Anyone who has been trading stocks for a long time has most likely experienced a dividend cut.

It’s not something that you want to brag about because it usually means that you lost money.

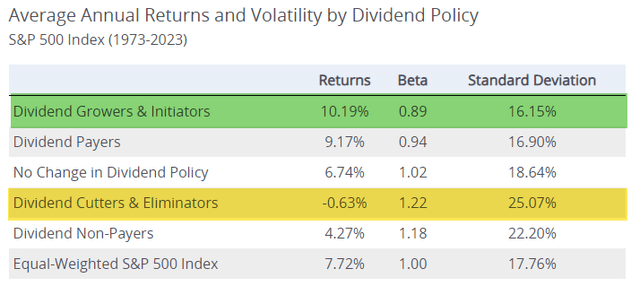

Consider this fact, since 1973 companies that grew their dividend – as opposed to cutting or eliminating the dividend – have experienced the highest returns since 193.

Source: Hartford Funds

That’s stunning, right?

Dividend growers and initiators have returned 10.2% annually over the last five decades compared with dividend cutters and eliminators that have returned -.63% annually over the same time period.

I don’t know about you, but I certainly don’t want to own too many of these rotten eggs that have cut or eliminated their dividend.

But it’s time for some transparency…

I’ve made a few mistakes of my own.

Take for example American Realty Capital (formerly ARCP), a net lease REIT that had amassed a large portfolio of freestanding buildings. On Oct. 23, 2014, I explained that

“My biggest concern with ARCP has to do with the unusually high yield that also signals that the dividend could be in danger of being reduced. Some have argued that a dividend cut would not hurt ARCP; however, I disagree because if the dividend is lowered, the price will also be lowered, and a price that previously was undervalued no longer represents a good value.”

A dividend cut followed and of course, a massive selloff related, as I pointed out,

“ARCP has orchestrated a more complex model and while the current Chairman (and previous CEO) advocates a “size matters” approach (“The World’s Largest Net Lease Company”) in which investors have fueled the growth, many have ignored dividend safety.”

So yes, I took a hit, and fortunately, my losses were mitigated because of my diversified holdings.

Another example comes to mind…

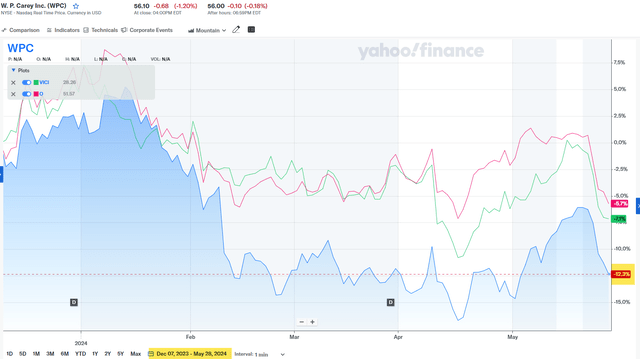

W. P. Carey Inc. (WPC) had spent decades (founded in 1973) building trust among its sticky retail investors. The sale-leaseback pioneer had commenced as an MLP and later converted to a REIT with a formidable track record of increasing dividends.

However, as I pointed out (in February 2024), “…on Dec. 7, 2023, the company declared a quarterly dividend of $.86 per share, down from $1.071 per share paid the prior quarter, representing a dividend cut of 20%.”

To be fair, Carey’s management team had previously telegraphed the spin of its office portfolio into a liquidation REIT known as Net Lease Office Properties (NLOP), which was due to distress in the office sector.

Yahoo Finance

As you can see, WPC has underperformed two of its net lease REIT peers – Realty Income Corporation (O) and VICI Properties Inc. (VICI) – since the announced dividend cut.

Perhaps it’s time to get back on the Carey train?

We’ll see, as I will be meeting with management next week at REIT Week.

But you get my point, right?

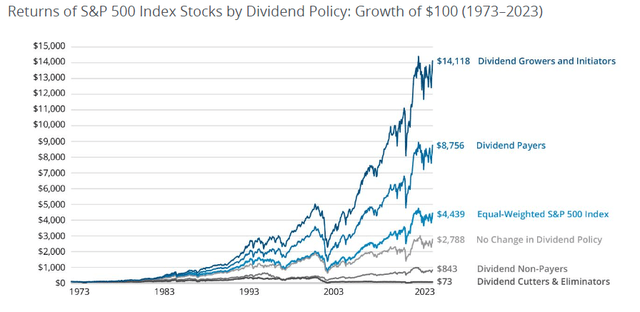

Dividend cuts aren’t good, whether they’re expected or unexpected, and investors should recognize that companies that consistently grow their dividends have historically exhibited strong fundamentals, solid business plans, and a deep commitment to their shareholders.

