A while ago, I wrote a cautious article on the SRH Total Return Fund (NYSE:STEW). Although I liked STEW’s value-oriented investment process, the fund had significantly underperformed the S&P 500 Index for many years and the underperformance was likely to continue.

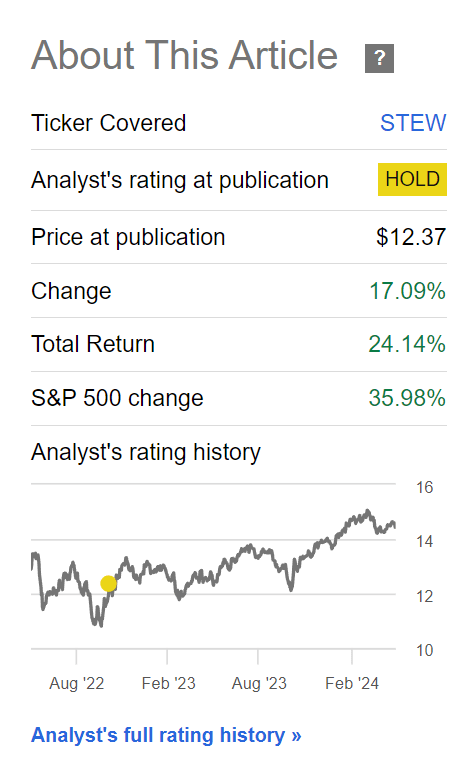

So far, my caution has been warranted, as the STEW fund has returned 24% in total returns since my article, significantly below that of the S&P 500 Index’s 36% nominal returns (Figure 1).

Figure 1 – STEW has returned 24% since October 2022 compared to 36% for S&P 500 Index (Seeking Alpha)

Has STEW’s performance actually been that poor (12% underperformance) compared to the index, or was there another factor at play?

Upon closer analysis, STEW’s underperformance in recent quarters has been primarily driven by a widening discount to NAV. The discount is now at a historically wide 22%.

With markets showing signs of froth, I believe investors should consider transitioning to a more defensive positioning, and STEW’s 22% discount to NAV gives investors a wide margin of safety. I am upgrading STEW to a relative buy.

Brief Fund Overview

The SRH Total Return Fund, Inc. is a closed-end fund (“CEF”) focused on total returns by applying a “value investing” approach to identify attractive companies for its portfolio.

The STEW fund was formerly managed by billionaire investor, Stewart Horejsi, until his retirement in April 2022. Since then, it has been managed by portfolio managers Joel Looney and Jacob Hemmer, who have been working at the STEW fund since 2013 and 2018 respectively (Figure 2).

Figure 2 – STEW is currently managed by Mr. Looney and Hemmer (srhfunds.com)

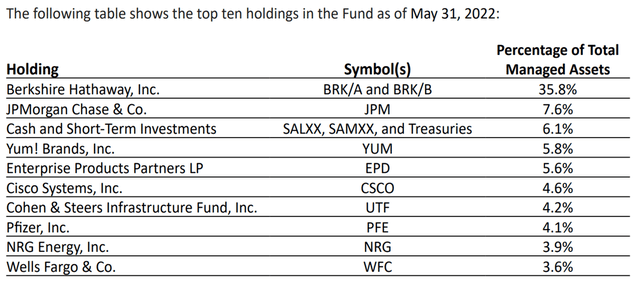

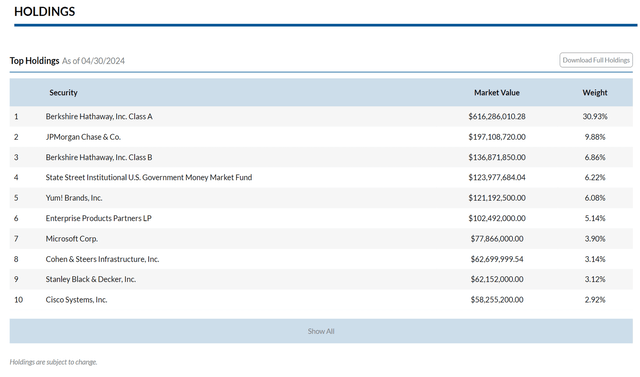

The STEW fund is characterized by long-term core holdings and low turnover. In fact, comparing the portfolio holdings as of May 31, 2022 (Figure 3, the most recent semi-annual report before my last article) to April 30, 2024 (Figure 4, most recent month-end), most of the fund’s top-10 holdings have remained the same.

