The Advent Convertible & Income Fund (NYSE:AVK) is a closed-end fund, or CEF, that income-seeking investors can purchase as a method of achieving their goals. The AVK fund certainly manages to do fairly well at this task, as the fund’s shares currently boast an 11.93% distribution yield. Despite today’s current high interest rate environment, this is a much more attractive yield than that possessed by most broad market indices:

|

Index |

TTM Yield |

|

S&P 500 Index (SP500) |

1.35% |

|

Bloomberg U.S. Aggregate Bond Index (AGG) |

3.41% |

|

Bloomberg U.S. Floating Rate Note < 5 Yrs. Index (FLOT) |

5.86% |

|

Bloomberg High Yield Very Liquid Index (JNK) |

6.60% |

At first glance then, investors who are seeking a high level of income may immediately favor the Advent Convertible & Income Fund over any of the broad market indices. Another advantage that this fund has going for it is that investors in it do not need to sacrifice all of the upside potential that could be obtained from an investment in common equity. As we can immediately see, common stocks have substantially lower yields than fixed-income securities, but they make up for it with a much higher potential for growth and capital gains. This fund, on the other hand, is able to deliver the best of both worlds due to the nature of the securities in which it invests.

The current yield of the Advent Convertible & Income Fund also compares fairly well to other closed-end funds that employ a similar strategy. We can see that here:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Advent Convertible & Income Fund |

Fixed Income-Taxable-Convertibles |

11.93% |

|

Bancroft Fund (BCV) |

Fixed Income-Taxable-Convertibles |

8.22% |

|

Calamos Convertible Opportunities and Income Fund (CHI) |

Fixed Income-Taxable-Convertibles |

10.18% |

|

Ellsworth Growth & Income Fund (ECF) |

Fixed Income-Taxable-Convertibles |

6.43% |

|

High Income Securities Fund (PCF) |

Fixed Income-Taxable-Convertibles |

11.19% |

|

Virtus Convertible & Income Fund (NCV) |

Fixed Income-Taxable-Convertibles |

12.71% |

As we can immediately see, the Advent Convertible & Income Fund has a higher yield than that possessed by any of its peers, except for the Virtus Convertible & Income Fund. However, that fund has several problems, which we discussed in an article that was published two weeks ago. The Virtus Convertible & Income Fund also has underperformed most of the peers on this list over the past few years, so it will probably not be the most attractive choice for investors that are seeking a high level of income despite its higher yield. The Advent Convertible & Income Fund is overall likely to be more appealing to most investors, for reasons which we will discuss in this article.

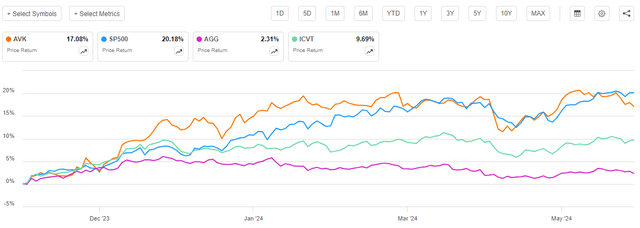

As regular readers can undoubtedly recall, we previously discussed the Advent Convertible & Income Fund back in November. The equity market has generally been quite strong since that time, but the fixed-income market has been much more volatile. Despite this, the Advent Convertible & Income Fund managed to deliver a 17.08% gain. This was not as good as the 20.18% gain that the S&P 500 Index delivered over the period, but this fund managed to outperform both domestic investment-grade bonds and the Bloomberg US Convertible Cash Pay Bond Index (ICVT):

Seeking Alpha

This is something that certainly looks promising, as the fund managed to deliver a very attractive performance when compared to that of some of the indices that investors might choose as an alternative to this fund. However, we can still see that it did not manage to outperform common stocks (although it did manage to temporarily get ahead of them) over the period. This is expected, as this fund is investing in assets that are theoretically less risky than common equities.

