Introduction

Three months ago, I wrote an article on Sea Limited (NYSE:SE), highlighting that the market is still in ‘disbelief’ and that the stock has much more room to run despite its sharp rally.

Since that article, the stock is up another 20%, and since its bottom in January, it’s up more than 100%.

Considering the stock’s recent run, bulls might feel the urge to take some profits and reinvest the proceeds elsewhere.

But before you hit that sell button, let me talk about why it might be a better idea to hold on to, or even add to, SE stock. Here are 8 reasons to remain bullish on the Southeast Asian tech conglomerate.

Reason #1: Unprecedented Scale

Without a doubt, Sea is one of, if not, the most dominant tech company in the whole of Southeast Asia. The holding company operates three businesses namely Garena, Shopee, and SeaMoney, all of which are leaders in their respective categories.

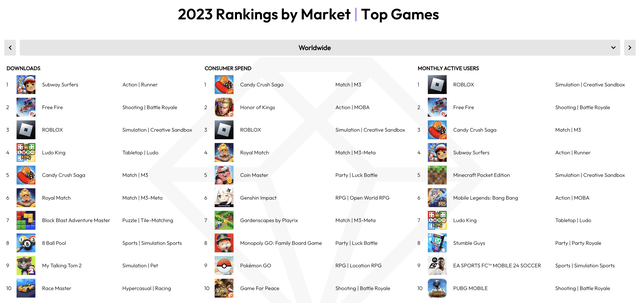

Garena is the leading mobile game developer and publisher with games such as Free Fire, Call of Duty Mobile, and Arena of Valor in its portfolio.

According to data.ai, Free Fire holds the #2 spot in terms of the most downloads and monthly active users in the mobile game category in 2023. In addition, per SensorTower, Free Fire was the most downloaded mobile game worldwide in Q1 this year.

