Main Thesis & Background

The purpose of this article is to evaluate the Vanguard Utilities Index Fund ETF Shares (NYSEARCA:VPU) as an investment option at its current market price. The fund’s stated objective is “to track the performance of a benchmark index that measures the investment return of stocks in the utilities sector” and is managed by Vanguard.

As my followers know, VPU has long been a fixture in my portfolio. I use it for diversification, income, and overall stability – and it has indeed served me well over time. But buying selectively can mean everything with this fund just like any other and I thought the time was ripe just over a month ago. In hindsight, this was a great call as Utilities as a whole saw rapid interest in a short period:

Fund Performance (Seeking Alpha)

While it is a feel good exercise to take a victory lap, what is more important today is to consider how well VPU is going to perform going forward. Yes, it has a lot of momentum, but I am getting concerned that these types of gains (double-digits in a month) are not sustainable.

Do I still feel VPU is worth holding in my portfolio? Yes, I do, and I will continue to do so. But I am looking at this with respect to new money. While I like the concept of Utilities, that doesn’t mean I add to it at any price. I won’t pump any idea as a buy without a consideration of the cost – Utilities included. It is in this vein that I think some prudence is necessary and supports a downgrade to “hold” for now. I will discuss the reasons why in detail below.

Why Have Utilities Been Soaring Of Late?

To begin, I thought I would take some time to reflect on the why behind why VPU has been an alpha-generator in the short term. This is an important exercise because this helps us gauge whether or not the momentum can continue. The simple fact is that VPU’s rise (and Utilities more broadly) isn’t due to just one idea, but multiple.

The first is that markets as a whole have been rising. This includes US large-caps (notably Tech), developed markets, emerging markets, high yield debt, you name it. So Utilities have been caught up in this bull-run and that has certainly helped. A primary catalyst behind this broad-based rally has been that inflation in the US has been trending lower. While I am a bit of a skeptic on how this will influence the Fed near term, the market disagrees with me for now and views this decline as a buying opportunity:

Inflation Readings (US) (Bloomberg)

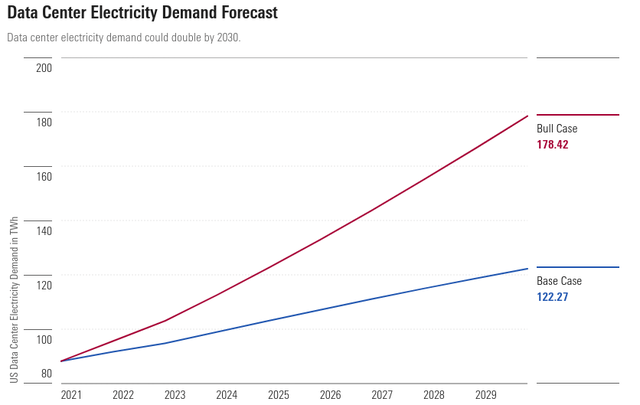

A second reason has been a re-thinking of investors about the broader industry. This has turned into an “AI” play without the AI. What I mean is, investors are now contemplating that Utilities are going to benefit from the AI boom because electricity demand is going to soar. The companies that utilize machine-learning and those who consume it are going to need more internal bandwidth to develop and produce this service. The net result has been that market participants have begun forecasting aggressive demand for electricity in the years ahead:

Electricity Demand – Forecast (Bull and Bear Cases) (Morningstar)

This is certainly a good sign in that it means Utilities – often considered a boring sector – are front and center of one of the biggest plays of 2024 thus far. The “AI mania’ has helped propel Tech stocks higher, and it is nice to see Utilities be a beneficiary of it as well.

A third reason is that economic growth has been slowing in the US. This may seem counter-intuitive, but it helps explain why defensive areas – like Utilities – have held up well in the prior months. When economic concerns mount, investors are drawn to the stability that utility providers offer given their services are necessities, not “wants”. This slowing growth dynamic will probably continue in the second half of 2024 (my personal view) and that is likely driving some of the recent buying in this corner of the market:

GDP Growth (USA) (US Bank)

The bottom-line is that Utilities have been rising for some legitimate reasons and that is something to keep in mind. This reality is why I will continue to own the sector – including VPU – and why I am not a “bear” more broadly. But that doesn’t mean I love the risk-reward proposition for new buy-in points right now either. I have concerns, supporting a neutral view, and I’ll get to those next.

Is This Really An “AI” Play?

My primary concern has to do with one of the factors mentioned above. The “AI” frenzy has been driving some momentum buying in many big Tech names – but it has found its way into the Utilities corner too. I don’t want to completely discount this narrative. After all, if electricity and other data center demands rise, then surely that is good for the providers of that service. So, yes, this is a positive catalyst.

But my concern rests with how optimistic the market has become. To be fair, I do see the AI-demand as a bullish catalyst for the sector. That’s a very reasonable outlook and this is a multi-year catalyst for sure. But will a rise in electricity demand really push utility stocks higher and higher in a straight line? I doubt it, which is why I would manage expectations here.

A double-digit pop for this sector in a 1-month timeframe is not common and the AI hype is going to fade at some point even if the longer-term story behind it is positive. I simply wouldn’t count on another double-digit leg up in the months ahead, and that is why I am downgrading my outlook. It wouldn’t be prudent of me to jump in here with fresh cash and try to ride this wave higher when the optimism seems to have been built in at current levels.

