Dear readers/followers,

In this article, I’ll provide an update on K+S (OTCQX:KPLUY) (OTCQX:KPLUF), a fertilizer business and salt company that has seen a considerable turnaround in its overall fortunes and the volatile upswing that characterized earnings for the past few years. Now it’s on the way down. Since my last article, I’ve seen a decline of a few percent, but it’s not a “failure” in a way that would make this investment an unsuccessful long-term play. In fact, I am still positive about the business and believe that there is considerable upside to be had here at this time.

My last article at this time is from a few months back and is one you can find here. In this article, I make it clear that K+S is a solid company, and despite the current macroeconomic trends, I consider the company as a solid investment with potential upside.

We’ve now seen around 2-3% negative RoR since my last piece – and I am still not worried about this In any way. At this point, I have been covering the company for almost two years, and while I cannot say that this has been my best investment “on file”, I believe there is much to be said for the potential upside here.

It’s difficult to say just how low this company could potentially go because we’ve already seen It decline quite significantly over time. SDF is the native ticker here and the company’s fundamentals are, for the sector, (not in general when looking at everything) absolutely superb.

SDF has a BBB rating, and while it does have a very complex set of earnings trends, I see a good chance for an eventual upside here.

Let’s look at the latest results and what sort of upside we can materialize here.

K+S – Plenty to like, just a lot of volatility as well

Since my last coverage, not only K+S has seen a problematic trend. Fertilizer companies overall have been in a downward spiral due to temporarily worsening fundamentals, related not only, but in part to macroeconomic concerns. The problem was also that 2022 was an absolutely record year – not just for this business, but for most fertilizer businesses worth their salt if you pardon the expression. Even the high energy prices suffered by many of these businesses could do nothing to downplay the record-high sales prices and product prices enjoyed during the period.

The latest results we have are 1Q, but first off, we need to understand that this is a company that is quickly climbing towards an annualized EBITDA of €1B at a margin of 20%+, with adjusted free cash flow of half a billion a year, based on revenues of almost €4B.

Those are, while not record numbers, absolutely stellar, and the business is one of the best potash and salt companies around – and the largest as well.

K+S IR (K+S IR)

The company serves customers from two industries, the agriculture and the industrial sector through potassium chloride (or MOP), and fertilizer specialities, and also guide farmers to getting the best sort of crop qualities.

In addition to that, the company produces for the industry a huge amount of de-icing salt and other industrial solutions, about half the revenue of the agri segment.

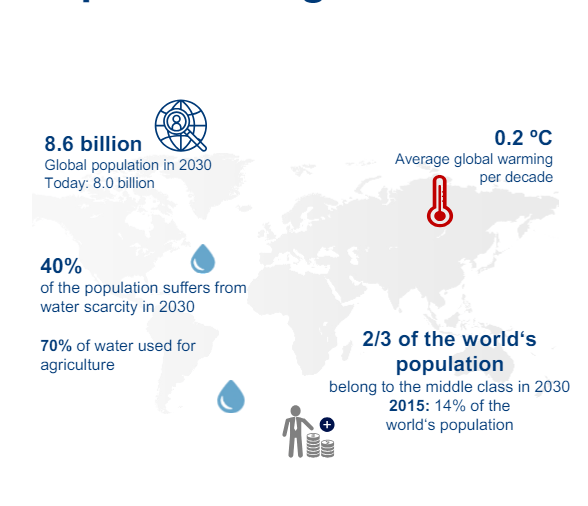

K+S operations are completely in line with current global megatrends. What global megatrends we are looking at here are things like the population growth, and the average global warming increases- not because of climate change, but rather due to changes in arable land, water scarcity, and the amount of freshwater having to be used for the agriculture sector. I’m interested in concrete, not speculative causality and data points – and that is what Is what we have here.

K+S IR (K+S IR)

Also, there is a growth in the demand for salt, especially in Asia, for a variety of purposes. The company is also a play on infrastructure.

The company is, however, a good play overall because the process of fertilization among other things the company’s products and services, is an absolute necessity for the process of achieving high yields over a longer period of time. That is because the soil is usually deprived of nutrients after a few cycles, which is why it needs to be compensated by the addition of additional substances – i.e. fertilization.

K+S IR (K+S IR)

The company manages a large number of impressive sites, from Bethune to Zielitz, with Werra as one of the main investment projects for the company for the near future.

K+S IR (K+S IR)

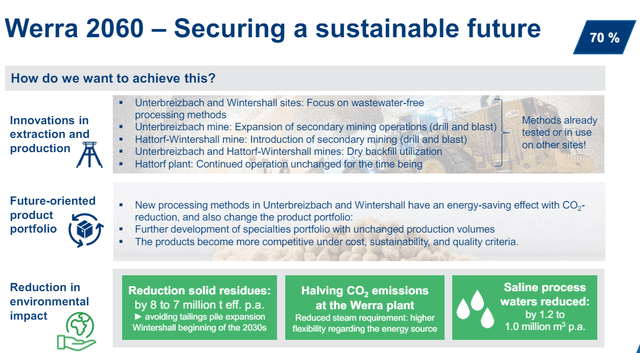

CapEx in Werra is expected to be high all the way until 2027, at which point the company’s investments will be done, and turn to positive impact. The company is looking at a CapEx amortization period of less than 10 years, which is impressive here.

The core of the company will remain farming and agriculture. But there will be moves towards renewables and green energy (at the production sites, not that the company will start to become a producer), with increased waste management, re-use of the company’s vast subterranean mining complex (biotech production is one use being considered), under a very strong management. This remains a positive.

