RYCEY’s Investment Thesis Remains Compelling – Thanks To Its Successful Reversal

We shall be discussing Rolls-Royce Holdings (OTCPK:RYCEY) (OTCPK:RYCEF) in this article, a unique company, given that it is synonymous to the luxurious vehicles usually reserved for the extreme rich.

However, those in the knows will be aware that this particular company no longer manufactures cars, with that division previously spun off as Rolls-Royce Motors in 1973 and the brand rights broken up amongst BMW Group (OTCPK:BMWYY) for the Rolls Royce range and Volkswagen Group (OTCPK:VWAGY) for the Bentley range.

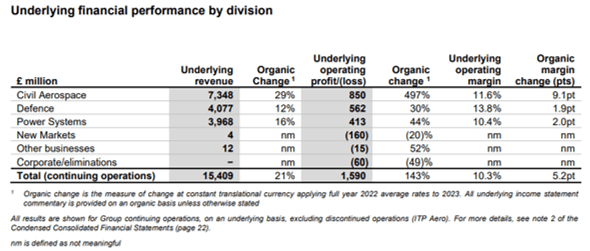

RYCEY Revenue Segment

RYCEY

For now, RYCEY’s primary business is actually in the Civil Aerospace, Defense, and Power Systems, with the Civil Aerospace being its top/ bottom-line driver at £7.34B (+29% YoY) and £850M (+497% YoY) in FY2023, respectively.

Even so, readers must note that things have not always been smooth sailing over the past few years, attributed to the impact of COVID-19 on the aviation industry.

For context, RYCEY had faced uncertain cash flow issues during the pandemic attributed to the “Power by the Hour” business model, where airplane owners would only pay for the hours that the planes’ engines were used, essentially: an “engine subscription plan.”

With most airplanes not flying during the heights of the pandemic, it was unsurprising that RYCEY had faced impacted top/ bottom lines in FY2020/ FY2021, with the management having to take on additional debts then.

And this was also when RYCEY had to raise capital by offering shareholders the “rights issue plan” in October 2022, in which “investors can buy 10 new shares for every three they own at 32 pence each, a 41% discount to the theoretical ex-rights price,” effectively raising £2B in cash then.

While this strategy had naturally taken “any liquidity questions off the table through the crisis,” we had also seen its shares outstanding grow tremendously from 1.9B in FY2019 to 5.98B in FY2020, 8.35B in FY2021, and finally, to 8.4B in FY2023.

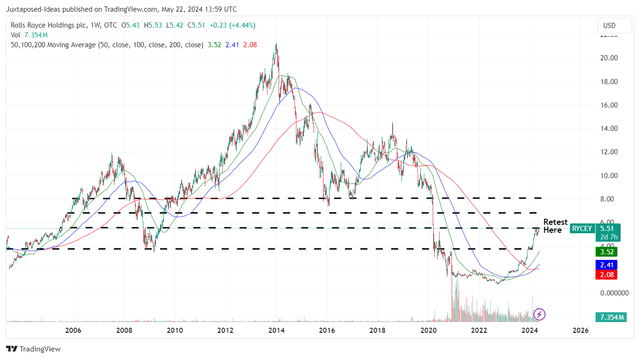

RYCEY 18Y Stock Price

Trading View

As a result of the impacted top/ bottom lines and the immensely dilutive capital raises during the pandemic period, it is unsurprising that RYCEY’s stock prices have also collapsed between 2020 and 2022, with things only recovering by late 2022 after a management shake up and air travel returns.

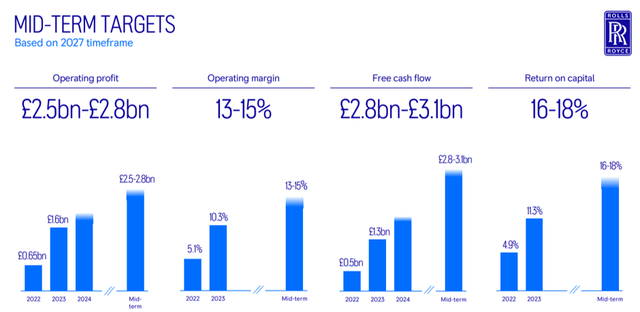

RYCEY 2027 Target

RYCEY

The new CEO had taken drastic steps then, by laying off numerous headcounts, optimizing operational costs, and hiking servicing prices, all of which was part of its transformation plan to deliver the ambitious 2027 targets as outlined above.

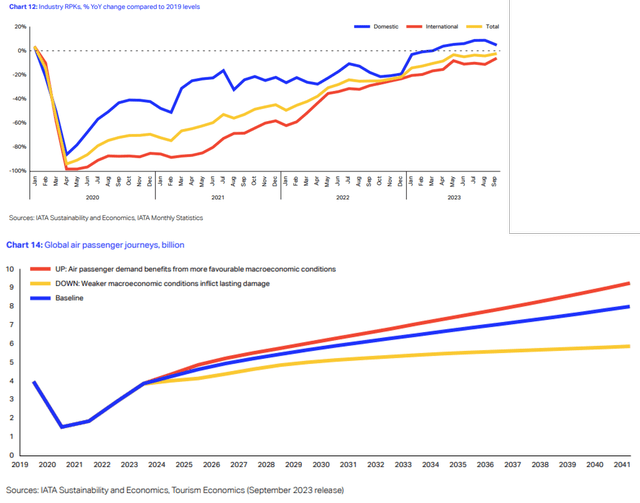

Global Air Travel Trends & Projections

IATA

At the same time, global air travel has recovered near to pre-pandemic averages by the end of 2023, with things to further grow over the next few years as the “global commercial aviation fleet also expands by +33% to more than 36,000 aircraft by 2033, according to an Oliver Wyman analysis.”

