Co-authored by Rida Morwa.

Investors love to parrot the phrase “Buy low, sell high,” yet so many fail to do it. Step one of “buying low” usually means buying something that isn’t popular. You aren’t going to find me arguing that the market is efficient; however, the reality is that stocks that are trading at a low valuation are usually trading low for a reason.

Often, the best returns in the market come from buying distressed sectors. Investors willing to “stick their hand in the fire” can often walk away with significant gains. Today, I’m going to discuss a company that is trading at an extremely low valuation, and the reasons it is are clear. The sector is distressed, there are some real operational challenges and high interest rates are costing real money, resulting in lower earnings. There is no mystery as to why the price is low right now.

What about the future? For investors who are willing to look ahead and see beyond the current challenges, the potential upside is significant.

Unwanted Office Space

The woes of commercial real estate are all over the news, and the sector that is perhaps the most negatively impacted is office.

Brandywine Realty Trust (NYSE:BDN) is an office REIT. Office is a sector that has been hit hard by shifts in commercial real estate. The combination of “work from home” having companies rethink their office space needs, high interest rates impacting real estate values, and the ability of some companies to finance office buildings has put a lot of stress on the sector.

Due to these risks, we have limited our exposure to office space in the HDO Model Portfolio. However, for those who are willing to accept the volatility, there are some “diamonds in the rough” that are trading at extraordinarily depressed prices, while paying out likely sustainable and very high yields – one example is BDN.

The Financial Impact Of High Interest Rates

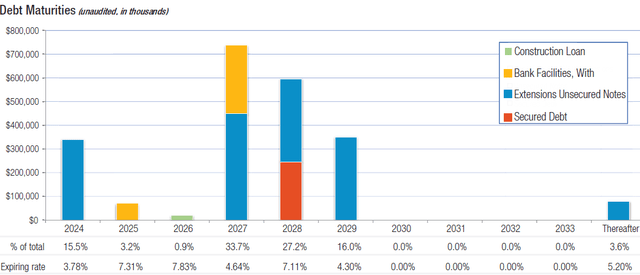

Interest rates negatively impacted BDN as it had debt maturities in 2023 and 2024 that were refinanced at higher rates. Source.

BDN Q1 2024 Supplement

After the quarter end, BDN issued 8.75% Notes maturing in 2028, which is being used to refinance its 2024 maturities. That is a significant increase in interest rates, and the headwinds that BDN experienced to FFO (Funds From Operations) in 2023 and 2024 are primarily attributable to increased interest expense. This is why BDN opted to reduce its dividend in October 2023.

The good news is that this impact is now known and is incorporated in current guidance. BDN has no significant debt maturities until 2027, and the small maturities they have before, are already paying +7% rates. Then in 2028 and 2029, BDN will have an opportunity to refinance the high-coupon debt it is taking out now. It is very likely that refinancing that debt will be a benefit to FFO, just like taking it out now has been a headwind.

The Outlook

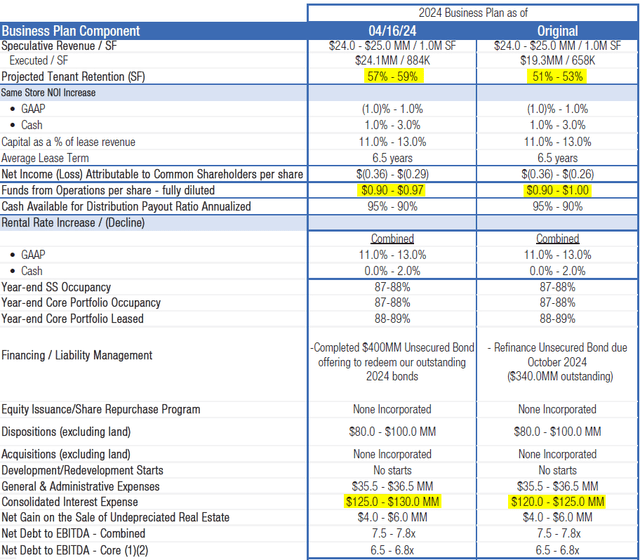

One thing we love about BDN is that management has some of the best disclosure of its guidance in the business. Instead of just providing the target FFO number, management provides a detailed breakdown of each assumption that goes into it. Each quarter, it compared the current expectations to the original expectations. As a result, we have the opportunity to see what is going right, what is doing better, and what isn’t.

2024 Guidance (BDN Q1 2024 Presentation)

The changes are highlighted: The FFO range was tightened toward the low end, and this was due to a $5 million increase in projected interest expense. The only other change is in tenant retention, which BDN now expects to be 57-59%, an increase from 51-53%. Tenant retention is the percentage of tenants with expiring leases who are choosing to renew.

This increase is a positive development but doesn’t move the needle because BDN doesn’t have many leases expiring. Only 3.8% of its square footage is expiring this year. 2025 and 2026 are also in the mid-single digits, a very manageable pace.

