Investment Thesis

Diversified Energy Company (OTCQX:DEC) has been an underperformer for the past year, down significantly and approaching a rock bottom valuation. Given the consistent cash flow from operations the company has, I find this pessimism to be unwarranted and think the stock is undervalued. Free cash flow and adjusted EBITDA continue to perform quite well in my view, leading me to believe the market does not appreciate the fundamental improvement of the company. With a prudent hedging program and solid operational results, I think the stock is a buy.

Company Overview

Diversified Energy Company is “an independent energy company engaged in the production, marketing, transportation and retirement of primarily natural gas and natural gas liquids related to its U.S. onshore upstream and midstream assets” according to its website. Basically, they own a bunch of wells and other oil and natural gas producing assets that generate steady cash flows for investors.

They focus on “acquiring existing long-life, low decline producing wells” and “do not actively engage in large-scale, capital-intensive drilling and development programs that seek to capture short-term high production and revenue”. Therefore, the cash flows are relatively stable as those wells sit there and produce natural gas at prices that are hedged with contracts purchased by management.

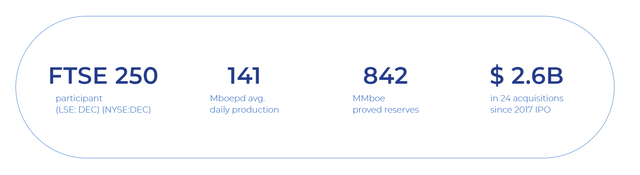

The company owns wells and operates in the Appalachian Basin, with 141 mboepd average daily production and 842 MMboe proved reserves, according to its website. Long term, I think this is attractive as the country still uses fossil fuels to power electricity, so my belief is that production rates should increase as the company continues to strategically acquire more wells.

Website

It is rather interesting to see a company with $2.6 billion in acquisitions trade at a market cap of below $1 billion. I got interested after seeing this discrepancy and wanted to see if the stock was undervalued, or if these acquisitions were truly disastrous and thus deserved a markdown. To my surprise, since the IPO, cash flows have increased from $87 million in 2018 to $410 million for TTM. The stock is now reaching all-time lows, which leads me to believe there’s some mispricing here.

Q1 Earnings Review

The company reported Q1 2024 earnings on May 9, 2024. Here is the brief summary,

- Production essentially flat from 4Q23 adj. production of 725 MMcfepd (121 Mboepd)(A)

- Operating Cash Flow of $107 million, and Net loss of $15 million inclusive of non-cash unsettled derivative fair value adjustments, and non-cash depreciation, depletion and amortization

- Achieved 1Q24 Adjusted EBITDA of $102 million and Free Cash Flow of $74 million

So, investors can see the company is earning solid cash flow, with adjusted EBITDA that roughly matches operating cash flow. Production is relatively flat, but certainly not low enough to justify a stock price decline of over 40% in the past year, in my view. Overall, the quarter showed continued consistency in the cash flow, which is enough to support the dividend of $0.29 a quarter.

The company is also starting to buy back shares at attractive prices in my view. For the quarter, the press release says, “Repurchased ~400,000 shares in 2024 for £3.9 million ($5 million) at an average of £9.74/share”, which translates to about $12.38. Management seems to know that their stock is undervalued and is putting money where their mouth is with their buybacks.

Debt is heading the right way, down “~20% (~$309 million) compared to Q1 2023”. With these fundamentals heading the right direction, I am surprised that the stock trades so low. With strong cash flows, repurchases and dividends, production holding tight, I question whether the market is pricing this one correctly.

CEO Rusty Huston commented in the press release, “I am pleased that our ongoing focus on cost reduction opportunities has translated directly into a 7% sequential quarterly operating cost improvement, allowing us to effectively navigate the current natural gas market headwinds”. Given natural gas trades at around 5 year lows, I am surprised to see the business hold up pretty well. Their cost reduction and hedges seem to be working, with free cash flow of $74 million a quarter could translate into $200+ million of free cash flow for 2024. Management seems to be keen on continuing buybacks, so I feel confident that this quarter demonstrates the fundamental story behind Diversified Energy is still intact.

Hedges Outweigh Low Natural Gas Prices

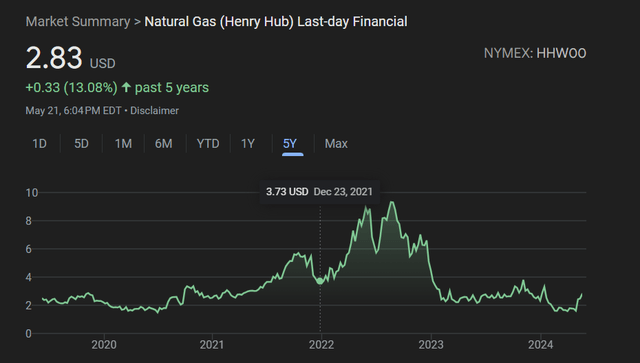

A key reason why I think this stock is misunderstood is because people may think it sells natural gas and therefore will struggle given low natural gas prices. Henry Hub shows a significant decline in price, from as high as $9 in 2022 to below $3 today.

