What Happened

US stocks outpaced international markets in the first quarter, due in no small part to ongoing interest in the prospects for artificial intelligence (‘AI’), which propelled the shares of many large-cap American companies in the technology sector. International small caps lagged their large-cap counterparts by 260 basis points (‘bps’), although benchmark returns were mixed by region and sector.

Monetary policies in global developed markets, which had previously moved together toward higher rates to curb inflation, began to diverge as central bankers addressed varied inflationary trends. In the US, the Federal Reserve kept its benchmark rate steady at 5.25–5.50% for a fifth consecutive meeting, as higher-than-expected Consumer Price Index figures largely caused by rising housing expenses dashed hopes for an early rate cut. Nevertheless, the Fed continued to signal three rate cuts this year. Both the Bank of England and European Central Bank also kept rates unchanged, in contrast to the Swiss National Bank’s unexpected reduction of 25 bps—the first cut by a major central bank since the pandemic’s end—triggered by inflation there returning to the bank’s target range.

MSCI ACWI ex US Small Cap Index Performance (USD %)

|

Sector |

1Q 2024 |

Trailing 12 Months |

|

Communication Services |

-0.5 |

5.7 |

|

Consumer Discretionary |

2.1 |

9.7 |

|

Consumer Staples |

-0.4 |

6.5 |

|

Energy |

6.3 |

19.8 |

|

Financials |

6.8 |

28.4 |

|

Health Care |

-1.6 |

7.1 |

|

Industrials |

5.5 |

17.0 |

|

Information Technology |

2.1 |

20.3 |

|

Materials |

-0.6 |

5.3 |

|

Real Estate |

-2.5 |

5.6 |

|

Utilities |

0.4 |

10.0 |

|

Source: FactSet, MSCI Inc. Data as of March 31, 2024. |

|

Geography |

1Q 2024 |

Trailing 12 Months |

|

|

Canada |

4.5 |

7.0 |

|

|

Emerging Markets |

1.1 |

21.1 |

|

|

Europe EMU |

1.4 |

9.4 |

|

|

Europe ex EMU |

1.1 |

10.6 |

|

|

Japan |

5.2 |

14.8 |

|

|

Middle East |

5.1 |

14.1 |

|

|

Pacific ex Japan |

0.1 |

4.8 |

|

|

MSCI ACWI ex US Small Cap Index |

2.2 |

13.4 |

|

|

Source: FactSet, MSCI Inc. Data as of March 31, 2024. |

|||

In a landmark move, the Bank of Japan (‘BOJ’) raised short-term interest rates, bringing to a close the country’s decade-long era of negative interest rates. The BOJ also announced an end to both its yield curve control policy, which had capped long-term Japanese government bond yields, and its asset-purchase program, which had encompassed not only government bonds but also stock ETFs and real estate investment trusts, in a sustained effort to offset negative wealth effects from deflation. As a result, yields on Japanese 10-year bonds increased, though they remain well below comparable yields in other developed markets.

These moves boosted value stocks in Japan, which led the index. While all regions ended in positive territory, Pacific ex Japan was the biggest laggard, weighed down by Hong Kong, New Zealand, and Singapore.

Financials, Energy, and Industrials, some of the most economically sensitive sectors, outperformed amid higher interest rates, higher energy prices, and improving economic sentiment in many economies. Even though large-cap tech companies are more easily thought of as direct beneficiaries of the rising demand for semiconductors and AI tools, AI-related spending also boosted the small-cap Information Technology (‘IT’) sector’s returns (later, we highlight a holding that is capturing some of this spending).

The Materials sector underperformed as prices fell for several commodities—including iron ore, nickel, and lithium—amid weak economic growth in China and declining demand for electric vehicles, which source raw materials for their batteries. Health Care was another weak sector, as higher interest rates and reduced venture-capital investment in drug-discovery startups continued to weigh on investor sentiment. US legislators also introduced a bill called the Biosecure Act to limit Chinese companies from accessing US patient data, which may restrict the ability of US companies to work with Chinese partners on national-security grounds.

By style, the cheapest stocks outperformed the most expensive by about 370 bps. The trend was especially pronounced in Japan, where the cheapest stocks outperformed the most expensive by nearly 1,600 bps. The MSCI All Country World ex US Small Cap Value Index also beat its growth counterpart by nearly 70 bps.

How We Did

The International Small Companies Equity composite declined 0.09% gross of fees in the first quarter, compared with a 2.21% gain in the MSCI ACWI ex US Small Cap Index. Weak relative returns were largely due to poor stock selection.