data.ai

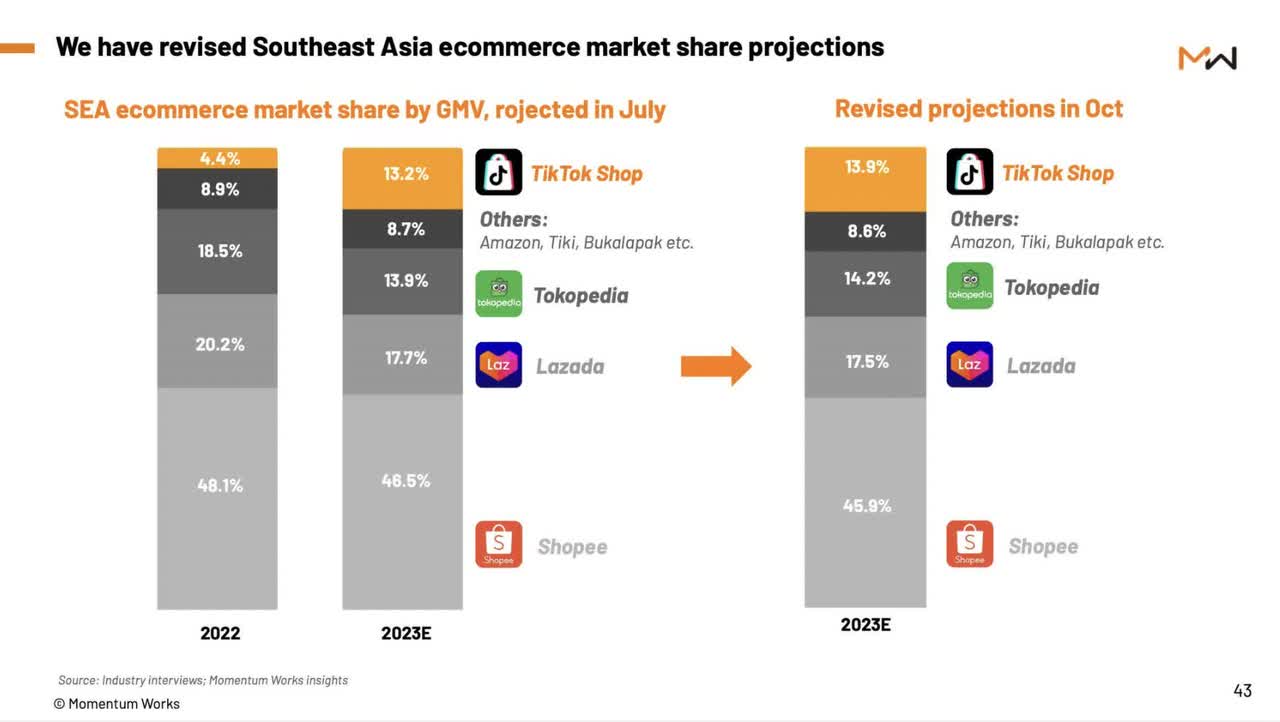

Shopee, the leading e-commerce marketplace in Southeast Asia, holds an estimated 45.9% market share in Southeast Asia, which is nearly triple its closest competitor, Lazada. As exemplified by Amazon’s (AMZN) success story, size in the e-commerce industry matters.

Momentum Works

SeaMoney, the group’s fintech arm, is also building a substantial market position. SeaMoney offers various forms of financial services via the Shopee app, including digital wallet (ShopeePay), BNPL (SPayLater), and financing (SPinjam). SeaMoney also offers digital banking solutions and lending services off-Shopee, including SeaBank and MariBank.

Combined together, Garena, Shopee, and SeaMoney make such a formidable force in Southeast Asia. More importantly, its massive size bestows the tech conglomerate with powerful network effects and efficient scale moats that protect the business from smaller competitors. In addition, it enables Sea to sustain and expand its leadership position over time.

Reason #2: Southeast Asia’s Digital Transformation

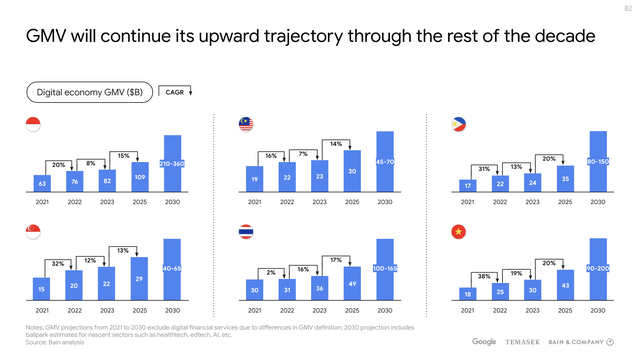

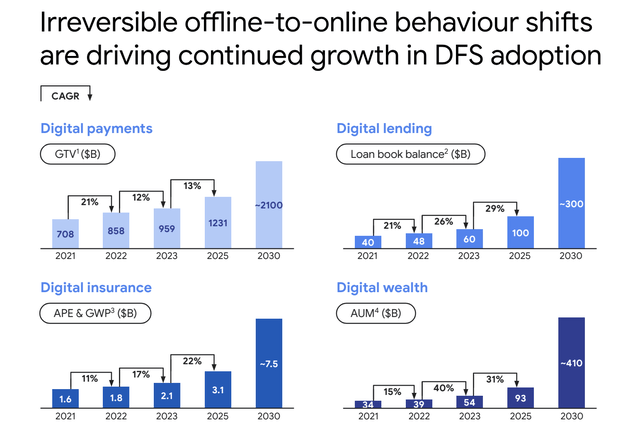

Having a dominant market position in Southeast Asia also means that Sea will be in a prime position to capitalize on the rapidly growing digital economy in the region.

As you can see below, the digital economy of each of the major Southeast Asian countries is expected to expand even more throughout 2030. This secular trend, which includes e-commerce and fintech, will be net positive for Sea.