Be Aware Of Debt Burdens

Another factor to consider is that the Utilities sector is saddled with above-average debt loads. This makes the inflationary environment a disproportionately bigger headwind for VPU and other utility funds because elevated borrowing costs present a challenge for this sector. When debt levels are high, lower interest rates are obviously preferable. With inflation remaining higher than the Fed’s target, this means the central bank is unlikely to move on rates soon, in my view. To me, this supports being selective on VPU – we need to understand that higher borrowing costs will remain a risk going forward.

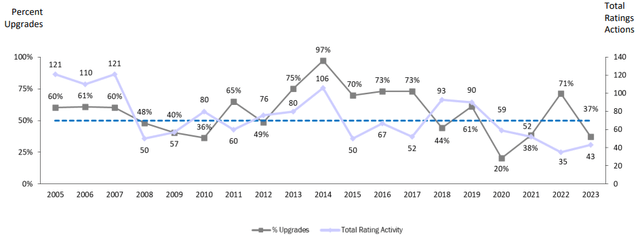

This isn’t something that I worry about in isolation. One only has to look to US credit ratings agencies to understand this is a macro-concern for the sector. With investor optimism over rate cuts in 2023 failing to materialize, these agencies have been consistently downgrading, rather than upgrading, publicly own utility company’s ratings:

More Downgrades Than Upgrades (Public Utility Companies) (US) (Edison Electric Institute)

The significance is clear – if something doesn’t change, these are companies that could run into some fiscal challenges in the years ahead. Will things change? Probably. I doubt we will have an inflationary environment two years from now that is the same as today. Similarly, I doubt interest rates will be at current levels in 2025 or 2026. So I’m not trying to be alarmist here. But prudent investors don’t ignore credit ratings agencies, and in this case, there is reason for caution. Keep this in mind when evaluating how big of an allocation you want to this arena.

Why Own This Sector? Diversification

I want to balance out this review again by emphasizing why one would want to own Utilities – and VPU by extension – for the long term. As my followers know, this is a fund (and sector) I have long championed and the reasons are multi-fold. So while I am exercising some caution here, I am not raising any major red flags or trying to be overly bearish. Quite the contrary. I will continue to own VPU and see the merit to buying it. But this review isn’t about cheer-leading or pumping a fund I own, it is about giving readers some insight into what the short-term risks are and support why they should weigh them carefully.

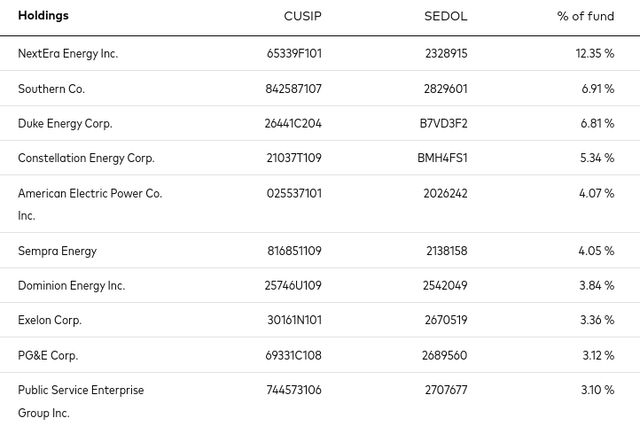

But one reason why I bought VPU years ago remains true to this day. That is diversification. The fund owns many stocks that are in the S&P 500, but are lightly weighted in that index. The top ten holdings in VPU are not notable holdings for funds that track the S&P 500, so that in and of itself gives investors some balance to their portfolios:

VPU’s Top Holdings (Vanguard)

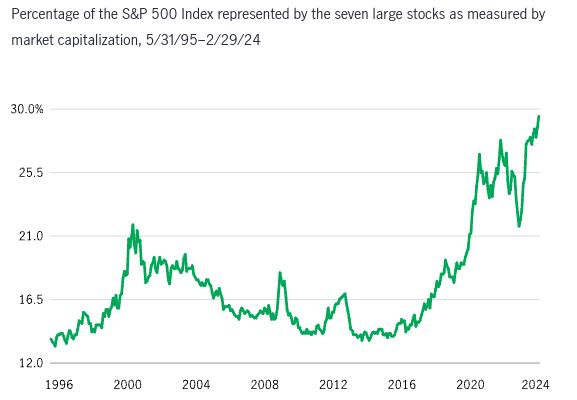

Expanding on this point, I see the usefulness in this ETF even more so today than ever before. That is because the S&P 500 has continued to get more and more concentrated in just a handful of names. In fact, the top seven names in the index make-up almost 30% of the weighting – well above the historical norm for an index that generally been top heavy – just not that much!

Mag 7’s Percentage of the S&P 500 (FactSet)

The fact remains that branching into sector ETFs in areas like Utilities, Energy, Industrials, Real Estate, and others remains top-of-mind for myself and many investors due to this consolidation within the S&P 500. When one buys a passive S&P 500 ETF or a “large-cap” US index, they are essentially getting massive exposure to a small number of names. This can be good when the trade is working – as we have seen over the past two years. But concentration risk can work both ways, highlighting the need for diversification and balance. VPU helps to provide this to an overall portfolio and that is why I own it.

Bottom line

Utility stocks have been roaring of late and that has been a welcome development for me. VPU has produced a strong gain since I amplified my position and I wish I could bank on continued gains in a similar manner.

But that type of outlook doesn’t bode well for the prudent side of my brain. As the famous saying goes: “only fools rush in” – and I don’t want to be a fool. When I see outsized returns on a sector that is traditionally not prone to such big moves in a short time period, I think the case is pretty clear that being aggressive here is not the right move. As such, I am downgrading my outlook on VPU to “hold” and I believe readers should approach new positions very carefully at this time.

Read the full article here