Preamble

Of late, I’ve written a couple of sell-while-you-can articles. For those who follow Deere & Company (DE), you may recall the article I penned forecasting an imminent drop in the stock price. Although, I have covered NVIDIA (NASDAQ:NVDA) (NEOE:NVDA:CA) investment in AI minnows, which evokes positive optimism in Nvidia’s future dominance in AI, this article is more of a harbinger of tough times ahead in markets outside of the collective West and the Chinese market.

Those who keep abreast of chip related stories will be familiar with the US government’s sanctioning of China with the enthusiasm of a Wall Street banker selling Mortgage-Backed Securities to the Greeks. For instance, in October last year, it was reported that the US government tightened export restrictions on Nvidia’s most advanced AI chips. These chips, which were designed for the Chinese market under previous regulations, then were banned for export. This move escalated the tech war and China condemned the restrictions. The US implemented similar restrictions the previous year in order to prevent China from acquiring powerful AI technology.

Fast-forward 1 year, and it’s evident that the restrictions haven’t worked. Apparently, despite the US ban on selling advanced AI chips to China, various institutions have managed to acquire them through resellers, who remain unknown. Experts who have delved into the matter claim that the chips may well have been diverted without the manufacturer’s knowledge. The US is now investigating potential violations, and Nvidia says they’ll take action if necessary. Server makers claim they complied with regulations and the products sold were not the most advanced.

As you may imagine, not only did the restrictions have a limited effect, but they spurred China to develop alternatives to Nvidia from home-grown companies such as Huawei.

As an investor in Nvidia, I’m hopeful that the company can successfully navigate the issues associated with selling into China, however, other big names, such as Tesla (Nasdaq:TSLA), have failed to maintain revenues and margin.

Tesla is embroiled in a brutal price war in China, and to maintain sales against a rising tide of competition from established automakers and new EV players like BYD and Xiaomi, Tesla has been forced to slash prices across multiple models.

These aggressive price cuts have come at a cost to Tesla’s profits, which are shrinking at an alarming rate in China. Domestic manufacturers, such as BYD, offer significantly cheaper cars, which can be around a third of Tesla’s cheapest option.

I’ve previously covered the travails of Intel and AMD in the Chinese market

Nvidia’s Financials

Overall, the last quarterly report painted a picture of a flourishing company with a dominant position in AI technology and laudable long-term growth prospects.

Revenue surged by 262% year-over-year, driven by the data center segment, and the company’s AI-related business is expected to continue its impressive growth.

Indeed, it was hard to find any negatives at all. The report went on to highlight the company’s increasing profitability, resulting from high levels of operational leverage and a move towards higher-margin products such as the Blackwell range. And given the growth in all things AI, investors are doubtless anticipating further above expected returns going forward.

Let us not forget the announced 10 for 1 stock split, which typically propels a stock price in an investor-pleasing direction.

Now, to address potential impediments for success in China. The challenges involved in the Chinese markets due to export restrictions were addressed, and the company has a strategy to overcome the hurdles set by the US government. In fact, the company suggested that additional competition from Chinese companies would galvanise Nvidia to innovate even more.

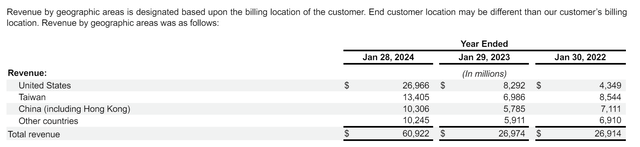

According to Nvidia’s most recent Form 10-K filing, China accounts for around 17% of Nvidia’s total revenues. While “other countries” also accounts for circa 17%. These “other countries” include Western countries and nations outside of the influence of the collective West; Indonesia and Russia, for example.

Nvidia’s regional sales (Nvidia Form 10 K)

In recent years, US export restrictions have limited the types of chips Nvidia can sell in China. As we all know, the most advanced AI chips have been banned. But now, even those designed specifically for the Chinese market as a result of restrictions have been put on the banned-for-sale list.

To address this, Nvidia have had to develop modified, less powerful versions of its chips to comply with US export controls. In a nutshell, Nvidia is stuck with selling products with specifications way below their most advanced technology.

To say that the situation is fluid would be an understatement. There are ongoing changes in US regulations and enforcement actions, which could all influence what chips Nvidia is able to sell in China.

Huawei

Back in 2023, it was reported that US restrictions on exporting advanced AI chips to China could create an unexpected opportunity for Huawei and their Ascend chips.

