IonQ Stock’s Bubble Has Imploded

IonQ, Inc. (NYSE:IONQ) investors who chose to ignore IONQ stock’s frothy optimism in August/September 2023 have been given a memorable lesson in investing. As a reminder, I urged investors to be cautious about IONQ in September 2023 and to closely assess the $20 resistance level, which could invite intense selling pressure. Astute sellers have capitalized on IONQ FOMO, unleashing a battering that might not have bottomed yet.

With IONQ down nearly 60% from my caution, it has significantly underperformed the S&P 500 (SP500). Consequently, IONQ has continued to take out lower highs and lower lows as it entered a medium-term downtrend. In contrast, the S&P 500 hit a new all-time high this week, intensifying the misery on the IONQ bagholders. The short-interest ratio on IONQ stock has also increased markedly to nearly 25%, as bearish investors bet on the continued decline of IONQ.

While I’m optimistic about quantum computing’s long-term growth potential, its near-term applications remain limited. Quantum computing insiders believe we could be two to three years away from broader adoption across several industry verticals. Therefore, they think Quantum Computing’s “ChatGPT moment” could draw closer, even as the debate over its near-term monetization potential is far from over.

IonQ Needs To Scale Fast And Profitably

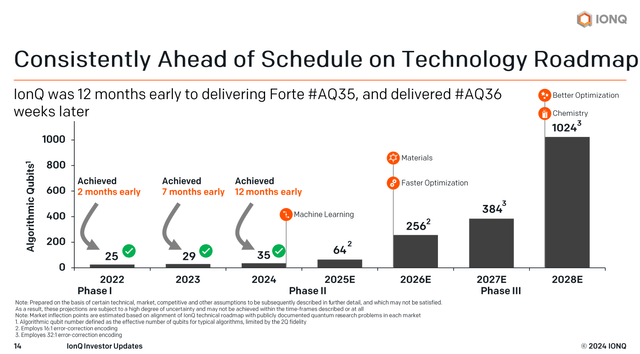

IonQ technology roadmap (IonQ filings)

IonQ achieved its “2024 technical scaling goal 12 months early,” demonstrating its technical capabilities. Furthermore, IonQ’s platform offers 36 algorithmic qubits and is expected to attain the 1024 AQ level by 2028. IonQ management believes the company can penetrate a TAM worth $65B by 2030, corroborating a potentially massive market. Notwithstanding its potential, I assess that IonQ remains in the early stages of its commercialization phase, suggesting an uncertain path toward profitability.

IonQ’s business model is based primarily on its Quantum computing-as-a-service or QCaaS model. Notwithstanding IonQ’s cloud integration with the hyperscalers (Microsoft Azure (MSFT), Amazon Web Services (AMZN), and Google Cloud (GOOGL) (GOOG), it isn’t considered a revolutionary business model. IonQ still faces significant competition from cloud incumbents and also possibly, Nvidia (NVDA). IonQ also competes against IBM (IBM), which is keen to demonstrate its superior technological prowess with its quantum computing technology.

IonQ highlighted its “significant progress in identifying the first potential production applications of quantum computing.” The company also has a “fully operational” manufacturing facility, which was instrumental in producing the “the first IonQ Forte Enterprise system sold to a customer.”

Therefore, it seems unjustified to say IonQ hasn’t made meaningful progress. However, whether it’s enough to justify a reversal in IONQ’s bearish momentum remains to be seen.

Is IONQ Stock A Buy, Sell, Or Hold?

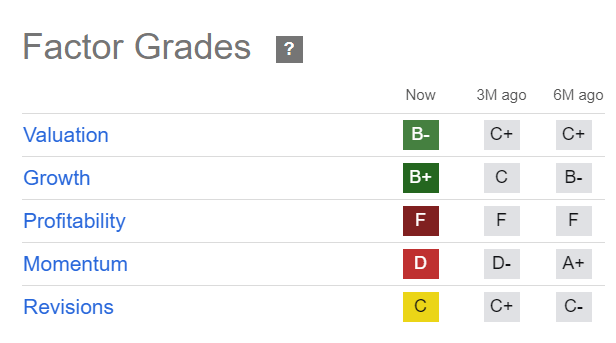

IONQ Quant Grades (Seeking Alpha)

IONQ stock is assigned an “F” profitability grade and a “D” momentum grade. Therefore, it’s clear that the market isn’t convinced (yet) of its ability to commercialize and scale its technology successfully.

Considering IONQ’s relatively attractive “B-” valuation grade, it wasn’t sufficient to attract dip-buyers to return, worsening the relative underperformance and hammering of IONQ stock.

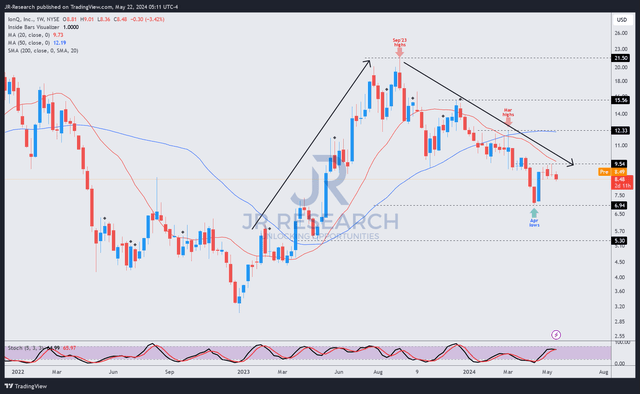

IONQ price chart (weekly, medium-term) (TradingView)

As a price action investor, I always believe that we must correctly assess the market’s dominant trend bias and not attempt to fight against the market. While IONQ was clearly in an uptrend before the bubble burst in September 2023, it has reversed into a medium-term downtrend.

Notwithstanding a reasonable “B-” valuation grade, investors seemed to have reallocated away from IONQ, corroborated by its relative underperformance. I have assessed a possible bottom above the $7 level (April lows). However, the assessed buying momentum failure below IONQ’s $9.50 level could introduce another round of selling pressure, intensifying the pain for IONQ shareholders.

As a result, the market remains skeptical about IonQ actualizing its long-term potential, overshadowing the possibly huge opportunities in quantum computing.

IONQ’s fundamentally weak “F” profitability grade justifies the market’s pessimism, suggesting the downtrend bias could continue. Unless I assess a clear bottom holding above the $7 level decisively, I urge investors to consider reallocating from IONQ.

Rating: Downgrade to Sell.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here