e-Conomy SEA Report 2023

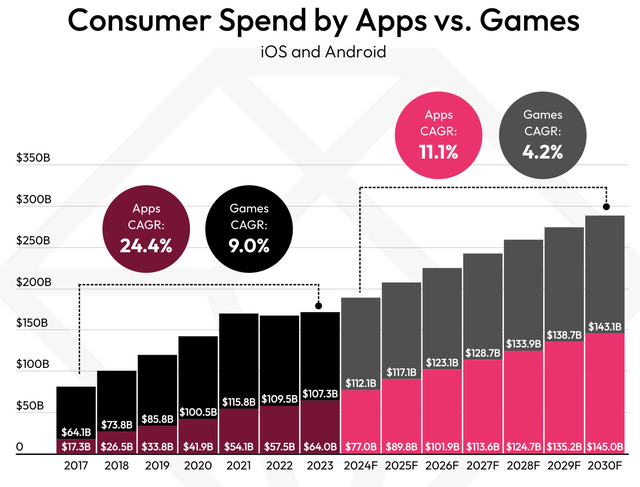

Moreover, worldwide consumer app and mobile game spending are expected to grow steadily over the next few years, at an 11.1% CAGR and 4.2% CAGR, respectively. This should be a tailwind for Garena.

data.ai

Put simply, Sea still has a long growth runway ahead as each of its three business segments enjoys strong tailwinds from the growth of the Southeast Asian economy.

Reason #3: Shopee’s Dominance

As mentioned earlier, Shopee is the largest Southeast Asian e-commerce platform at an estimated 45.9% market share. This figure was actually revised down, most likely due to TikTok Shop’s growing presence in the region.

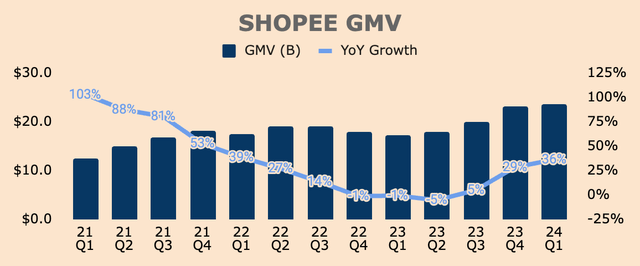

However, Shopee’s growth over the last couple of quarters shows that Shopee has been gaining market share. In Q1, Shopee’s Gross Merchandise Volume (GMV) was $23.6B, a record high for the company. Q1 GMV growth was 36% YoY, an acceleration from Q4’s already-robust growth of 29% and last year’s negative growth of (1)%.

Shopee’s growth rates in the past two quarters were much better than expected so this should comfortably put its market share above 50%, further solidifying its leadership position.

Author’s Analysis

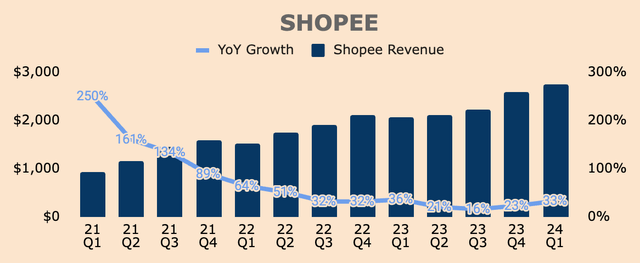

As a result of strong GMV growth, Shopee Revenue grew 33% YoY to $2.7B. Notably, Core Marketplace Revenue was $1.7B, up 47% YoY. Management pointed out that improved service quality and integrated logistical capabilities contributed to Shopee’s growth. For instance:

- Shopee is now directly managing the return-and-refund process, which led to a 30% YoY reduction in resolution times, with about 45% of cases resolved within 24 hours.

- SPX Express is now “one of the fastest and most extensive logistics operators” in Southeast Asia, with about 70% of SPX Express orders in Asia delivered within 3 days. Economies of scale is also evident as SPX Express cost per order dropped by 15% YoY in Asia and 23% YoY in Brazil. Shoppe has been investing heavily to improve and expand its logistics network — and its investments are starting to pay off. These savings could be passed on to the consumers and/or merchants, further strengthening Shopee’s value proposition.

Author’s Analysis

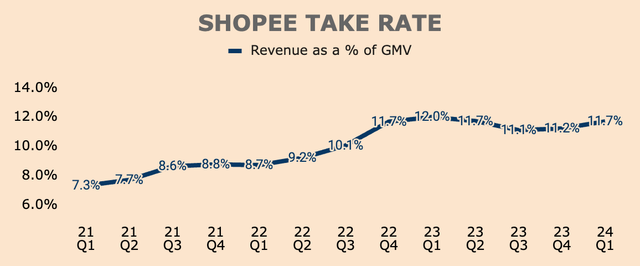

Shopee’s Take Rate — defined as Revenue divided by GMV — was 11.7% in Q1, up from 11.2% a quarter ago. Management spoke about increasing its commission and ad take rate over time, which should drive monetization, and subsequently, Revenue growth.