Google Finance

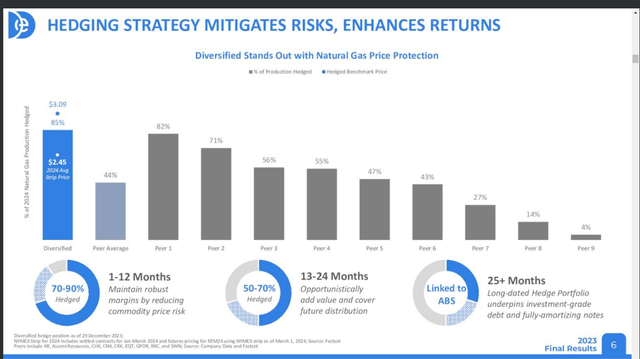

However, after reviewing their financials and investor presentation, I am surprised to see that management has intelligently hedged for this risk and still churns out steady cash. According to their presentation, 85% of their production of natural gas is hedged at prices that are favorable for shareholders. The hedged benchmark price is enough for the company to still be operationally profitable and gush free cash flow.

Investor Presentation, Page 6

Clearly, low natural gas prices don’t mean much to shareholders, as the hedges are doing their magic in keeping cash flow intact. Thus, this may explain why the stock is mispriced in my view, as people do not see that the hedges are outweighing low natural gas prices. In fact, it is precisely in this natural gas market where a company like Diversified Energy should shine. While their peers may be suffering lower profits and cash flow, a hedged strategy should allow Diversified to take the higher cash and reinvest in exciting projects and new wells to take advantage of a potential future upturn in natural gas prices. This strategy speaks well to me because I like the downside protection it gives, and think gives investors stable cash flows in any natural gas market environment.

The quarterly dividend of $0.29 seems sustainable to me, as the cash flows seem to be resilient to natural gas price fluctuations. I think investors are being paid to wait while seeing the company cut costs, focus on increasing production, and hedge cash flows intelligently. Management’s strategy on acquiring “long-life, low decline producing wells” is unique and effective because it allows for a level of certainty in long-term cash flow and looks easier to manage operationally in my perspective. In conclusion, I think the cash flows will continue to be stable, can cover the dividend, and give investors solid income while they wait.

Valuation – $20+ Fair Value

I will base my valuation on the cash flows of the company because I think they are predictably stable and also resilient to natural gas price fluctuations. For 2024, I expect the company to be able to earn at least $200 million in free cash flow, by taking $50 million of free cash flow in the first quarter and multiplying it by 4 to annualize it out. Given the free cash flow came in at $74 million for Q1, I think $200 million in FCF for 2024 is reasonable as $74 million actual for Q1 2024 is much higher than my projected $50 million of FCF a quarter. Also, FCF for 2023 was $219 million according to their presentation, so assuming it can hold at around $200 million seems reasonable as the hedges do their work in keeping cash flows stable.

Divide $200 million in FCF by shares outstanding of ~50 million gets me around $4 FCF per share. Multiply FCF by a below-average P/FCF of 5 gets me $20 per share fair value, with what looks to me incredibly conservative assumptions. Ultimately, the free cash flow is all that matters to me and I see it staying at the very minimum flat for the next year or two due to smart hedging and mature wells that don’t deteriorate that quickly.

I also find it unusual for a company that has historical acquisitions exceeding $2 billion to somehow have a market cap of below $700 million today. Those acquisitions seem to be value-add, as they increased the production capacity and cash flows of the company since they occurred. If I bought $2 billion of wells, oil producing assets and infrastructure, hedging contracts, and suddenly, it’s selling on the market for $700 million today, I’d think the market is severely undervaluing my assets. That’s exactly what, I think, is happening to Diversified Energy at this price, and thus believe the stock is probably undervalued.

Risks

Given the historical acquisition spree the company has gone on, one has to be concerned if management takes a turn for the worse and makes poor decisions about future acquisitions. Goodwill impairments, asset write-downs, and other indicators of bad purchases could dent shareholders’ equity and put the stock lower. Investors need to put some faith in management, as they seem eager and keen on making acquisitions to grow.

Environmental regulations could restrict the output of natural gas, as the country becomes more reliant on renewable energy instead of fossil fuels. In the long term, the company could face a secular headwind as the country shifts to solar and wind energy, and demand for fossil fuels wanes. Future regulations may restrict profitability and make it hard for management to expand operations.

Hedging may not always work, as past performance is no guarantee of future performance. If natural gas prices get super low, even the hedging can only do so much to protect cash flows. At a certain point, gravity takes over and extremely low natural gas prices may make it difficult to sustain cash flows despite smart hedging practices.

The company also has some leverage, coming in at over $1 billion. While not too worrisome, a slowdown in cash flows could lead to increased financial pressure on the balance sheet as management has to keep debt levels under control.

Buy Diversified Energy

Rarely have I seen a company with such good cash flows trading at such a low price. I’m rather impressed by the hedging, mature wells, and overall free cash flow the company generates. Management seems to be pretty smart about acquiring assets that fit the business model, so with over $2 billion in historical acquisitions, I think the market is severely underpricing the company today. Investors should look to Diversified Energy for its solid income and cheap assets at a bargain price.

Read the full article here