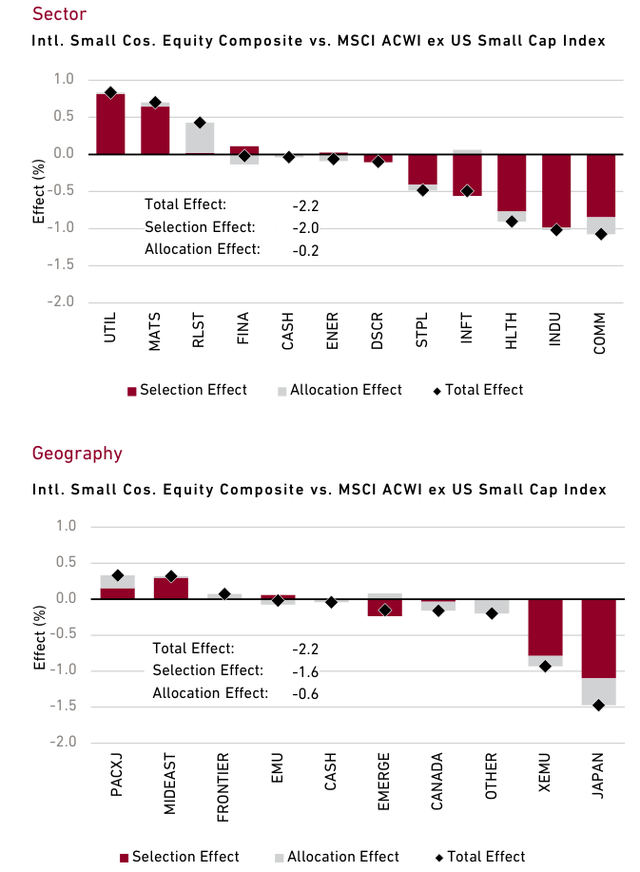

Japan accounted for nearly two-thirds of our underperformance, as investors in the region continued to favor the cheapest stocks, which are typically associated with the least-profitable and slowest-growing companies. Among the worst performers was Solasto (OTCPK:SLSCF), a leading provider of medical administration outsourcing services. The company reported profit that fell short of its own projections due to higher labor costs, IT investments, and new contracts with large hospitals.

First Quarter 2024 Performance Attribution Sector

|

“FRONTIER”: Includes countries with less-developed markets outside the index. “OTHER”: Includes companies classified in countries outside the index. Source: Harding Loevner International Small Cos. composite, FactSet, MSCI Inc. Data as of date March 31, 2024. The total effect shown here may differ from the variance of the composite performance and benchmark performance shown on the first page of this report due to the way in which FactSet calculates performance attribution. This information is supplemental to the composite GIPS Presentation. |

Performance was also poor in Europe ex EMU. Among our weakest performers was UK-based Keywords Studios (OTCPK:KYYWF), which does outsourced work for the video-game industry. While the company reported 13% revenue growth in 2023, investors continue to worry that as game developers increasingly use AI tools, they will have less of a need for Keywords’ services.

Returns in Pacific ex Japan helped offset some of the weakness. Shares of Singapore-based ASM Pacific Technology, a supplier of advanced packing equipment used to build semiconductors, surged on expectations that demand for AI chips will fuel the company’s growth.

By sector, the biggest laggards were Communication Services and Industrials. In Communication Services, YouGov (OTCPK:YUGVF), a UK-based market research company, reported weak organic sales growth due to a combination of more muted spending by customers, longer sales cycles, pricing pressure, and weakness in certain end-markets such as gaming. In Industrials, Japan-based SMS (OTCPK:SMSZF), which helps elderly-care centers recruit nurses, said that increased hiring led to strong sales growth but lower margins.

Health Care was also weak, including shares of Evotec (OTCPK:EVOTF), a contract research company focused on discovering new drugs for pharmaceutical and biotechnology clients. At the start of the year, Evotec’s chief executive officer resigned after failing to properly report his stock trades. Our takeaway from having continual discussions with Evotec’s board is that the broader executive management team has long been responsible for carrying out the company’s strategy, which should limit execution risks following the CEO’s departure.

The Materials sector performed well. SH Kelkar, a leading supplier of fragrances and flavors in India, reported 29% revenue growth in its latest quarter. It also won a contract with a large multinational consumer-staples company, a sign of its strengthening market position.

