Investment Thesis

Best Buy Co., Inc. (NYSE:BBY) is a retail specialty store focused on computing & mobile phones, consumer electronics, and appliances. Although e-commerce has cast doubts on its future, I believe this concern is overblown. This skepticism has caused Best Buy’s valuation multiples to fall below that of its peers, such as Walmart (WMT), Amazon (AMZN), Costco (COST) and Target (TGT).

With the stock selling at around a 35% discount relative to its current price, a dividend yield of around 5%, the anticipated recovery of consumer electronics fueled by AI, and the management’s current strategy to tackle e-commerce challenges, I am convinced that Best Buy is an excellent dividend stock you can buy right now.

Brief FY2023 Earnings Takeaway

Best Buy reported FY2023 revenue of $43.45 billion and a non-GAAP EPS of $6.37. For FY2024, they have guided a revenue ranging from $41.3 billion to $42.6 billion, with an impact of approximately $735 million due to FY2024 returning to a typical 52 weeks, as FY2023 included an extra week, which lifted its revenue by $735 million.

If you account for the lost week’s revenue, Best Buy’s 2024 revenue would be around $42.7 billion to $43.3 billion, resulting in a flat year-over-year performance. With no significant innovation from categories such as Personal Computers (PC) and smartphones, which compose 45% of Best Buy’s revenue, consumers are reluctant to upgrade their current devices. However, this could change with the recent development of AI being localized to personal devices. New AI use cases might be on the horizon that could provide a significant value proposition, overcoming consumers’ reluctance to upgrade their existing devices.

Computing & Mobile Phone Recovery

For Best Buy to resume its growth, it’s essential for the Computing & Mobile Phone category, which constitutes 45% of its revenue, to recover first. This category has experienced elevated inventory due to the recent semiconductor glut and suffered from high inflation, which resulted in its revenue plunging from $20.69B in 2022 to $16.93B in 2024.

What is the path forward for Best Buy to recover from this revenue slump? Generally, the common catalysts for this scenario are an eventual economic recovery, which would help Best Buy’s top line, or a disruptive technological innovation, which could stimulate demand for Best Buy’s business.

However, according to Best Buy CEO Corie Barry, the perception that the industry thrives only during cycles of disruptive technological innovation is a common misconception.

This remark was made by Corie Barry at the UBS Global Consumer and Retail Conference when asked if Best Buy needs a “revolutionary cycle” like the smartphone to do well moving forward.

I think there’s this misnomer that it’s that type of cycle. Like we haven’t seen a cycle like one of the two things you just talked about for about 15 years. Like the digital TV transition was in 2008, and it’s been a while since we like had the phone move. Where we do well is actually in constant innovation. That is a misnomer of the industry.

Corie Barry highlighted that Best Buy’s growth isn’t driven by a “Revolutionary Cycle” such as Apple’s groundbreaking innovation in the smartphone industry. Instead, it stems from the ongoing incremental innovations that follow.

While I agree with this statement, in my opinion, The main problem facing the computing and smartphone category of Best Buy is that recent innovations have been limited to small, sustaining innovations, such as marginal performance and efficiency gains. Customers are reluctant to upgrade because the current performance of their PC or smartphone is adequate for their daily needs. The main reason for this stagnation is the slowdown of Moore’s Law.

Author’s Compilation of Apple Bionic Chip Performance from Geekbench.

This is evident in Apple’s performance progression since 2014. We’ll use Apple’s Bionic chip, which is used in their iPhones, for consistency, as Apple is the only company that has consistently advanced in node wafer technology, thanks to TSMC (TSM). From 2014 to 2019, Apple’s incremental performance gain per generation averaged around 35% to 40%. However, since 2020, the average performance gain has dropped significantly to only around 12% per generation. Consequently, consumers are becoming increasingly reluctant to upgrade, as they can run the same applications or software and have comparable experience using older phones. Newer phones are only seconds faster than the old ones and offer marginally better photos, with differences so subtle that judgment often becomes subjective rather than objective.

This problem is compounded even more by elevated inflation. During economic uncertainty or high inflation, consumers tend to hold on to their PCs or smartphones, impacting the frequency of computing & smartphone upgrades.

