Investment summary

My recommendation for Petco Health and Wellness (NASDAQ:WOOF) is a sell rating. I am not convinced that the business is on track for a recovery anytime, as various metrics such as growth, market share, balance sheet, and FCF have all worsened or shown no signs of improvement. Despite this, the market seems to be already pricing in earnings recovery for the business.

Business Overview

WOOF is a retailer specializing in pet products, including food, tools, and toys, as well as grooming, training, veterinary, and prescription services. The business operates veterinary clinics within its brick-and-mortar locations as well as stand-alone and mobile units, and retails several owned brands across the food, wellness, and accessory space. Segment wise, WOOF has 4 segments: Consumables which is 50% of total revenue; Supplies and Companion Animals [SCA] that are ~34% of total revenue; Services and Other that are ~16% of total revenue; and e-commerce, which is 17% of total revenue. Geography-wise, WOOF only serves the US market.

1Q24 results update

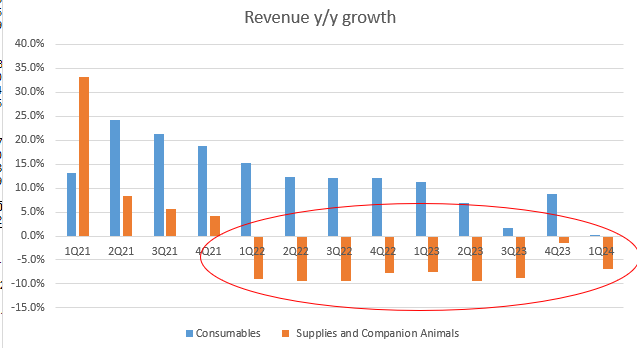

Released on 22nd May 2024 (last week), WOOF revenue fell by 1.7% to $1.529 billion, mostly driven by a same-store sales decline of 1.2%. By segment, consumables was flat at 0.1% y/y growth, SCA fell by 6.8%, and services and others grew by 4.2%. Gross margin came in better than expected at 37.8%, a 101 bps expansion vs. last year. Hence, while revenue fell, the improvement in gross margin drove the adj. EBIT margin to 1.2%, 60bps above consensus. In terms of free cash flow [FCF], WOOF reported -$41.1 million FCF, which was a big decline from 1Q24’s -$24.4 million.

No signs of bottoming

Redfox Capital Ideas

WOOF’s 1Q24 performance showed little, if not no, signs of bottoming or recovery at all. Its two largest segments (Consumables and SCA) continue to show lackluster performance. In particular, the SCA segment revenue decline worsened in 1Q24, dashing the hopes that 4Q23 represented a positive trend. The same was true for WOOF’s largest segment (Consumables) which saw muted growth. Though a part of this weakness can be attributed to lapping the high prices last year, the fact is that discretionary spending continues to be weak (this was called out by management in the earnings call). With inflation remaining sticky and interest rates staying high, I do not see any strong catalysts that would drive a recovery in discretionary spending anytime soon.

Turnaround showed improvements, but visibility was still limited

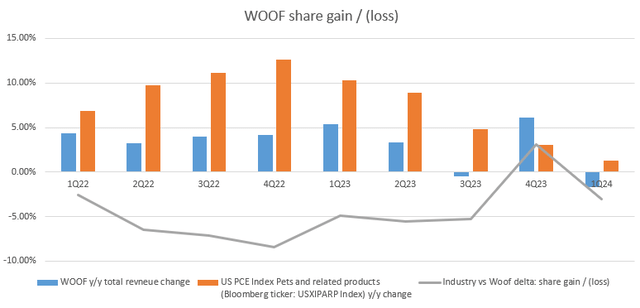

I do give credit to the interim CEO, Mike Mohan, and the broader executive team for attempting to turn around the business. However, the fact of the matter today is that WOOF continues to lose share after a blip in 4Q23, dashing hopes that an improvement is underway. I believe this is largely due to the fact that WOOF is missing a permanent CEO who can steer the business in the right direction. The lack of a proper management team to lay out a clear strategic focus is costing WOOF a lot of market share, and I expect this to continue if WOOF continues to operate in its current state.

Redfox Capital Ideas

The bullish investors might point to the improvement in gross margin and say that the team is moving in the right direction. That is not wrong; however, I note that visibility regarding WOOF’s near-term margin profile remains limited, particularly given the various initiatives underway to improve operations. For instance, the current management team plans to optimize store layouts, review pricing and assortment strategies, revamp inventory management practices, etc., and all of these take time and a lot of resources (capital and time) to make it work. In other words, margins and growth might get a lot more volatile in the meantime before we see a positive recovery, and I am not a fan of taking this risk while the valuation is already pricing in a recovery (as I note in the valuation section below).

Risky balance sheet

The biggest risk I see to WOOF is that its leverage ratio, on a net debt to last twelve months adj EBITDA basis, has increased to 4.1x from 3.7x in 4Q23 and 2.9x in 1Q23. Notably, the driver of this change is because WOOF EBITDA fell, not because net debt increased. This is concerning because my outlook for WOOF’s earnings is pretty negative at this point, considering the lackluster performance, continuous market share loss, and near-term operation disruptions. If earnings continue to stay poor, my worry is that the WOOF leverage ratio may continue to increase, and that would risk triggering any debt instrument covenant ratio. From a valuation perspective, it would also see pressure as the cost of equity would increase.

It also does not help to know that WOOF FCF worsened in 1Q24, driven by significantly lower operating cash flow despite a meaningful reduction in capex spend (down 47% vs. 1Q23). To put things into perspective, 1Q24 represented the company’s first negative operating cash flow quarter since the pandemic-impacted 1Q20, and that FCF for the quarter was also the lowest reported quarterly figure since 1Q20. While management is focused on turning FCF positive, I am not willing to give the benefit of doubt at this point, as I do not see any positive signs of it happening yet.

Valuation

The market is currently pricing WOOF at 38x 2-year forward earnings (average is around 18x 2-year forward), which means the market is already anticipating the current management team to turn things around, and I believe this is too optimistic at this point. The only positive sign so far is that gross margin has improved, but everything else, from growth to market share to balance sheet to FCF, has been negative. Simply from a valuation standpoint, if WOOF shows little progress in earnings recovery, the market could push valuation back down to 18x, and that itself represents ~50% downside.

Risk

The upside risk is that the management does turn things around, and this will fuel a very positive sentiment for the stock as WOOF is finally out of the woods. Installing a permanent CEO with a good pedigree would work well from a sentimental perspective too.

Conclusion

My view for WOOF is a sell rating. Despite some improvement in gross margin, WOOF exhibits no signs of recovery across its core metrics including growth, market share, and balance sheet. The current valuation appears overly optimistic, pricing in a turnaround that seems unlikely. The lack of a permanent CEO and weak discretionary spending environment further diminish the outlook for WOOF.

Read the full article here