Analysts said that Huawei’s Ascend chips were roughly on par with Nvidia’s China chips in terms of raw power, but still fell short in performance. However, the report went on to claim that a challenge lay in developing the software ecosystem built around Nvidia’s CUDA platform. This ecosystem allows for training complex AI models, something Huawei’s CANN alternative struggled with at the time. Technology gurus estimated that it could take Huawei 5-10 years to catch up, but Huawei produced competitive products far sooner than expected.

Latest Reports

Nvidia’s attempt to tackle the Chinese AI chip market with their H20 chip is facing an uphill battle. Despite being their most powerful chip designed specifically for China, the H20 has got off to a weak start. It would appear that there’s an oversupply in the market, forcing Nvidia to slash prices and sell the H20 at a discount compared to Huawei’s competing Ascend 910B chip.

Furthermore, Huawei is expected to ramp up production of their Ascend 910B chip this year, a chip that may even outperform the H20 in some key areas.

I’m sure it can be appreciated that the rise of Huawei as a serious competitor ought to be a major concern for investors.

According to Reuters, analysts are becoming increasingly worried about Nvidia’s long-term prospects in China, a market that contributes significantly to their revenue. And this price war is just one symptom of the intense competition Nvidia faces in China. China’s push for domestic chip development and a government directive to prioritise Chinese chips are additional headaches for Nvidia.

While some Chinese tech giants have placed orders for the H20, overall demand seems low. Government procurement data suggests less interest in the H20 compared to Huawei’s offering. To make matters worse, the need to undercut Huawei on price combined with higher manufacturing costs for the H20 is squeezing Nvidia’s profit margins.

With nearly a million H20 chips expected to be shipped to China in the coming months, it is claimed that Nvidia’s success hinges on their ability to compete effectively on price and performance with Huawei. However, if you ask me, if Nvidia is struggling to sell the H20 cheaper than the Ascend 910B, it’s a very bad omen.

Manufacturing

Huawei has partnered with a number of companies, including China’s biggest chip foundry, SMIC (OTCQX:SIUIF), to produce new advanced chips.

SMIC reportedly plans to manufacture Huawei designed chips without the most advanced extreme ultraviolet (EUV) machines, relying instead on older deep ultraviolet (DUV) technology. The companies are also developing technologies that involve self-aligned quadruple patterning, or SAQP, which will reduce their reliance on high-end lithography.

Whether Huawei and SMIC can use SAQP to achieve mass production of advanced chips remains to be seen. This research and development effort is considered a crucial step for China to potentially achieve self-sufficiency in chip manufacturing.

Once volume production of advanced chips has been accomplished, it seems to me that there are markets outside of China that could be satisfied.

Potential Markets

It’s pretty much common knowledge that Huawei is the equivalent of persona non grata in the collective West. But they are able to sell their wares in nonaligned countries, such as the countries that make up BRICS plus or Indonesia. This being so, it is conceivable that their Ascend range may soon be competing with Nvidia outside China; certainly, Russia.

Potential customers of Huawei could include Chinese data center giant, GDS Holdings Limited (GDS), which is making a big push into Southeast Asia. Reports are that, through a joint venture with Indonesia’s sovereign wealth fund, the company aims to develop a comprehensive data center platform across Indonesia, with their initial focus on building a massive hyperscale data center campus in Batam.

This facility will boast a net floor area of 10,000 sqm and an IT power capacity of 28MW. GDS views this collaboration as a validation of their expertise and a springboard for further expansion within Indonesia.

Another prospect for Huawei’s chips has to be Tencent Holdings Limited (OTCPK:TCEHY), a well-known Chinese cloud company. As early as 2012, the company built a facility in Jakarta, which is now fully operational. Apart from Indonesia, Tencent has data centres in; the US, Singapore, Russia, Germany, Canada, and India. And there have been a slew of articles describing Tencent’s push into MENA.

Risks

As previously mentioned, this article gives an alternative to the perpetually positive narrative that can be read frequently in the media. And, I am the first to admit that there are risks to this less-than-gung-ho-bullish thesis. First of all, countries outside the collective West may insist on the best, and at this point in time, no company comes close to Nvidia’s offering.

Secondly, even if some business is lost in China, and that seems highly likely, expansion in revenues outside of China are set to rise quite impressively.

Summary

It is clear that US restrictions have knobbled Nvidia’s plans to sell their most advanced AI chips in China, forcing them to attempt to flog lower specification versions. To complicate matters, Huawei has emerged as a serious competitor.

Huawei’s Ascend chips are gaining traction and could outperform Nvidia’s H20 in the Chinese market. Of course, a lower demand for the H20 and a price squeeze could impact Nvidia’s profits.

Then there is always the possibility that, at some stage, Huawei could carve out a foothold in other countries through Chinese data center focused corporations.

Read the full article here