However, as I stated in a previous article:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

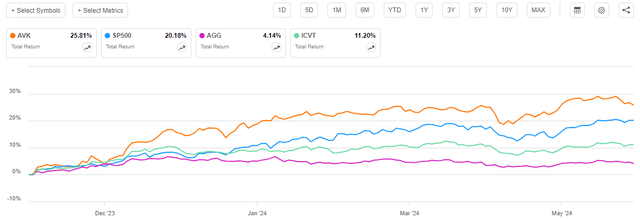

When we include the distributions paid out by the index funds as well as the Advent Convertible & Income Fund shown in the previous chart, we get this revised chart:

Seeking Alpha

Here, we can very quickly see that investors who put their money into the Advent Convertible & Income Fund back in November 2023 are now richer than investors who put the same amount of money into either common stocks or investment-grade bonds. This fund also managed to outperform the convertible bond index, but that is typical for a leveraged fund during appreciating markets. Thus, overall, this fund appears to offer a combination of strong performance and a high yield. Income-focused investors will undoubtedly be attracted by this.

Naturally, though, past performance is no guarantee of future results. As such, we should take a look at this fund as it is today in order to determine whether or not it makes any sense at all to purchase it.

About The Fund

According to the fund’s website, the Advent Convertible & Income Fund has the primary objective of providing its investors with a very high level of total return. This makes a lot of sense given the fund’s strategy, which the website explains in great detail:

The Fund’s investment objective is to provide total return, through a combination of capital appreciation and current income. Under normal market conditions, the Fund will invest at least 80% of its managed assets in a diversified portfolio of convertible securities and non-convertible income securities. Under normal market conditions, the Fund will invest at least 30% of its managed assets in convertible securities and up to 70% of its managed assets in lower-grade, non-convertible income securities, although the portion of the Fund’s assets invested in convertible securities and non-convertible income securities will vary from time to time consistent with the Fund’s investment objective, changes in equity prices and changes in interest rates and other economic and market factors. The Fund may invest without limitation in securities of foreign issuers and the Fund’s investment in foreign securities may vary over time in the discretion of the Fund’s investment advisor.

Thus, the Advent Convertible & Income Fund invests its assets in a combination of convertible securities and junk bonds. The description above seems to imply that it favors junk bonds over convertibles, but in fact, the reverse is true. The quote above does provide a minimum of 30% that must be invested in convertible securities, but there is no actual minimum for junk bonds. The strategy description simply says that convertibles plus junk bonds must total at least 80%. Thus, the actual minimum for junk bonds is 80% minus whatever the fund’s current convertible allocation is. This, therefore, shows a marked preference for convertible securities, but it does allow the fund to have only a minority of its assets invested in such securities in certain market conditions. That is something that could have come in very handy back in late 2021 and early 2022 when the pandemic-era bubble in convertible debt burst:

Seeking Alpha (edited by Author)

Junk bonds also took a beating during the same era, but they did not fall nearly as far:

Seeking Alpha (edit by Author)

Thus, the Advent Convertible & Income Fund could have avoided some of the worst of that bubble bursting by underweighting convertible securities in favor of junk bonds during that period of time. With that said, the fund’s net asset value did suffer quite a bit during that period though, but investors in the fund have still realized a 49.86% total return over the past five years. Thus, it appears that the fund managed to navigate the past few years better than some of its peers, such as the two Virtus convertible funds.

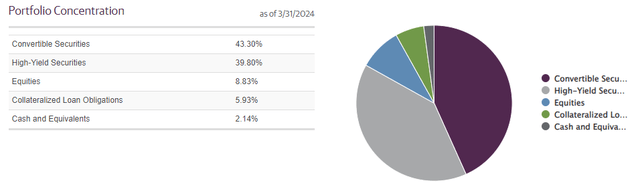

As of right now, the fund has a higher weighting to convertible securities than to junk bonds:

Guggenheim Investments

This is similar to what we saw the last time that we discussed the fund. However, there are a few changes:

|

Asset Type |

Today’s Weighting |

Previous Weighting |

% Change |

|

Convertible Securities |

43.30% |

46.38% |

-3.08% |

|

High-Yield Bonds |

39.80% |

38.00% |

+1.80% |

|

Equities |

8.83% |

8.50% |

+0.33% |

|

Collateralized Loan Obligations |

5.93% |

5.28% |

+0.65% |

|

Cash and Equivalents |

2.14% |

1.84% |

+0.30% |

The big thing that we notice here is that the fund’s allocation to convertible securities declined over the past eight months. In contrast, its junk bond and cash allocations went up. This is somewhat surprising, as junk bonds have underperformed convertible securities year-to-date, by quite a lot:

