The Pioneer Floating Rate Fund (NYSE:PHD) is a closed-end fund that income-seeking investors can purchase as a means of achieving their goals of earning a high level of income from their portfolios. The fund does fairly well at this, as it boasts an 11.54% yield at the current share price. This yield compares reasonably well with that of the fund’s peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Pioneer Floating Rate Fund |

Fixed Income-Taxable-Senior Loans |

11.54% |

|

Apollo Senior Floating Rate Fund (AFT) |

Fixed Income-Taxable-Senior Loans |

11.41% |

|

BlackRock Floating Rate Income Trust (BGT) |

Fixed Income-Taxable-Senior Loans |

11.15% |

|

Eaton Vance Floating Rate Income Trust (EFT) |

Fixed Income-Taxable-Senior Loans |

10.65% |

|

First Trust Senior Floating Rate Income Fund II (FCT) |

Fixed Income-Taxable-Senior Loans |

11.28% |

|

Nuveen Floating Rate Income Fund (JFR) |

Fixed Income-Taxable-Senior Loans |

11.74% |

As we can clearly see here, with the notable exception of the Eaton Vance Floating Rate Income Trust, all of the peer funds have yields in the 11.25% to 11.75% rate. There is only a fifty basis-point spread here, so any of these looks to be reasonably good at the provision of income. However, that does not mean that all of these funds are the same, as the expense ratio and leverage are different between them. In addition, the actual composition of the portfolios can differ, which affects the risk profile of the fund. As such, we should still have a close look at the Pioneer Floating Rate Fund in isolation in order to determine whether or not it would be a worthy choice among its peers.

Unfortunately, the Pioneer Floating Rate Fund shares the same problem as other leveraged loan and fixed-income funds when it comes to inflation protection. Unlike equities, debt securities do not go up in price in response to rising inflation. After all, corporations will usually see their revenue and net income rise in response to increasing prices throughout the economy (even though profit margins may not go up). This has a beneficial effect on the price of their equities. Debt securities do not benefit from this, and leveraged loans in particular tend to have remarkable price stability over time. We can see this quite simply by looking at the Bloomberg U.S. Floating Rate Note < 5 Years Index (FLOT). As we can see, the index has been very stable over the past ten years:

Seeking Alpha

The price of these securities is not really affected by interest rate movements, recessions, or most other external factors (the exception is broad-market panics). As such, we cannot expect that the Pioneer Floating Rate Fund will help investors protect the purchasing power of their assets against inflation. This is not a problem as long as the yield is above the inflation rate and thus allows for reinvestment. However, as I pointed out in a recent article, the official inflation rate reported by the Bureau of Labor Statistics has faced a great deal of criticism for understating the actual increase in the cost of living. If we accept this, then it is possible that the yield of the Pioneer Floating Rate Fund is too low to fully offset inflation after paying taxes on the distributions. Thus, the lack of inflation protection here could be a problem, and it would be wise to include other assets in a portfolio that will do a better job of holding their real value, as there are plenty of reasons to believe that inflation will be a problem going forward.

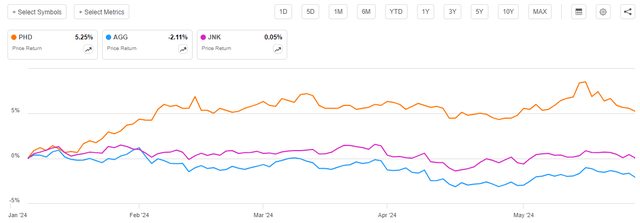

We previously discussed the Pioneer Floating Rate Fund in early January 2024. At the time, I suggested reducing your allocation to fixed-rate bonds and buying this fund for the debt portion of your portfolio holdings. That proved to be the correct move at the time, as the fund’s shares have appreciated by 5.25% since that article was published. The fund has outperformed both investment-grade and junk bonds since early January:

Seeking Alpha

The comparison against investment-grade bonds is particularly stark, as these assets have actually declined in price over the past five months. That was to be expected though, as the thrust of my thesis was that the Federal Reserve would not raise interest rates in either January or March, suggesting that bonds were overpriced at the start of the year. That thesis has proven to be correct.