On the commission take rate, generally, we still see there is a meaningful room to increase the commission take rate, although probably not aggressive — not as aggressive as last year in terms of increase. We also see there’s a meaningful room on the ad take rate that we can look at. I think I shared this in the previous call as well that we believe that our active rate is still slightly lower than the peers that we see in other markets. So there is some meaningful room there.

(CFO Tony Hou — Sea Limited FY2024 Q1 Earnings Call)

Author’s Analysis

That being said, despite higher Take Rates QoQ, Shopee was able to generate record-high GMV and Revenue — this shows how engaged Shopee users are and how dominant the Shopee platform is. And with room to increase Take Rates, Shopee has good potential to deliver robust Revenue growth over the next few years.

For context, assuming $25B of GMV per quarter, a 2 percentage point increase in the company’s ad Take Rate would rake in an additional $500M in high-margin ad Revenue… per quarter!

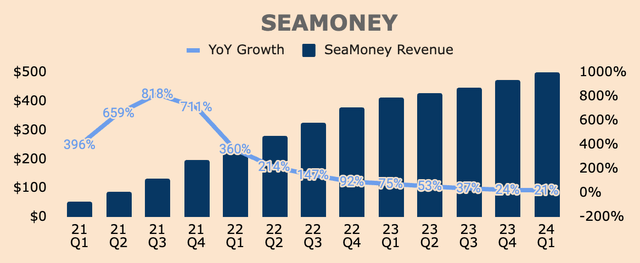

Reason #4: SeaMoney’s Runway

As Shopee grows, it can cross-sell SeaMoney products as well. As of Q1, SeaMoney Revenue was $499M, up 21% YoY. Although growth for the segment is slowing down, SeaMoney continues to make record Revenue with each passing quarter, implying strong demand for SeaMoney products.

Author’s Analysis

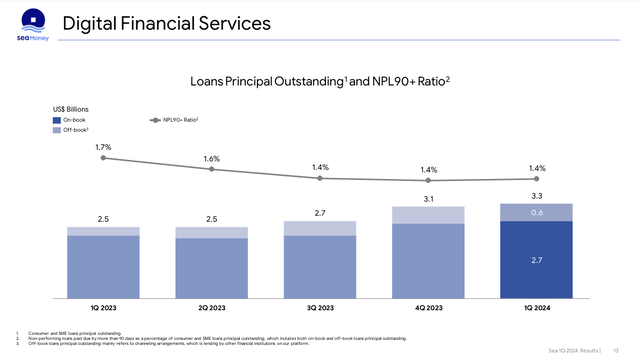

Growth was primarily driven by the consumer and SME credit business with loans principal outstanding of $3.3B, up 29% YoY, and active users of over 18M, up 42% YoY. Non-performing loan (NPL) ratio was 1.4% in Q1, which is stable QoQ.

Sea Limited FY2024 Q1 Investor Presentation

Of important note, 40% of SeaMoney’s loans were off-Shopee loans. This figure was higher than what I was expecting, so I was pleasantly surprised by how strong the off-Shopee business is. Management also mentioned that there’s “further upside to improve off-Shopee penetration”.