Seeking Alpha

However, there were some periods in which junk bonds were outperforming convertibles. Junk bonds also have delivered a higher total return year-to-date due to their higher yields:

Seeking Alpha

It thus could make some sense for the fund to be increasing its allocation to junk bonds and reducing the convertible securities weight. However, another thing that we see is that junk bonds have exhibited much more price stability than convertible bonds year-to-date. This, especially when combined with the rising cash position, could suggest that the fund managers are trying to reduce the fund’s volatility in today’s somewhat uncertain and increasingly liquidity-strained market. That is not a bad idea, especially considering that this fund is using leverage. Volatility is the enemy of leverage, after all. Overall, risk-averse investors could appreciate the changes that we see here.

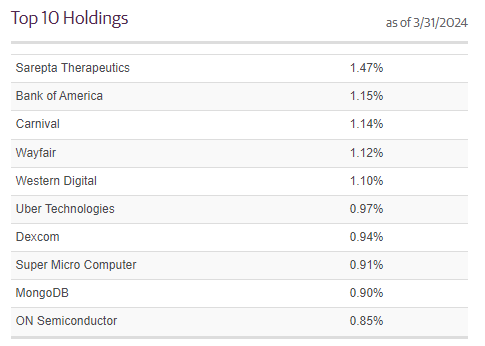

Here are the largest issuers whose securities are held by the fund as of March 31, 2024:

Guggenheim Investments

I will admit that I would have preferred a more recent date than March 31, 2024, but this fund does not publicly release updated information about its holdings monthly. As is usually the case with closed-end funds, we have to use the information that we have, which may be a month or two out of date. The Advent Convertible & Income Fund has a 116.00% annual turnover, so it is possible that something on the list has changed in the past two months.

The only two companies on this list that were also among the fund’s largest positions the last time that we discussed this fund are Bank of America (BAC) and DexCom (DXCM). Everything else among the fund’s largest positions list has been added to the portfolio within the past few months. The removed companies include Ford (F), Norwegian Cruise Line (NCLH), Nabors Industries (NBR), Marriott International (MAR), Southwest Airlines (LUV), Match Group (MTCH), and Zillow (Z). This is obviously a substantial number of changes to the portfolio, but it is not really surprising given the high annual turnover.

In fact, the Advent Convertible & Income Fund has a much higher annual turnover than most of its peers:

|

Fund Name |

Portfolio Turnover |

|

Advent Convertible & Income Fund |

116.00% |

|

Bancroft Fund |

44.00% |

|

Calamos Convertible Opportunities and Income Fund |

39.00% |

|

Ellsworth Growth & Income Fund |

47.00% |

|

High Income Securities Fund |

52.00% |

|

Virtus Convertible & Income Fund |

107.00% |

(All figures are as of the most recent financial report issued by each fund.)

The fact that the Advent Convertible & Income Fund has the highest turnover here could be a sign that it is unnecessarily incurring trading costs. However, the fund is the second-highest performer of this peer group over the past five years:

Seeking Alpha

As we can see, only the Calamos Convertible Opportunities and Income Fund managed to outperform the Advent Convertible & Income Fund over the period. Thus, if the fund’s trading costs are weighing on its performance, we can overlook it as ultimately the fund’s performance after expenses is the thing that we care the most about.

Leverage

As is the case with most closed-end funds, the Advent Convertible & Income Fund employs leverage as a method of boosting the effective yield and total return that it earns from the assets in its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and uses that borrowed money to purchase convertible securities, junk bonds, and other income-producing assets. As long as the purchased assets deliver a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the fund’s portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

With that said, this strategy is much less effective at boosting portfolio yields today than it was a few years ago when money was basically free. This is because the difference between the rate at which the fund can borrow and the rate that it receives from the purchased securities is much narrower than it used to be.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much debt as that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