While Best Buy may not necessarily require a “revolutionary cycle” to survive moving forward, I believe it needs one to reset the cycle of significant incremental performance gains that can stimulate an upgrade cycle among customers. I think that cycle has now started with AI.

The rise of AI and its potential to enhance our lives has prompted chipmakers like Intel (INTC), AMD (AMD), Qualcomm (QCOM), and MediaTek to integrate AI accelerators into their CPUs. These CPUs are supplied to OEMs such as HP (HPQ), Lenovo, Xiaomi, Samsung, and others, which also incorporate AI into their software or finished products to differentiate themselves. This feedback loop has the potential to further drive AI innovation, replicating the significant incremental improvements seen in the early days of the smartphone.

IDC has forecasted that smartphone shipments will reach 1.2 billion units in 2024 and are expected to increase to 1.3 billion by 2028, with a CAGR of 2.3%. Additionally, for PCs, IDC has forecasted shipments to reach 265.4 million in 2024 and grow to 292.2 million by 2028, with a CAGR of 2.4%

I believe that further innovation in AI and the discovery of its use cases can serve as a catalyst for the recovery and return to growth of the PC and mobile segments, thereby benefiting Best Buy’s top-line growth. Additionally, improving economic conditions can further compound this once consumer spending confidence improves.

The Threat of E-Commerce

Author’s Compilation of Best Buy’s Revenue and E-Commerce Revenue from Public Records.

Best Buy experienced significant growth in its e-commerce revenue during the pandemic. However, as COVID restrictions eased, in-store shopping surged. Additionally, with Best Buy’s product price range, customers often prefer to touch and experience expensive devices like smartphones and PCs before purchasing. As a result, Best Buy’s e-commerce revenue as a percentage of total revenue dropped from 40% to 30%, reflecting customer’s preference for in-store shopping to experience the products firsthand without being restricted by the pandemic. This behavior is further promoted by Best Buy’s extensive network of physical stores across the US.

The rise of omnichannel prompts brick-and-mortar retailers to further invest in their online and physical stores. According to the National Retail Federation, 65% of shopping and 45% of buying still occur in-store. Additionally, 50% of consumers who shop in-store do so to touch and feel the products before purchase.

This consumer behavior on both channels also presents an opportunity for traditional brick-and-mortar retailers like Best Buy to combat the threat of e-commerce by integrating their existing physical stores with their online platforms. This integration aims to offer a much more convenient customer experience throughout the entire journey of buying and using products.

By integrating online and physical stores, retailers can enhance the customer experience by offering services such as consultations before purchase and technical assistance during product usage, both done online or in-store. Additionally, they can provide faster resolution, as repairs can be raised online and performed in-store at the customer’s preferred time, unlike in e-commerce, where customers typically face wait times associated with shipping and handling.

This integration leverages Best Buy’s existing physical stores. With its network of stores and a wide array of products, Best Buy’s stores serve as more than just retail outlets; they act as showrooms where customers can interact with and explore a wide range of smartphones, PCs, and consumer electronics firsthand. This unique advantage sets Best Buy apart from e-commerce giants like Amazon, offering customers an immersive shopping experience.

Along with its omnichannel approach, Best Buy further complements this with its Geek Squad.

Based on a remark made by Corie Barry from Management Presents at BofA Securities 2022. She highlights the importance of Geek Squad not only to generate revenue for Best Buy but also to complement its business through its interactions with customers.

I think we cited a couple of things last week at our investor update. These service interactions result in stickier relationships with our customers. So Damien, you talked a little bit about those who interact with the Geek Squad tend to be more sticky to the brand. They come back to us. Or those who have a consultation, they’re 93% more likely to continue to come back and work with their consultant again.

So it’s not always about the revenue of the transaction in the moment. It is, for us, really important keeping those sticky relationships so that when you have a considered purchase again in technology, we’re top of mind for that.

Geek Squad not only resolves technical issues but also prioritizes building customer relationships and satisfaction. Interaction with customers can result in a sticky relationship, making them more likely to choose Best Buy to buy their devices.

I believe Best Buy’s commitment to customer experience sets it apart in the competitive consumer electronics market. Unlike E-commerce companies like Amazon, Best Buy operates as a specialty retail store focused on consumer electronics, allowing it to tailor its cost structure, internal processes, and company culture specifically to meet the unique needs of its customers. This specialization enables Best Buy to deliver a superior experience.