More importantly, SeaMoney — whether on or off the Shopee platform — still has a long growth runway ahead as fintech adoption in Southeast Asia remains low (but growing rapidly) which should be a huge boost to SeaMoney over the long run.

e-Conomy SEA Report 2023

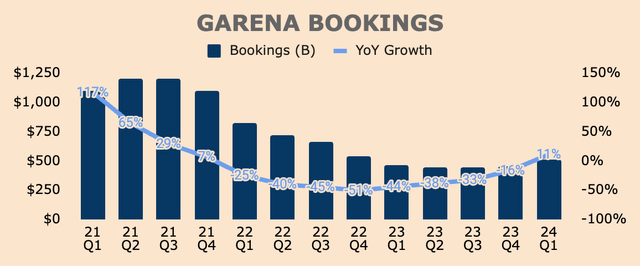

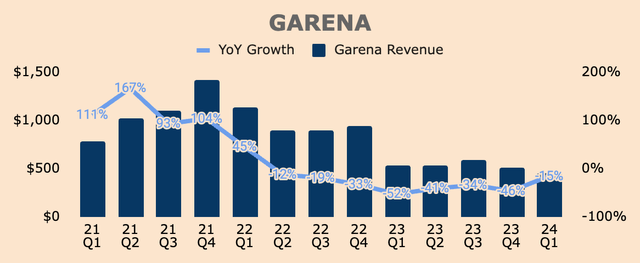

Reason #5: Garena’s Comeback

After two long years of negative growth, Garena finally returned to positive growth with Bookings up 11% YoY to $512M. It is nowhere near 2021 levels but this is a welcome sign that Garena is ready to make a comeback this year.

Author’s Analysis

Despite the growth in Bookings, Garena Revenue was $458M, down 15% YoY. This was mainly driven by “lower recognition of accumulated deferred revenue due to lower bookings in previous quarters”.

As you can see, Revenue continues to trend downwards, which is not good to see, but since Bookings rebounded in Q1, we can expect positive Revenue growth for the segment in Q2 and beyond. In fact, management expects double-digit growth for the segment in 2024.

Author’s Analysis

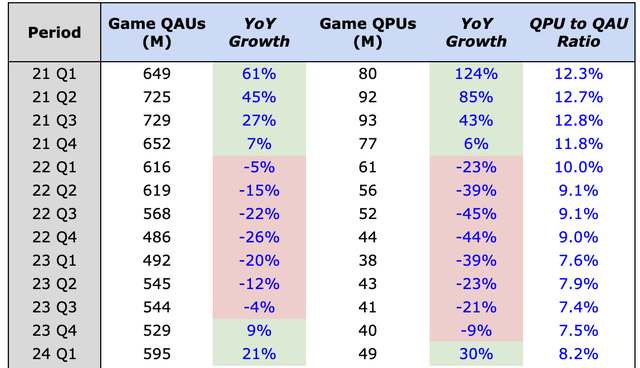

This is further supported by the fact that Quarterly Paying Users grew 30% YoY to 49M, the highest level since Q3 of 2022. Quarterly Active Users was 595M, up 21% YoY. As a result, Paying User Ratio was 8.2%, up 70bps QoQ, signifying improved monetization.

Author’s Analysis

All this growth was driven by Free Fire’s strong performance, which turned out to be the most downloaded mobile game globally in Q1, with average MAUs up 24% YoY in Q1.

And this does not include the relaunch of Free Fire in India, which could juice up Garena’s numbers once it goes live.

For Free Fire relaunch in India, at this moment we are actively working with order–like stakeholders, including like the regulators, the potential local partners, and to figure out what is the best plan to relaunch Free Fire in India. And well, if that is successful, I think that will be a meaningful or potential upside in terms of the users and the bookings considering India is a very, very big market.

(CEO Forrest Li — Sea Limited FY2024 Q1 Earnings Call)

Considering Garena’s strong momentum and potential Free Fire India relaunch, I believe Garena’s turnaround story has only just begun. Eventually, Garena will reclaim its status as a cash cow, producing high-margin Revenue and robust cash flows for years to come.

Reason #6: Profitable Growth

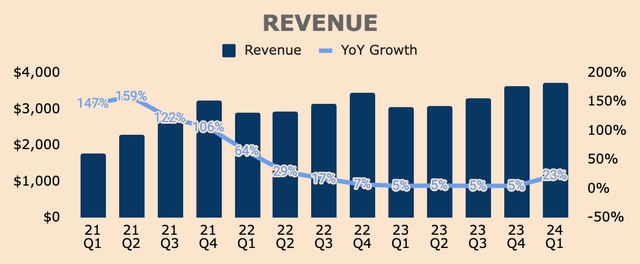

As a whole, Sea generated Revenue of $3.7B in Q1, beating analyst estimates by $110M. This was a breakout quarter for Sea as growth reaccelerated to 23% YoY following five consecutive quarters of single-digit growth.