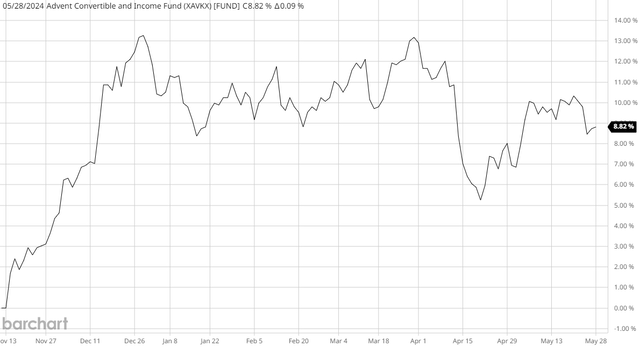

As of the time of writing, the Advent Convertible & Income Fund has leveraged assets comprising 42.88% of its portfolio. This is much better than the 47.44% leverage ratio that the fund had back at the start of November, which is understandable. After all, the fund’s net asset value has increased by 8.82% over the period:

Barchart

This means that the fund’s portfolio has increased in size. It should be obvious that would reduce the proportion of debt to the total portfolio’s size.

The Advent Convertible & Income Fund still has a leverage ratio that is well above the one-third of assets levels that we would ordinarily prefer, even though it has declined over the past eight months. The fund also has a substantially higher level of leverage than any of its peers, as clearly shown here:

|

Fund Name |

Leverage Ratio |

|

Advent Convertible & Income Fund |

42.88% |

|

Bancroft Fund |

21.00% |

|

Calamos Convertible Opportunities and Income Fund |

37.90% |

|

Ellsworth Growth & Income Fund |

24.00% |

|

High Income Securities Fund |

0.00% |

|

Virtus Convertible & Income Fund |

36.95% |

(All figures from CEF Data.)

This could explain why the fund has seemingly been trying to reduce its volatility. A high level of leverage amplifies downward movements when asset prices decline, so volatility can potentially be very problematic for a fund that has a high level of leverage. This is the reason why some of the infrastructure closed-end funds were nearly wiped out by the COVID-19 pandemic, even though midstream partnerships have been some of the best-performing assets since that date. Unlevered funds were able to avoid the losses that were caused by leverage. The same is true here, and given this fund’s high level of leverage, we do not want it to be investing heavily in assets that will exhibit significant price swings.

A risk-averse investor may want to consider the risks related to the fund’s leverage. There are a few potential near-term catalysts that could move the assets held by this fund downward. These include:

- The U.S. economy entering into a recession,

- A failure by the Federal Reserve to cut interest rates this year,

- Problems in the commercial mortgage market, sparking a panic-driven market sell-off,

- Investors not liking the outcome of the American elections in November.

While none of these should be taken as a prediction, they are all risks that investors may want to consider, since any of these events could have an adverse impact on both junk bonds and convertible securities. The Advent Convertible & Income Fund could experience a greater net asset value and price decline than some of its peers should one of these events happen due to its high degree of leverage. Investors should therefore be cognizant of the risks before taking a position in the fund and ensure that they are comfortable with them.

Distribution Analysis

The primary investment objective of the Advent Convertible & Income Fund is to provide its investors with a high level of total return. However, like most closed-end funds, it aims to pay out its investment profits to the shareholders in the form of distributions. As such, the fund pays a monthly distribution of $0.1172 per share ($1.4064 per share annually), which gives it an 11.93% yield at the current share price.

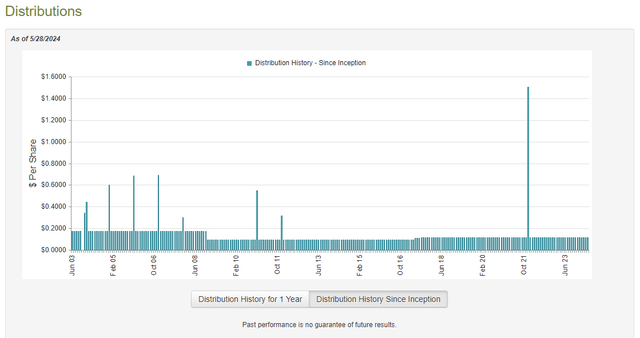

The fund has not been perfectly consistent regarding its distributions over the years:

CEF Connect

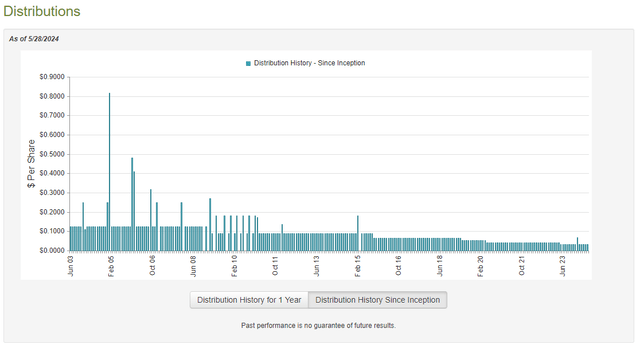

However, it has certainly done better than many other convertible bond funds in this respect. After all, funds such as the Virtus Convertible & Income Fund have been reducing their distributions repeatedly over the past several years. We can see this clearly in this chart, which shows the distribution history of the Virtus Convertible & Income Fund:

CEF Connect

Note the stark contrast between the two funds. The Advent Convertible & Income Fund did reduce its payout back during the subprime mortgage crisis, but otherwise it has generally kept it stable or increased it. The Virtus Convertible & Income Fund, which uses a very similar strategy, has been cutting its distribution over the past fifteen years.

As I pointed out in the previous article:

[The distribution history of the Advent Convertible & Income Fund] will certainly appeal to any investor who is seeking to earn a safe and consistent income from the assets in their portfolios. However, there are very few funds that were not adversely affected by the rising rate environment over the past two years. In fact, pretty much the only funds that actually saw their performance improve consistently are those ones that invest in energy infrastructure companies or floating rate securities. This fund does neither, so it seems likely that it has taken some losses that have caused the distribution to have a destructive effect on its net asset value.

I went on to show that the fund’s net asset value has indeed fallen over the past three to five years. This suggests that the fund is not actually covering its distribution. We should investigate this further.

As of the time of writing, the most recent financial report for the Advent Convertible & Income Fund is the annual report that corresponds to the full-year period that ended on October 31, 2023. While this report is several months old at present, it is newer than the one that we had at the time of our last discussion, so it should work fine as an update.

For the full-year period that ended on October 31, 2023, the Advent Convertible & Income Fund received $33,587,285 in interest along with $4,030,467 in dividends from the assets in its portfolio. This gives the fund a total investment income of $37,617,752 for the period. The fund paid its expenses out of this amount, which left it with $13,089,343 available for shareholders. That was not enough to cover the $48,652,676 that the fund actually paid out in distributions over the period.

The fund was unable to make up the difference through capital gains. For the full-year period, it reported net realized losses of $16,412,964, which were amplified by $3,698,919 net unrealized losses. Obviously, these losses did not help the fund cover its distribution at all, which explains why the annual report states that $35,009,622 of the distributions during the full-year period was a return of capital. That means that 71.96% of the money that the fund paid out during the most recent fiscal year was not covered by investment profits. Please note though that the tax classification of the distributions may differ due to the tax year being different from the fund’s fiscal year. Overall, though, we can clearly see that this fund is failing to cover its distribution.

That was the second year in a row for which the fund failed to cover its distribution. Over the past two years, the fund’s net assets have declined by $321,873,734 after accounting for all inflows and outflows. That figure is 46.29% of the fund’s net assets as of November 1, 2021. Clearly, this fund should have reduced its distribution, as the payouts are destroying its net asset value.

While the fund has overall managed to cover its distributions since the closing date of the 2023 fiscal year, its net asset value is still much lower than it was a few years ago. It remains to be seen whether the fund will be able to sustain its distribution at the current level or not, as doing so will require that the market remain as strong as it has been since November 2023. That could be a tall order.

Valuation

Shares of the Advent Convertible & Income Fund currently trade at a 4.01% discount to net asset value. This is slightly better than the 3.66% discount that the shares have averaged over the past month.

Conclusion

In conclusion, investors in the Advent Convertible & Income Fund may want to use caution. The fund failed to cover its distribution for the most recent fiscal year, and its high level of leverage could expose it to more volatility than you may prefer.

The portfolio, however, looks reasonable as the fund’s management appears to be moving its assets into assets that should exhibit greater price stability than the fund had a few months ago. That could be a good thing if the market corrects in the near future. We have seen moderately weak sessions over the past two days, so this might be a good idea. Overall, this is not necessarily a bad fund, but it does look a lot riskier than some of the other convertible funds that we have discussed recently.

Read the full article here