Figure 3 – STEW top 10 holdings, May 31, 2022 (STEW 2022 semi-annual report)

Figure 4 – STEW top 10 holdings, April 30, 2024 (srhfunds.com)

The only notable changes have been the addition of Microsoft (MSFT) and Stanley Black & Decker (SWK) into the top 10 in place of Pfizer (PFE) and NRG Energy (NRG).

STEW’s portfolio disclosures appear to have improved with the change in management, as the fund now discloses month-end top 10 positions whereas historically, I believe position information was only available in financial reports.

Underperformance Mostly Driven By Widening Discount

As I noted at the beginning of this article, STEW’s market performance since October 2022 has significantly underperformed that of the S&P 500 Index. However, looking in more detail, STEW’s investment performance was not as poor as the market returns difference suggests.

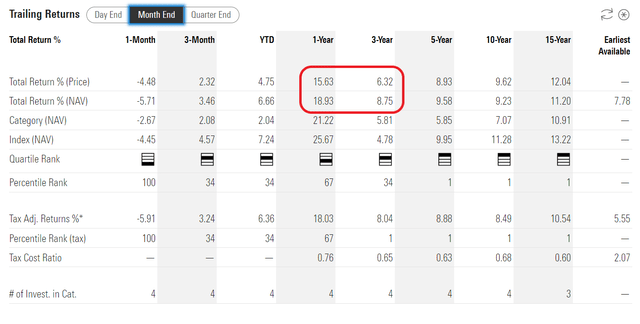

For example, the STEW fund has a 1-year net asset value (“NAV”) return of 18.9% to April 30, 2024, and a 3-year average annual return of 8.8% (Figure 5).

Figure 5 – STEW historical returns (morningstar.com)

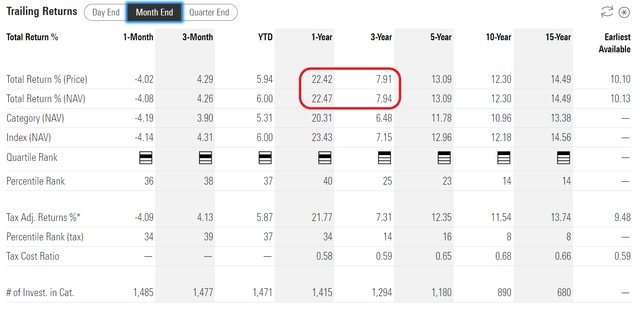

While the 1-year return has lagged the SPDR S&P 500 ETF Trust’s (SPY) 22.5% return, STEW outperformed SPY’s 7.9% return on a 3-year basis (Figure 6).

Figure 6 – SPY historical returns (morningstar.com)

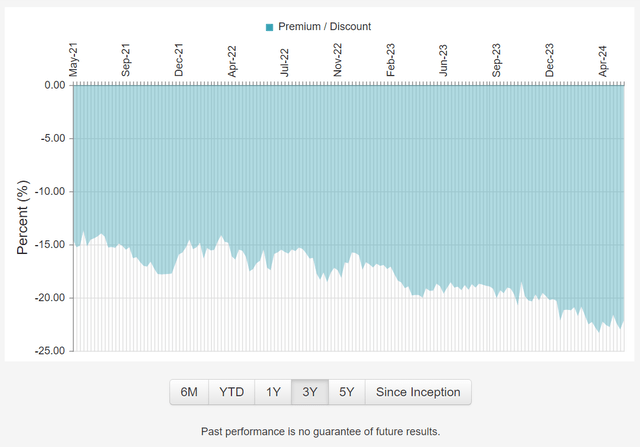

STEW’s market underperformance is primarily driven by a widening of its discount to NAV, which has widened from ~15% when I last wrote about the fund to 22% currently (Figure 7).

Figure 7 – STEW’s discount to NAV has widened to 22% (cefconnect.com)

CEFs Can Trade A Significant Discount/Premiums To Net Asset Value

A closed-end fund is a type of investment fund with a fixed number of shares that are issued to investors through an initial public offering (“IPO”), much like a regular company’s stock.