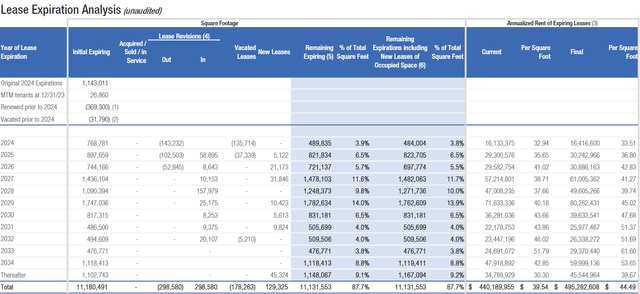

Lease expiration schedule (BDN Q1 2024 Presentation)

The reason BDN has so few leases expiring in the next few years is because of COVID. During COVID, the first thing BDN did was start aggressively marketing to their tenants, encouraging them to extend their leases. Management’s thought back then was to lock down their portfolio and make it as sustainable as possible. Back then, nobody knew how long COVID would last, but BDN knew it didn’t want a big glut of leases expiring. This sacrificed some short-term FFO, but given what we know now, having relatively few leases expiring today is very positive.

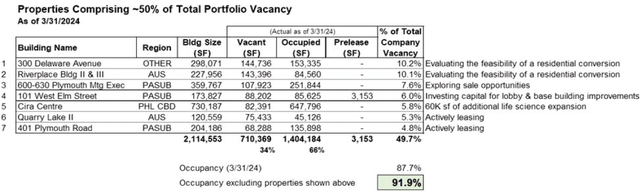

Dealing With Vacancy

For an office REIT, vacancies are expensive. Even when a building is vacant, there are costs associated with basic maintenance, insurance, taxes, and if partially occupied, the costs of maintaining the common areas.

BDN’s occupancy is quite healthy compared to the national averages. In part, this is due to their efforts in extending leases, partially because BDN primarily focuses on “Trophy class” and “Class A” office space, which has seen demand hold up better, and partially it is because BDN is highly concentrated in a couple of markets. BDN focuses primarily on Philadelphia and Austin.

BDN Q1 2024 Presentation

As a result, BDN’s vacancy is highly concentrated in a few assets. BDN has 69 operating properties and 7 of those account for nearly 50% of vacancies. Management outlined its plan for each of these properties:

BDN Q1 2024 Presentation

27 of BDN’s buildings are 100% occupied. Resolving the buildings that have significant vacancies will reduce costs, even if the ultimate solution is to sell the properties that have persistently low occupancy.

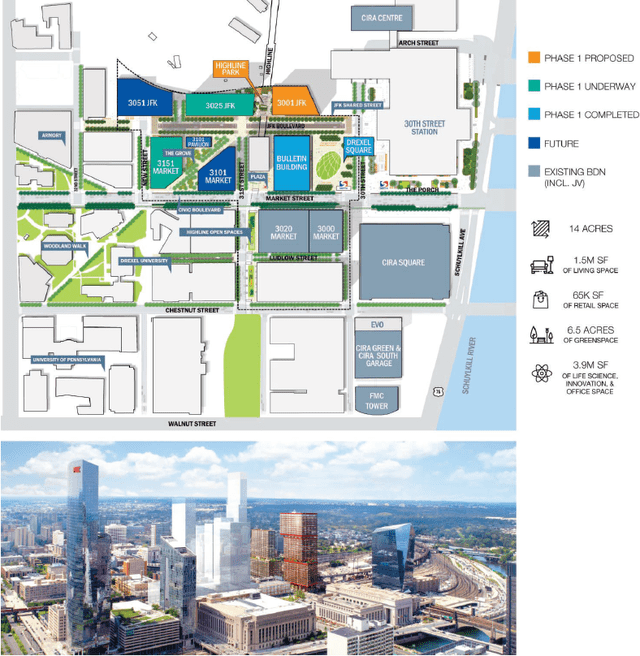

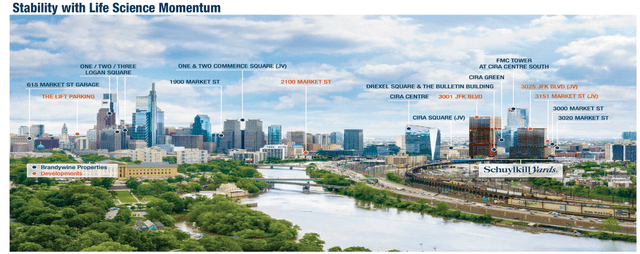

Developing For The Future

BDN’s future is primarily tied to its development plans. BDN is the master developer of two huge projects. Schuylkill Yards is a development centered around Drexel University in Philadelphia, which will include 1.5 million square feet of residential, 65,000 square feet of retail, 3.9 million square feet of Life Science office/lab space, and 6.5 acres of parks.

Schuylkill Yards (BDN Q1 2024 Presentation)

This development is literally building the skyline of Philadelphia, and adding on to its already impressive ownership of a large portion of Philadelphia’s skyline.