Author’s Analysis

What’s more impressive is that Sea got all this growth without spending excessive amounts of Operating Expenses. Marketing Expenses did increase 92% YoY to $770M but that’s due to low marketing activity last year as the company was undergoing restructuring. On a QoQ basis, Marketing Expenses actually dropped 20%, so for Sea to produce much higher growth numbers with lower marketing dollars implies strong demand and user engagement.

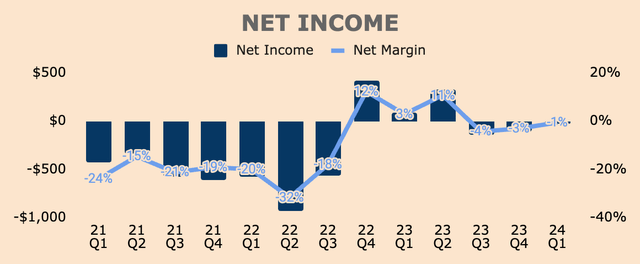

Net Income remained negative at $(23)M, but keep in mind that it is mainly due to investment losses of $111M that were recognized in Q1. Without this impact, Net Income would have been positive.

Author’s Analysis

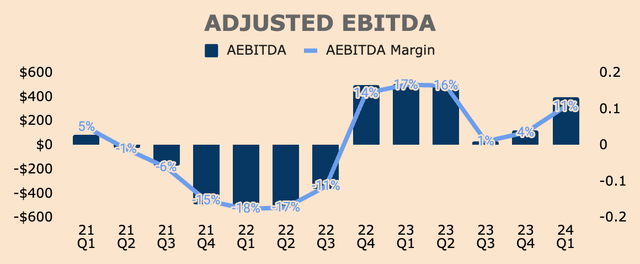

Adjusting for non-cash expenses and one-time charges, Adjusted EBITDA was $401M in Q1, representing an 11% Margin:

- Shopee Adjusted EBITDA was $(22)M, a (1)% Margin. Shopee remains unprofitable as management ramped up Marketing Expenses to stimulate growth and market share expansion. Despite being negative, Shopee Adjusted EBITDA Margin improved by 800bps QoQ so if this trend persists, Shopee should turn profitable in Q2, which could be a major catalyst for the stock.

- SeaMoney Adjusted EBITDA was $149M, a 30% Margin. Management is still investing heavily in the segment to acquire new users and launch new financial services products.

- Garena Adjusted EBITDA was $292M, a 64% Margin, which expanded 21 percentage points YoY and QoQ. With Garena expected to rebound in 2024, we can expect robust cash flows from the gaming division moving forward.

Author’s Analysis

As you can tell, Sea is showing solid growth and an improving margin profile, with all three businesses now firing on all cylinders.

Profitable growth is management’s focus. Earnings are set to compound. Investors will surely be rewarded.

We have a clear roadmap for profitable growth. Our results in the first quarter have given us a strong start to 2024, and we are well on-track to deliver our full-year guidance.

(Sea Limited FY2024 Q1 Earnings Release)

Reason #7: Improving Cash Flow

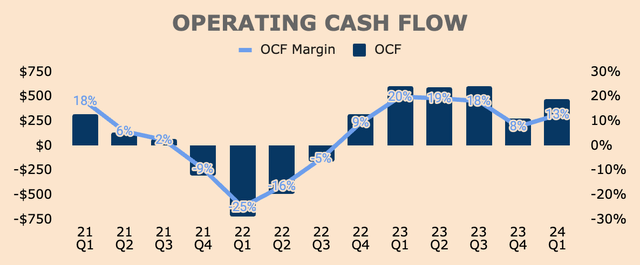

With its focus on profitable growth, Sea is producing strong cash flows. In Q1, Operating Cash Flow was $468M at a 13% Margin. As you can see, Sea has generated positive Operating Cash Flows in the last six quarters, and with business momentum picking up, Sea’s cash flow profile is set to improve further.