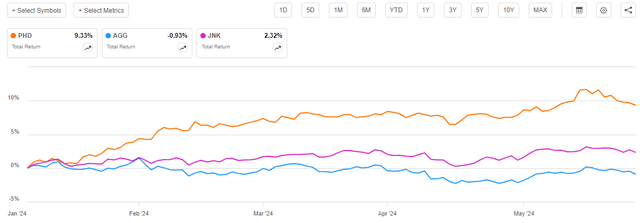

Since the start of this year, investors in the Pioneer Floating Rate Fund have outperformed by even more than the above chart shows. As I stated in a previous article:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

When we include the distributions paid out by both bond indices and the Pioneer Floating Rate Fund since the start of the year in the chart shown above, we get this:

Seeking Alpha

As we can clearly see, investors in the Pioneer Floating Rate Fund have realized a 9.33% total return since January 5, 2024. This is obviously much better than investors in either investment-grade bonds or junk bonds realized over the period. Thus, anyone who purchased this fund following my recommendation earlier in the year is probably reasonably pleased with their purchase.

Naturally, though, several months have passed since that previous article was released and the overall environment in both the market and the economy has changed. Thus, we should revisit this fund and see if it still makes sense to own. The fund has released its annual report since the previous article was published, so this will help us in our task today.

About The Fund

As I mentioned in the previous article on this fund:

The Pioneer Floating Rate Fund is one of the few closed-end funds that does not have a dedicated website. The fund sponsor simply provides a website that lists all of its funds and offers downloadable literature. As such, we are pretty much going to rely on the fund’s monthly fact sheet as our primary source of information about the fund itself since that seems to be the closest thing that this fund has to its own website.

The most recent fact sheet available for the Pioneer Floating Rate Fund is dated April 30, 2024, so it is fairly recent. I updated the link in the quote to point to this document.

According to the fund’s most recent fact sheet, the Pioneer Floating Rate Fund has the primary objective of providing its investors with a high level of current income. This makes a lot of sense given the strategy that the fund uses, which the fact sheet describes:

The Fund seeks a high level of current income by investing primarily in floating-rate loans. It also seeks capital preservation as a secondary objective to the extent consistent with its primary goal.

The fund’s annual report states that its asset allocation as of November 30, 2023 was the following:

|

Asset Type |

% of Net Assets |

|

Senior Secured Floating Rate Loan Interests |

122.3% |

|

Common Stocks |

0.5% |

|

Asset-Backed Securities |

3.0% |

|

Collateralized Mortgage Obligations |

2.6% |

|

Commercial Mortgage-Backed Securities |

1.0% |

|

Corporate Bonds |

11.1% |

|

Preferred Stock |

0.1% |

|

Insurance-Linked Securities |

1.6% |

|

U.S. Government and Agency Obligations |

4.8% |

Obviously, not everything listed here is a floating-rate security. For the most part, the senior secured floating-rate loans, some of the asset-backed securities, the collateralized mortgage obligations, and the commercial mortgage-backed securities all have floating-rate coupons that adjust based on some benchmark, usually the thirty-day average secured overnight financing rate.

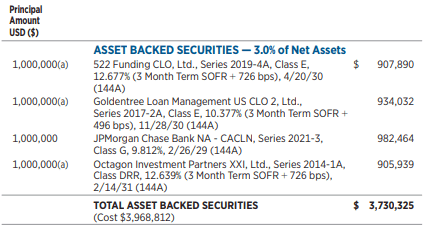

However, not all of the asset-backed securities are floating-rate securities. Here are the asset-backed securities shown in the fund’s annual report:

Fund Annual Report

The JPMorgan Chase Bank NA – CACLN security issue is not a floating-rate security. That particular security has a fixed 9.812% coupon. This is certainly a pretty attractive rate, especially in the eyes of someone who is used to the ultra-low interest rate environment that has been dominant in the United States and most other developed countries over the past decade. However, since that is a fixed-rate security, we can expect that its price will move inversely to interest rates just like any other bond.