BDN Q1 2024 Presentation

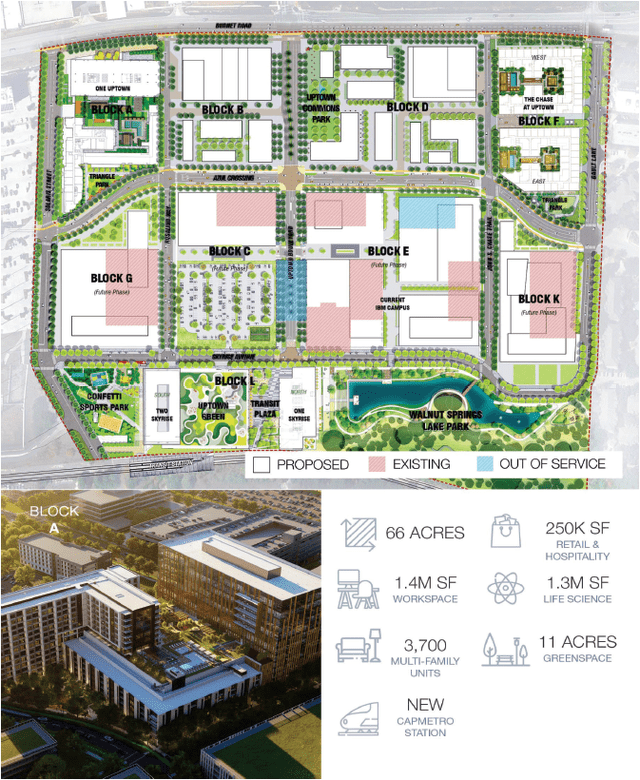

The other major development is in Austin. Uptown ATX was a corporate campus of IBM, and BDN is transforming it into a 66-acre mixed-use development that will include 1.4 million square feet of workspace, 1.3 million square feet of life science space, 250,000 square feet of retail, 3,700 residential units, and a new metro station that is scheduled to open in 2026.

Uptown ATX (BDN Q1 2024 Presentation)

Thanks to COVID and a high cost of capital with recent high interest rates, the pace of these developments is slower than it might have been envisioned five years ago. However, BDN keeps making forward progress.

In real estate, there is a saying that the three most important things are “location, location, location.” The locations of these developments are extremely valuable in two rapidly growing cities. BDN already owns the real estate, it has already put in a significant amount of the infrastructure, it has already done the legwork of working with government agencies to get the required permits and zoning. It has completed the initial buildings in both developments with positive leasing results.

The thing about development is that the initial buildings are the most expensive to build and lease for the lowest amounts. Future buildings hook into the same infrastructure, and the success of the first buildings encourages leasing of the new buildings. Tenants want to be in areas where others are already successful and will pay a premium to be there. On the other hand, identical spaces in an area that isn’t successful and has high vacancy can’t be leased for any price. BDN isn’t developing one building, where it is dependent on its neighbors to keep the neighborhood nice. It is building the entire neighborhood from scratch.

Development has been occurring slower than anticipated before COVID, as the macroeconomic situation has been unstable, to put it mildly. However, BDN has continued pushing forward and the value being created is every bit as immense.

Conclusion

We won’t be adding BDN to the HDO Model Portfolio because of the risks in office space. It is a difficult sector right now. But for those willing to take on the risks, BDN is offering a +12% yield that appears to be comfortably sustainable and there should be significant price upside as interest rates decline. If the Schuylkill Yards and Uptown ATX developments are successful, BDN has a path to substantial upside.

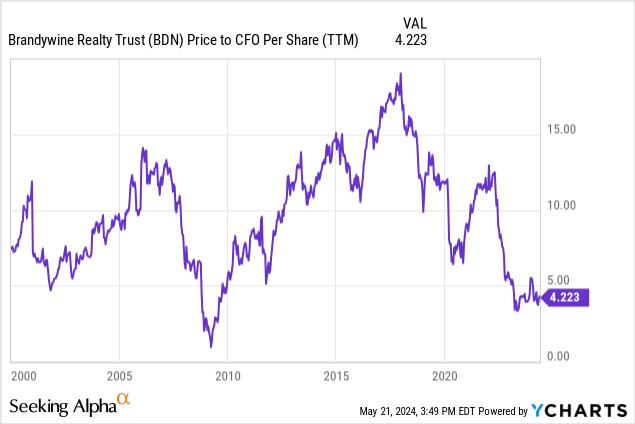

In terms of valuation, Brandywine Realty Trust is trading at the lowest valuation it has since the GFC. Which, in hindsight, was a fantastic buying opportunity.

Going into 2025, it is reasonable to expect FFO to stabilize and return to growing. As the Schuylkill Yards and Uptown ATX developments make progress, BDN should see FFO/share climbing at a much faster pace than it has seen in decades.

BDN is working its way through the current challenges, and the developments it has focused on are still very relevant in a “work from home” world if that trend survives. BDN pays a 12% dividend yield right away, with the potential to double or even triple in price if its valuation returns to historical levels.

Read the full article here