As a result of these developments, it is unsurprising that the RYCEY stock has recovered drastically by +607.8% from the October 2022 bottom, well outperforming the wider market.

This is also buoyed by the company’s excellent FY2023 results, with revenues of £15.4B (+21% YoY), growing operating margin of 10.3% (+5.2 points YoY/ +5.1 from FY2019 margins of 5.2%) and robust Free Cash Flow generation of £1.28B (+154.4% YoY), further aided by the growing civil Long-Term Service Agreement balance growth to £9.08B (+23.2% YoY/ +59.5% from FY2019 levels of £5.69B).

Based on RYCEY’s growing cash/ equivalents of £3.78B (+45.3% YoY) and the moderating debts of £4.04B (-1.4% YoY) in FY2023, its balance sheet looks much healthier at net debts of -£0.26B as well (+82.6% YoY/ -123.4% compared to FY2019 net cash of £1.11B).

This is especially since only £0.5B of its debts is maturing in 2024, £0.8B in 2025, and £2.8B through 2028.

At the same time, readers must note that the RYCEY management has delivered a promising FY2024 guidance, with £1.85B in operating profits (+16.3% YoY) and £1.8B in Free Cash Flow generation (+40.6% YoY), further underscoring its successful turnaround story.

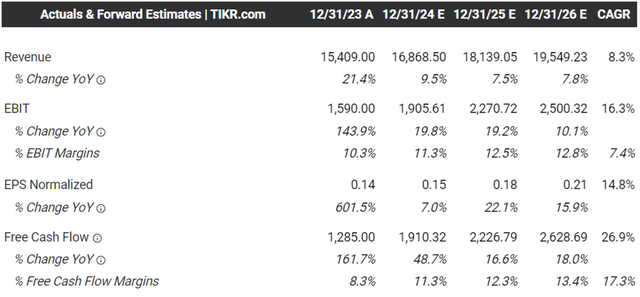

The Consensus Forward Estimates (in £)

Tikr Terminal

Perhaps this is also why the consensus have raised their forward estimates, with RYCEY expected to generate a promising top/ bottom line performance at a CAGR of +8.3%/ +14.8% through FY2026.

This is compared to the previous estimates of +5.6%/ -5.9% and the historical growth at +3.9%/ -19.3% between FY2016 and FY2019, respectively, with FY2024 likely to cement the CEO’s position as a visionary leader that has brought the company “from a burning platform to a booming platform” within two short years.

At the same time, based on adjusted split prices, the RYCEY stock has already exceeded the Q2’20 pandemic prices (prior to the dilutive capital raise), further underscoring the excellent bullish support and its ongoing reversal, thanks to the new CEO’s transformation plans.

So, Is RYCEY Stock A Buy, Sell, or Hold?

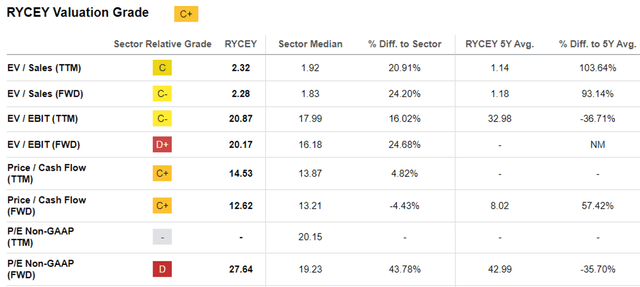

RYCEY Valuations

Seeking Alpha

For now, RYCEY is trading at FWD P/E valuations of 27.64x, higher than the 1Y mean of 25.67x though finally nearing its 3Y pre-pandemic mean of 31.56x.

Compared to its aerospace engine peers, such as RTX Corporation (RTX) at 19.55x and GE Aerospace (GE) at 39.80x, it appears that RYCEY is still trading reasonably, offering interested investors with a decent margin of safety.

For now, based on the FY2023 adj EPS of $0.18 (based on the exchange rates at the time of writing) and the FWD P/E valuations of 27.64x, it seems that RYCEY is trading near to our fair value estimates of $5.00.

Based on the consensus FY2026 adj EPS estimates of $0.27, there seems to be an excellent upside potential of +39.4% to our long-term price target of $7.50 as well.

At the same time, based on RYCEY’s improving balance sheet and expanding profitability as discussed above, there is a good chance that the management may reinstate dividends and/ or buy back shares in the intermediate term, once it returned “to an investment grade credit rating,” presumably by sometime in 2025 as projected by Fitch Ratings.

As a result of the attractive risk/ reward ratio, we are initiating a Buy rating for the RYCEY stock, though with no specific entry point since it depends on individual investors’ dollar cost average and risk appetite.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here