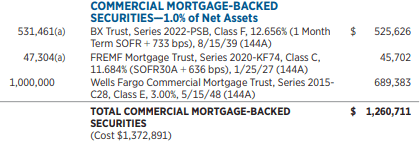

All of the collateralized mortgage obligations in the fund are floating-rate assets. However, not all of the commercial mortgage-backed securities are floating-rate assets. Here are the commercial mortgage-backed securities that this fund was holding as of the date of the annual report:

Fund Annual Report

The Wells Fargo Commercial Mortgage Trust is not a floating-rate security. It is a fixed-rate bond backed by a pool of commercial mortgages paying 3.00%. That is a remarkably low coupon rate right now, especially since the other two commercial mortgage-backed securities in this portfolio are paying double-digit interest rates in today’s environment. That low-interest rate is something that may be a bit off-putting to some investors, especially because commercial mortgages are not considered to be the safest asset class right now. The sector has been facing turmoil as falling valuations for office buildings and some other urban commercial properties have met with rising vacancy rates and prompted some borrowers to default on their mortgages. As of right now, there does not appear to be a catalyst to turn this situation around, so a 3.00% interest rate is insufficient to compensate investors for taking on this risk. It is possible, though, that this fund purchased the security at a price below face value, so the actual amount that it is receiving is higher than 3.00%. The fund does not, unfortunately, disclose the yield-to-maturity nor the yield-on-cost of any of the assets in its portfolio.

The corporate bonds listed in the fund’s asset allocation chart above are all fixed-rate junk bonds. Those account for 11.1% of the fund’s net assets. Thus, we can immediately see that a not insignificant percentage of this fund’s assets are not invested in floating-rate securities. This does mean that this fund’s portfolio will have higher interest-rate risk than we might expect from a leveraged loan fund, so potential investors should keep that in mind when purchasing this fund. Fortunately, though, the fact that the fund’s share price went up along with interest rates year-to-date does suggest that the interest-rate risk here is lower than it would be with any fixed-income fund.

In my previous article on the Pioneer Floating Rate Fund, I pointed out that the majority of the assets held by the fund are below-investment-grade securities:

The Pioneer Floating Rate Fund is not without risks, however. One of the biggest ones comes from the fact that senior loans are typically backed by companies that may not have the strongest balance sheets. This is one of the reasons why the fund is able to sport a double-digit yield despite the fact that Treasuries are only yielding 4.5% to 5.5% depending on the maturity date.

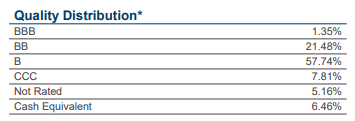

In that article, I showed a chart detailing the fund’s holdings by credit rating. Here is a more current chart showing the same:

Fund Fact Sheet

This table compares the fund’s credit rating profile today compared to at the start of the year:

|

Credit Rating |

% of Portfolio Today |

% of Portfolio Previously |

% Change |

|

BBB |

1.35% |

1.26% |

+0.09% |

|

BB |

21.48% |

21.96% |

-0.48% |

|

B |

57.74% |

58.58% |

-0.84% |

|

CCC |

7.81% |

8.83% |

-1.02% |

|

Not Rated |

5.16% |

5.26% |

-0.10% |

|

Cash Equivalent |

6.46% |

4.11% |

+2.35% |

We can immediately see that the fund has improved the credit quality of its portfolio since our previous discussion. In particular, it increased its allocation to investment-grade credit and cash-equivalent securities. The fund slightly decreased its allocation to every type of junk debt, although it does appear that the riskier securities had their allocation decreased more than the higher-rated junk debt. After all, we can immediately see that the CCC-rated securities experienced the largest decline in their allocation over the period. Meanwhile, the highest-rated things held by the fund (cash equivalents) experienced the greatest increase in weighting. This could suggest that the fund’s management is positioning the portfolio for a “higher for longer” environment, since such an environment would likely result in a higher default rate for the riskiest debt. As regular readers likely know, I am expecting that the Federal Reserve will have difficulty cutting rates if it wishes to keep inflation under control, so I can generally agree with the fund’s management here.

Risk-averse investors could also derive a certain amount of comfort from the fund’s apparent attempt to improve the credit quality of its assets. After all, securities with a higher rating are less likely to suffer from losses as the issuers are less likely to default. The fund therefore appears to be attempting to satisfy its secondary objective of preservation of capital. Retirees and others who are dependent on their portfolios for income may have difficulty obtaining new principal to replace any lost to defaults, so they will probably appreciate this.

Leverage

As is the case with most closed-end funds, the Pioneer Floating Rate Fund employs leverage as a method of boosting the income that it generates from its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate debt and similar income-producing securities with variable yields. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will normally be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I do not typically like a fund’s leverage to exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Pioneer Floating Rate Fund has leveraged assets comprising 31.90% of its assets. This is obviously well below the one-third of assets threshold that we would ordinarily prefer to see. It is also significantly below the 32.90% leverage ratio that the fund had at the time of our last discussion in early January.