After the IPO, CEFs shares can be bought and sold on a stock exchange like regular stocks, but no new shares will be created, and no new money will be raised by the fund, unless the fund explicitly engages with dealers to issue new shares (i.e. via a rights offering).

Therefore, if the demand for a CEF’s shares is very high or low, the shares may even trade at a significant premium or discount to the fund’s net asset value.

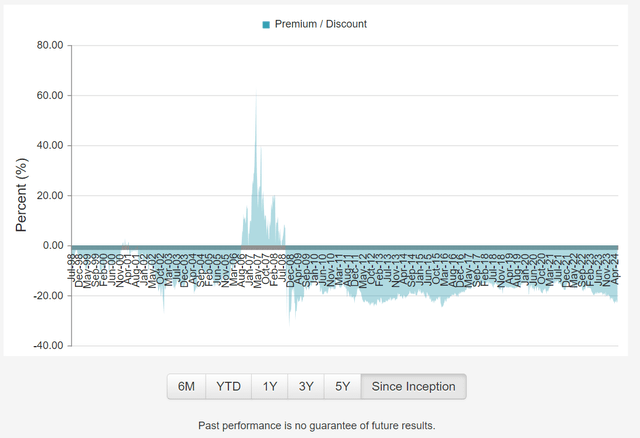

In STEW’s case, investors have gotten very pessimistic about the fund’s near-term prospects and have punished the STEW fund to a 22% discount to NAV, one of the widest discounts since STEW’s inception (Figure 8).

Figure 8 – STEW’s discount to NAV at historically wide levels (cefconnect.com)

While there is no guarantee that a fund’s discount to NAV will close, there are usually strategies an investment fund can adapt to reduce this discount. For example, the fund can institute a share buyback at a discount to NAV (say 95%), such that any shares bought back will be accretive to remaining unitholders while offering selling unitholders an ability to improve their discount to NAV.

STEW As A Defensive Play

Interestingly, if we study Figure 8 above in detail, during financial crises like the 2001 dot-com bubble bursting and the 2008 Great Financial Crisis, the STEW fund’s discount to NAV actually closed and/or went positive. This is probably because the STEW fund’s value-oriented investment process, translates into a portfolio dominated by defensive stocks like Berkshire Hathaway (BRK.A) that perform well during financial crises.

So in some respects, investors may consider the STEW fund as a defensive way to gain equity exposure, as the fund’s wide discount to NAV gives investors a margin of safety, in addition to the defensive stock picks.

Tax Risks May Be Overblown

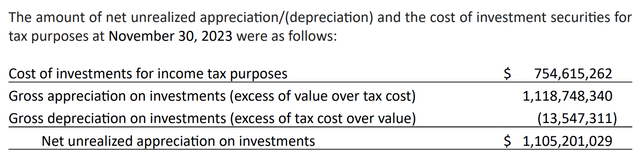

In my prior article, I saw many commentators note that the STEW fund has a lot of embedded tax liabilities, since the fund’s cost base for its investments was very low (Figure 9).

Figure 9 – STEW has a low tax base for its investments (STEW 2023 annual report)

Commentators worried that if the STEW fund were to liquidate its portfolio, recent investors would be hit with a large tax bill without the corresponding unrealized investment gains to offset.

While that is technically true, I believe this fear may be overblown. As of November 30, 2023, trusts and entities affiliated with Mr. Horejsi owned 45,384,254 shares of Common Stock of the Fund, or 46.75%. In my opinion, it is highly unlikely that the STEW fund will saddle Mr. Horejsi and his affiliates with a large tax bill, given his influence on the fund manager.

Conclusion

As markets continue to make new all-time highs based on the narrow leadership of AI-related stocks like Nvidia (NVDA) and Microsoft, I am uncomfortably reminded of the 2001 dot-com malinvestment bubble. Therefore, my attention in recent months has been to look for defensive ways to maintain equity exposure.

I believe the STEW fund could be an appealing candidate. The STEW fund employs a value-oriented investment process to pick stocks that are held for the long term. Its portfolio consists of market stalwarts like Berkshire Hathaway and JPMorgan. It currently trades at a 22% discount to NAV, giving investors a wide margin of safety. I am upgrading STEW to a relative buy.

Read the full article here