The company has a fairly progressive dividend policy for a German company. This includes 30-50% to shareholders in a combination of buybacks and returns while maintaining very conservative leverage at no higher than 1.5x. Dividends have really been “up and down” for quite a while, €1 2023, and €0.7/share for this year, which currently marks a dividend yield of 5% – which is actually extremely solid, given where fertilizer businesses have been heading in terms of their dividends.

To say that K+S is the best investment in the sector would be an exaggeration. To say it’s a solid investment with an upside though, that’s a different story and a different stance. Given the upside inherent to the stock relative to the company’s risk profile, my conviction is high that this company is in fact a solid investment – despite the current macro.

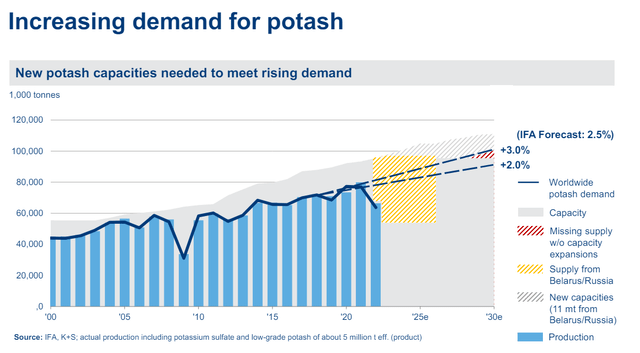

The 1Q quarter did not see any surprises. The market situation remains in flux, with an exclusion of Russian potash capacities, meaning much more is now being carried by NA and EU. There is also an ever-increasing demand for potash globally, and without the supply from Russia and Belarus, there is no way that the global demand can be met as things are looking right now, according to forecasts.

K+S IR (K+S IR)

Given this situation, not only do I believe that things are going to improve, I think that pricing for potash is going to improve and rise materially – and I believe we’re already seeing the beginning of this at this time.

K+S also remains the third-largest supplier (single company) in the entire world, though only about a third of the size of the massive structure Canpotex, which is the combination of Nutrien (NTR) and Mosaic (MOS).

Overall, I say that this company remains extremely solid, with a very good upside, but only if you look at it over the very long term.

Let me clarify and make this upside more concrete for you.

The upside for K+S – Plenty to like over the long term about 5%+ yielding fertilizer

The fact is, that the potash market needs even more capacity to meet the increasing demand for potash around the globe. With a demand growth until 2032, the current supply won’t be enough to meet it here, and the current calculation is about 4 million tonnes short. This creates a very attractive pricing situation.

On the forecast side, SDF, or K+S, is expected to grow its results and annual trends in both 2025 and 2026 – though not yet in 2024. 2024E is expected to come in around €0.31, and a cut to the dividend. However, this is then likely to reverse to a €0.6/share adjusted EPS and over €0.8/share in 2026E, meaning this is a company that’s likely to grow. (Paywalled F.A.S.T graphs Link)

There are two problems with this assumption based on the forecast accuracy and earnings stability of the business. First of all, this company is extremely hard to forecast properly. By “extremely hard”, I am referring to the fact that the company only hits its targets by either beating them, 25% of the time or as the rest of the time, missing them entirely with negative forecasts misses. This company has not, during the last 10 years, even once hit the forecasts targes with a 10-20% margin of error – which is quite a feat. It shows just how volatile the sector is, and how difficult forecasting the business here is.

I believe the improvement in EBIT will come both due to price and demand increases, as we’re seeing the initial moves here in Q1 as well as improved fundamentals for the sector. Even if K+S is not as good as Yara – and it’s not in my view, or I’d own much more than I am – and the yield isn’t as clear or as good, there’s still an upside.

S&P Global analysts consider the company to be a clear “BUY” here. From an average share price from a range of €20 to €30/share, we’re now down to a range of €10 to €20/share with an average of €16/share. However, out of 16 analysts, 9 have the company at a “BUY” or similar positive rating, implying a 13% upside to a very conservative price target for the company. Very conservative in this case implies less than 0.7x to sales and less than 0.7x to revenues. Peers to K+S in this case come in the form of Nutrien, Symrise, Mosaic, Covestro, Yara and others – many of which I cover on a fairly regular basis here on Seeking Alpha. These companies trade at wildly varying multiples and numbers – with NTM P/E’s going from as low as 10x to as high as 33x, with K+S at around 26.15x, and many of the other companies close to K+S, such as Mosaic and Nutrien being above 30x P/E. (Paywalled T.I.K.R. Link) – but also higher than 20-25x on average. This is also why I have a relatively high price target for the company and consider this to be valid – both the fundamental upside, but also the comparative upside based on where peers typically trade.

Overall, I want to convey that the company continues to have a good fundamental and operational upside, but I expect this company to take some time to get there.

Therefore, to invest here, you should be prepared to wait for a number of years, but provided you do this, I can see a share price of €25/share.

Thesis

- K+S is one of the largest players in Potash remaining after Russia and Belarus are sanctioned off to most of the modern world. This makes this German fertilizer and salt giant an attractive play, and a good time for the company to flex its expansionary muscles. Despite a lack of an IG rating, I view this as an interesting play.

- In the right environment, which we have today, it’s not inconceivable that the company could rise closer to its fair value, which I view as being valid close to €25/share.

- I now have at my conservative €25 PT based on conservative growth rates, mixed NAV/peer valuations, and conservative multiples and forecasts. This is above the average, but I consider it fair as of May of 2024.

- I, therefore, view it as a “BUY” here, albeit a characteristically “speculative” one.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

My one change is that I now view K+S as “cheap” here, fulfilling all of my criteria.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here