Author’s Analysis

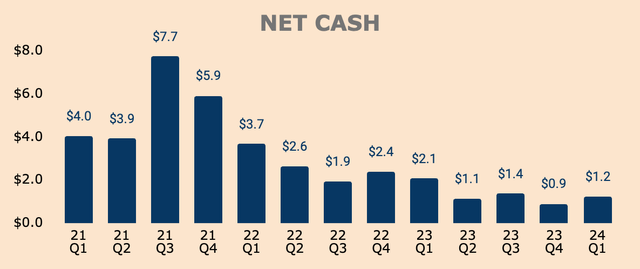

And this should lead to balance sheet expansion over time. As of Q1, Sea has $5.4B of Cash and Short-term Investments with $4.2B of Total Debt, placing its Net Cash position at $1.2B. Net Cash improved by $0.3B QoQ — I expect this figure to rise further in 2024 and beyond.

Author’s Analysis

With positive cash flow and positive net cash, Sea will not only have the financial flexibility to capitalize on opportunities when they arise but also beat smaller competitors who are mostly still unprofitable.

Reason #8: Undervalued Despite Its 100% Run

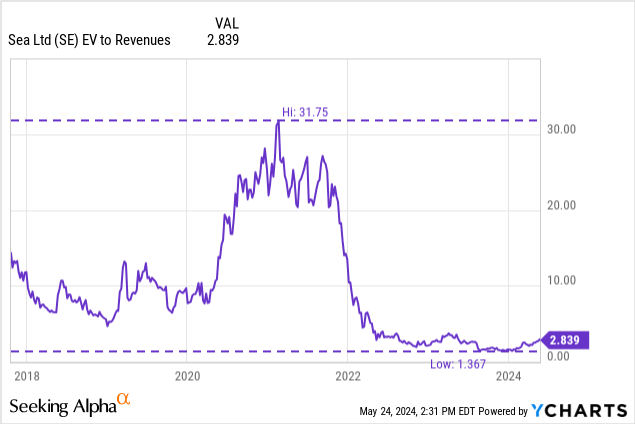

SE stock has had a good run over the last few months, up more than 100% since its bottom of $35 a share. Despite its recent run, Sea still trades at depressed multiples, at just 2.8x its Revenue. As you can see, Sea still sits at its lowest valuation multiple ever — despite being a much larger and more profitable company than ever before.

This disconnect won’t go on forever, and I believe a valuation reset to the upside will happen sooner rather than later.

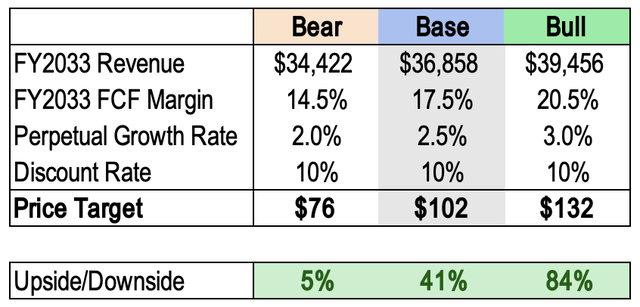

As for me, I have the following price targets for SE stock:

- Bear case: $76

- Base case: $102

- Bull case: $132

Assumptions are laid out below.

In short, I believe SE stock is still undervalued, presenting an upside potential of 41% (base case) over the next twelve months.

Author’s Analysis

Thesis

SE stock had a strong first half of 2024. The parabolic rise in the share price might have tempted some investors to sell out completely.

It’s perfectly reasonable.

But significant alpha can be made when investors buy low and sell high — and do nothing in between.

So to prevent investors from selling out too early, let me recap the 8 reasons to remain bullish on SE stock:

- Dominant market position

- Secular tailwind from Southeast Asia’s digital economy

- Shopee’s market share expansion

- SeaMoney’s fintech opportunity

- Garena’s turnaround story

- Earnings compounder in the making

- Positive net cash and cash flow

- Attractive valuation

There are risks such as competition (nothing new here), slowdown in growth, and worsening losses. However, due to the 8 reasons mentioned above, I believe the potential upside far outweighs the downside.

Read the full article here