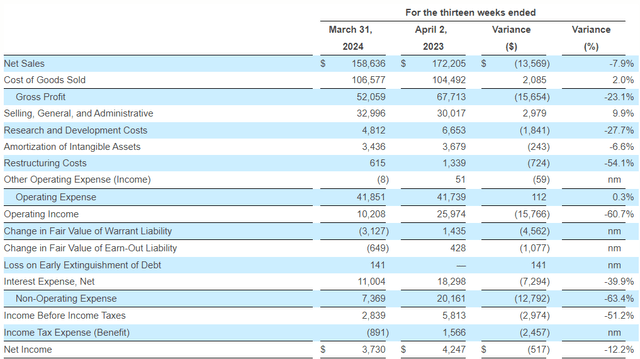

Looking at the Q1 2024 financial results, we can see that it was a challenging quarter for Holley as net sales decreased by 7.9% year on year to $158.6 million. Revenues declined across all product categories and the company blamed high inventory levels at the end of 2023 as a result of underwhelming holiday demand. On a positive note, the company continued to implement its cost cutting program and the optimization of freight policies generated $3.7 million in savings during the quarter. In addition, research and development expenses were slashed by 27.7% to $4.8 million. Interest expenses also fell significantly but this was due to the positive impact of its interest rate collar during the period so it’s likely to be temporary. Unfortunately for investors, these positive developments couldn’t compensate for the loss of economies of scale in full and net income fell by 12.2% to $3.7 million.

Holley

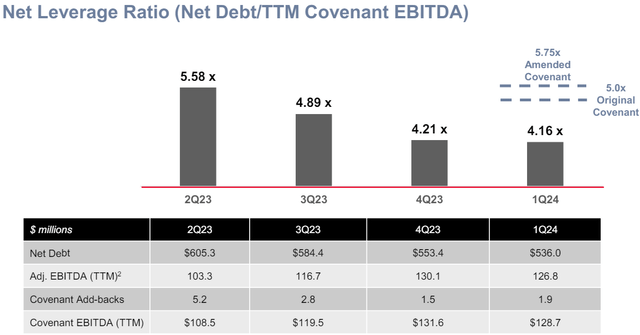

Turning our attention to the balance sheet, Holley continued to pay down debts in Q1 2024, and its net debt stood at $536 million at the end of March. The net leverage ratio thus remained well below its credit agreement covenant of 5.75x despite the decrease in adjusted EBITDA for the quarter.

Holley

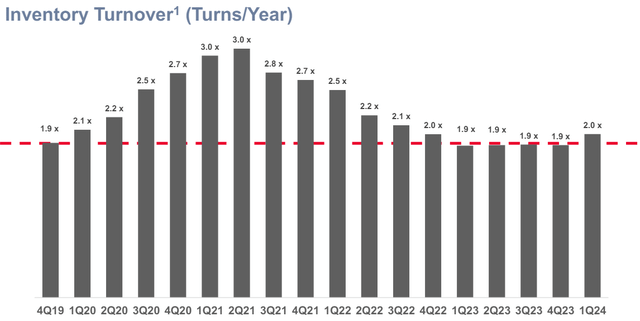

On the topic of inventory management, Holley removed around 12,000 slow-moving or low revenue SKUs from its portfolio and improved the in-stock rate for its top 2,500 SKUs by about 5%. About 40,000 in SKUs have thus been rationalized in less than two years and the company has reduced some 45% of its total finished goods SKUs. However, I think that further improvements in the inventory turnover ratio will be difficult to achieve considering the latter has surpassed pre-pandemic levels. This is likely to have a negative impact on free cash flow going forward and I think quarterly levels could drop below $10 million in the near future. Overall, the results for Q1 2024 were mixed and it seems that most of the low-hanging fruit has been picked up in terms of cost savings and efficiency improvements.

Holley

Future of the company

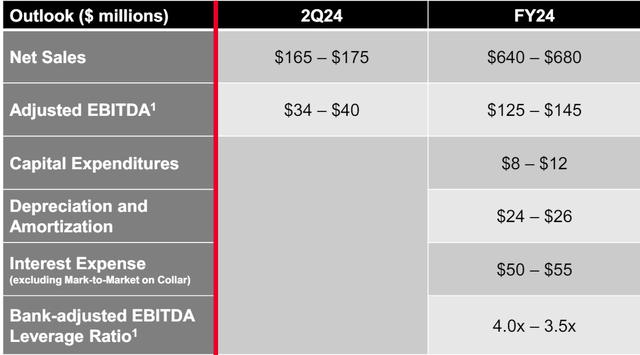

Holley kept its guidance for the full year unchanged, and it still expects to book net sales of between $640 million and $680 million and adjusted EBITDA of between $125 million and $145 million. This suggests that the remainder of 2024 should be stronger for the company as destocking by customers eases.

Holley

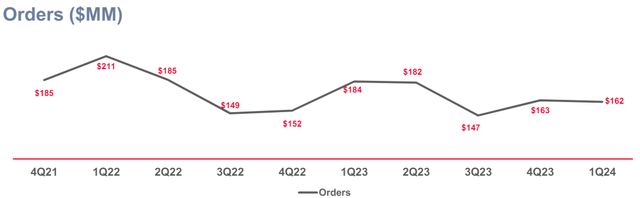

However, I think that the company could be over-optimistic in its expectations, especially regarding Q2. The reason behind my skepticism is the weak order backlog. While orders increased quarter on quarter in the first quarter in 2022 and 2023, this year marked a slight decline which suggests that destocking by customers could be slow or that the market is weak at the moment.

Holley

In my view, net sales and adjusted EBITDA for Q2 2024 could be below $160 million and $30 million, respectively. Holley should release its financial results for the quarter around the middle of August.

Valuation

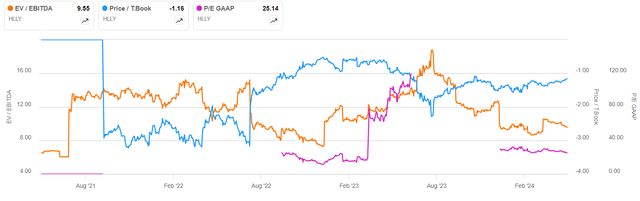

As you can see from the chart below, Holley is currently trading at an EV/EBITDA multiple of 9.6x. While the ratio has often been higher in the past few years, it’s elevated for a business struggling with growth and I’m concerned that the stock could lose momentum over the coming months if Q2 results are mixed like the ones for Q1. Looking at other traditional key financial metrics, Holley also looks expensive based on price to earnings and the tangible book value is still negative.

Seeking Alpha

Investor takeaway

Holley had a tough quarter as a decrease in net sales offset progress in cost cutting and efficiency improvements. The company expects the remainder of 2024 to be better, but I think this could be over-optimistic as orders in Q1 declined compared to Q4 2023. In addition, there doesn’t seem to be much room for further margin improvement and free cash flow could decrease in the coming quarters as the inventory turnover ratio is now above pre-pandemic levels. Overall, this remains a turnaround story, but the lack of revenue growth and the falling backlog are major red flags. My rating on Holley’s stock is neutral.

Read the full article here