This specialization, coupled with its immense scale as a consumer electronics retailer, provides a competitive advantage for Best Buy against diverse e-commerce retailers like Amazon and smaller consumer electronics players, respectively.

Takeaway

The US retail industry is forecasted to grow at only 3.2%. To beat the industry average, competitors must strategize to steal market share. Best Buy, as a specialty store for consumer electronics, has differentiated and positioned itself well against the threat of e-commerce and diversified retailers such as Target, Costco, and Walmart by focusing on enhancing customer experience both online and in-store, offering a wide array of products, from low-end to premium products and complementing it with specialized value-adding services like Geek Squad. Additionally, Best Buy is expanding into new segments like Best Buy Health, which has the potential to become a significant revenue stream down the road.

A Sustainable Dividend

Author’s Compilation of Best Buy’s EPS and DPS from Public Records

Before the semiconductor glut and high inflationary environment, Best Buy maintained a robust Dividend Coverage Ratio (DCR) of around 3x. Despite facing challenging times, Best Buy not only maintained its dividends but also raised them, which reduced its DCR to around 1.5x. Given its bright outlook, with the PC and smartphone markets stabilizing, I anticipate an improvement in Best Buy’s performance, enabling the company to maintain its dividend and eventually raise it as its revenue recovers.

Valuation

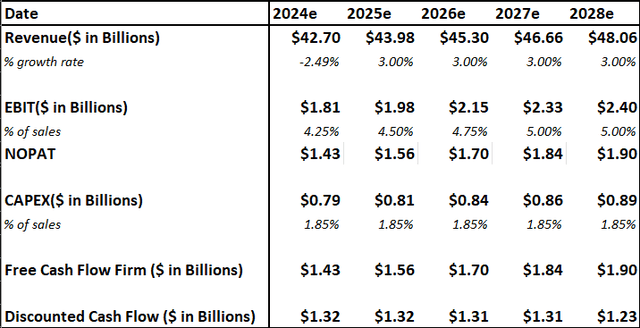

Author’s Future Assumptions – Best Buy

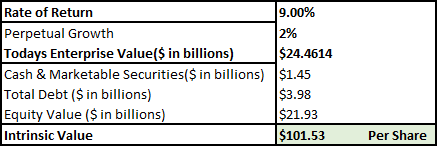

Author’s Intrinsic Value Calculation – Best Buy

Aside from being a generous dividend payer, Best Buy is also consistently buying back its shares. Since 2015, they have brought back around 130M shares. To account for future dividend payments and share buybacks, I will use the Discounted Cash Flow (DCF) method to valuate Best Buy.

For Operating or EBIT Margin, we will assume there will be no significant change in Best Buy’s strategy that can change its cost structure. Therefore, we will use its historical EBIT margin based on its historical revenue to determine its future margin.

Even if Best Buy grows at the industry’s forecasted growth rate of around 3%, it is currently undervalued by approximately 25% to 30%. At its current valuation, I believe it doesn’t reflect Best Buy’s commitment to returning capital to shareholders or its optimistic outlook.

Risk

Consumer Expertise

Younger generations are often more technologically savvy than older ones, posing a significant challenge to Best Buy’s business model. Traditionally, Best Buy has relied on customers seeking their technical expertise to make informed purchases. However, with younger consumers possessing more knowledge of consumer electronics, Best Buy’s technical expertise risks being commoditized. This threatens to erode Best Buy’s competitive advantage, especially when compared to retail giants like Amazon or Walmart, which can offer the same products without the need for specialized technical assistance as Best Buy.

Harsh Economic Condition

Best Buy’s products fall under the category of consumer discretionary items. The company’s business is sensitive to the prevailing economic conditions. During harsh periods, consumers tend to prioritize essential expenditures like food and rent, leading to decreased spending on discretionary items, including products sold by Best Buy.

Conclusion

Despite the incredible rise of e-commerce with Amazon as the clear evidence, I believe Best Buy’s management has positioned the company to focus on things that they can do better than the competition, which is improving customer experience in-store and online and prioritizing customer relationships. With the impending recovery of Consumer Electronics and economic recovery, I believe Best Buy will be able to maintain its dividends and slowly raise them over time.

Read the full article here