What’s On Our Minds

Charlie Munger once used a surfing metaphor to explain how a company can take advantage of a “wave”—a powerful trend or industry force—to create long-term growth. By recognizing a large wave as it forms and catching it at the right moment, he said, a surfer can ride the wave for “a long, long time.” It was 1994, and one of the examples Munger gave was Microsoft (MSFT) and the rise of personal computing, a wave the company would ride for the next three decades to a US$3T market capitalization. Munger, who died last year, was also known to preach patience: “The first rule of compounding,” as his famous line goes, is to “never interrupt it unnecessarily.” Finding companies poised to benefit from big waves, and allowing time for their profits to grow and compound, can have a powerful effect on returns.

Generative AI is a wave that has gained tremendous momentum since the November 2022 launch of ChatGPT, a chatbot that introduced much of the business world to the practical applications of AI. While computer scientists have been working to improve AI for decades, the revolutionary change initiated by the success of large-language models like the one ChatGPT uses is in its infancy. The world spent around US$50B on the chips that enable this technology in 2023. This figure is widely expected to surge over the next few years, although forecasts vary from about US$100B to more than US$400B. Large companies such as Nvidia (NVDA) have been the earliest and clearest beneficiaries of this demand. However, there are many smaller companies, such as our holding Pfeiffer Vacuum (OTCPK:PFFVF), that occupy an important niche in the supply chain.

Pfeiffer Vacuum is a German manufacturer of advanced pumps that create near-perfect vacuums, a critical tool for maintaining the “clean rooms” where semiconductors are manufactured. Clean rooms are sterile environments that must be devoid of dust and other airborne particles. When making semiconductors, the smallest contamination can adversely affect their precision and functionality, which reduces a manufacturer’s yield of non-defective chips. As semiconductors become more sophisticated, they also require more material deposition—a process in which thin layers of material are deposited onto the wafer—as well as more processing. The smaller the transistor, the more sensitive it is to impurities in the air. With this increasing complexity, not only are more vacuum pumps needed, but also more powerful pumps.

An attractive feature of this niche is its consolidated industry structure: Two suppliers, Pfeiffer Vacuum and Atlas Copco (OTCPK:ATLKY), control about 95% of the global market for clean room vacuum pumps. And nearly half of Pfeiffer Vacuum’s overall sales are to semiconductor customers. The company’s competitive advantage is underpinned by a strong brand and high switching costs—characteristics that we think are likely to endure. Pfeiffer Vacuum has recently experienced a slowdown in orders, but we expect capital spending by chipmakers to ebb and flow over the short run, and for long-term demand to remain strong.

Another wave that appears ready to crest is in cybersecurity. With data breaches on the rise—ransomware attacks were up 70% in 2023—our Israeli holding Cyberark (CYBR) has built a strong position in the fast-growing niche of protecting “privileged accounts.” This term refers to the users or applications that have access to sensitive areas of a business’s computer systems. If a firewall is breached, Cyberark’s tools create a digital vault inside the enterprise that securely stores these credentials, alerts the customer’s IT professionals, and monitors and records the movement of the hacker inside the network.

Several years ago, Cyberark decided to shift from selling its technology as a one-time purchase to a cloud-based subscription model. Cloud-based solutions allow for more seamless updates, thus better protecting customers from ever-evolving risks. But because upfront revenue from new customers is lower in a subscription model, this strategic shift reduced margins and cash flows for a time, leading some investors to doubt the company’s growth outlook. But like other companies that have transitioned to a subscription model, such as Microsoft, revenue has now rebounded. Revenue is expected to grow 24% this year, with subscription fees accounting for an increasing majority. Adjusted cash flows are also climbing back above their 2021 level.

A key feature of the cybersecurity wave is the growing array of non-human digital identities that must be protected from hackers. Typically, we think of login credentials and permissions as being tied to humans such as IT administrators. But for every human identity there are now 45 machine identities—such as software applications, servers, and other devices connected to a business’s network. This has expanded Cyberark’s addressable market. In a recent meeting, management estimated that only about 50% of the privileged users—human and machine—in its customers’ organizations are secure, presenting a large opportunity to expand Cyberark’s relationships with these companies. Furthermore, in December, the US Securities and Exchange Commission said all US-listed companies will be required to report “material” cybersecurity events within four days, which helps incentivize businesses to prioritize cybersecurity investments. Providers of cybersecurity insurance are also requiring customers to have privileged-access-management capabilities. Another promising development is Cyberark’s new Secure Cloud Access offering, a small but growing source of revenue. Security has not kept pace with the rapid adoption of cloud-based services and the growing number of developers who use these services. Secure Cloud Access aims to address this problem by providing a way to limit users’ permissions based on what they need access to and when.

Long-term waves can be turbulent, and as Munger said, some companies fall off. An investor always must be watching for signs that a business is losing its competitive edge. For now, though, Pfeiffer Vacuum and Cyberark appear well positioned to surf the wave.

Read the full article here