It is not surprising that the fund’s leverage ratio has decreased since early January. After all, the fund’s net asset value is up 1.67% since that article was published:

Barchart

As some readers might notice, the fund’s net asset value did not increase by nearly as much as its leverage did over the past few months. This is something that will have implications for its current valuation, as we will discuss later in this report. For our purposes right now, an increase in net asset value typically results in a decrease in the fund’s leverage ratio, for reasons that we have discussed in numerous previous articles.

Here is how the Pioneer Floating Rate Fund compares to its peers in terms of leverage:

|

Fund Name |

Leverage Ratio |

|

Pioneer Floating Rate Fund |

31.90% |

|

Apollo Senior Floating Rate Fund |

35.64% |

|

BlackRock Floating Rate Income Trust |

22.99% |

|

Eaton Vance Floating-Rate Income Trust |

37.00% |

|

First Trust Senior Floating Rate Income Fund II |

14.07% |

|

Nuveen Floating Rate Income Fund |

37.99% |

(All figures from CEF Data)

As we can clearly see, the leverage ratio of the Pioneer Floating Rate Fund is right around the median of its peer group. This tells us that the fund is not using an excessive amount of leverage for its strategy. Overall, investors should be able to sleep reasonably well at night here.

Distribution Analysis

The primary objective of the Pioneer Floating Rate Fund is to provide its investors with a high level of current income. To this end, the fund pays a monthly distribution of $0.0925 per share ($1.11 per share annually), which gives it an 11.54% yield at the current share price.

The fund has not been especially consistent with respect to its distribution over its history:

CEF Connect

As I stated previously:

This may prove to be a turn-off for those investors who are seeking to earn a safe and consistent income from the assets in their portfolios. However, it is hardly something that is unexpected considering the nature of the securities that the fund invests in. After all, as we have already seen, floating rate securities are incredibly stable over time and are generally immune to the price changes that would otherwise accompany swings in interest rates. As such, the return that investors will receive is directly dependent on the coupon that these securities pay and that is a function of short-term interest rates. Thus, we can generally expect that this fund’s distributions will increase when the federal funds rate goes up and vice versa. This is one of the reasons why it has raised its distribution over the past twelve months, which actually works out well for those investors who need extra money to cover the rising cost of living in today’s inflationary environment.

As mentioned in the introduction, the fund has released an updated financial report that we can consult to determine the fund’s ability to sustain its distribution. This report corresponds to the full-year period that ended on November 30, 2023, so it is obviously a few months old at this point. However, it is more recent than the report that we had at the time of our previous discussion, so it should work well to provide us with an update.

For the full-year period that ended on November 30, 2023, the Pioneer Floating Rate Fund received $18,945,048 in interest and $340,032 in dividends from the assets in its portfolio. This gives the fund a total investment income of $19,285,080 for the period. The fund paid its expenses out of that amount, which left it with $14,008,068 available for shareholders. That was sufficient to cover the $13,272,116 that the fund paid out in distributions during the period.

Thus, it appears that this fund is simply paying out its net investment income as a distribution. The fund did the same thing in the previous full-year period, so this appears to be a recurring theme for it. As such, we probably do not need to worry too much about this fund right now. It will cut its distribution when its net investment income declines, which will almost certainly occur once the Federal Reserve cuts its benchmark rate. Thus, the distribution is not technically sustainable over the long term. However, we also do not need to worry about the fund unnecessarily depleting its asset base by paying out a larger distribution than it can afford.

Valuation

Shares of the Pioneer Floating Rate Fund are currently trading at a 7.52% discount to net asset value. This is very much in line with the 7.53% discount that the shares have had on average over the past month. Thus, the current price appears to be a reasonable entry point if you wish to add this fund to your portfolio today.

Conclusion

In conclusion, the Pioneer Floating Rate Fund appears to be a decent holding for income-focused investors right now. The fund’s yield is one of the highest around, due mostly to the fact that short-term rates are significantly higher than long-term rates at present. The fund has apparently been reducing the credit risk of its portfolio, which may be a good thing in a “higher for longer” environment that sees defaults increase. Finally, the fund is fully covering its distribution and trades at a reasonably attractive valuation.

The only real downside here is that the yield might not be high enough to keep up with the cost of living if you are holding the fund in a taxable account.

Read the full article here