See this chart below: A picture is worth 1,000 words:

Source: Hartford Funds

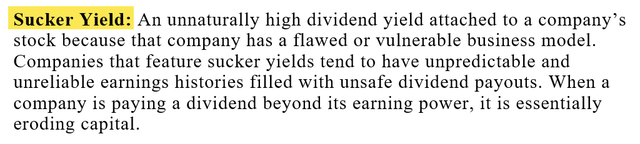

Who’s the Sucker?

I define a “sucker yield” as follows:

Source: Brad Thomas

Obviously, none of us want to invest in a business that has a flawed business model with a history of unreliable earnings and unsafe dividend payouts.

The best way to measure whether a company will be able to pay a consistent dividend is through the payout ratio. The payout ratio is calculated by dividing the yearly dividend per share by the earnings per share (and for REITs, we use Adjusted Funds from Operations).

A high payout ratio means that a company is using a significant percentage of its earnings to pay a dividend. We have used the payout ratio to help investors avoid many dividend cuts.

Now let me provide you with three REITs that are likely to cut their dividend.

Blackstone Mortgage Trust, Inc. (BXMT)

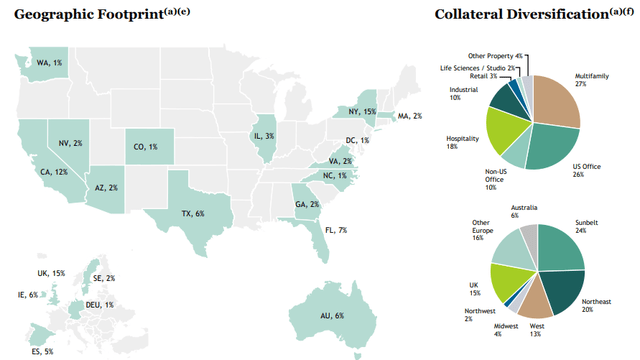

BXMT is an externally managed mortgage REIT (“mREIT”) that specializes in the origination of secured senior loans which are collateralized by commercial real estate (“CRE”) located throughout North America, Europe, and Australia.

The company has a market cap of approximately $2.99 billion and manages a $21.1 billion senior loan portfolio that consists of 173 loans with a weighted average origination loan-to-value (“LTV”) ratio of 63%.

Blackstone Mortgage Trust’s portfolio focuses on floating-rate senior loans that are collateralized by multiple property types including office, multifamily, hospitality, industrial, and retail.

In addition to a diverse property mix, the collateral securing BXMT’s loans is spread across both domestic and international markets. Roughly 63% of the company’s collateral is located in the U.S., 15% is located in the United Kingdom, 6% is located in Australia, and 16% is located in “other Europe.”

Essentially, the company attempts to create value by generating interest income on its secured senior loans.

BXMT – IR

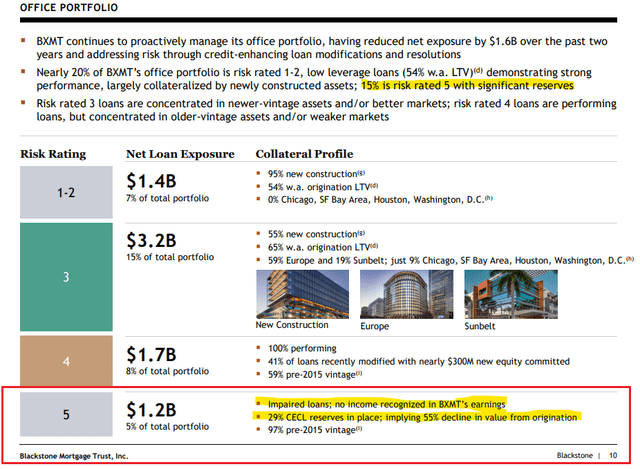

The issue is that BXMT’s portfolio is 26% U.S. Office and 10% non-U.S. Office. Combined, almost 40% of its portfolio is exposed to the office sector.

The company defines levels of risk within its portfolio by using risk ratings that range from 1 to 5. Loans that are risk-rated 1 and 2 are performing, have low leverage, and are typically collateralized by new construction.

By the time you get to a risk rating of 5, the loans are impaired with no income recognized.

5% of BXMT’s total portfolio consists of office loans that are assigned a risk rating of 5. Additionally, risk-rated 5 loans have a 29% current expected credit loss (“CECL”) reserve in place which implies a 55% decline in asset value since origination.

BXMT – IR

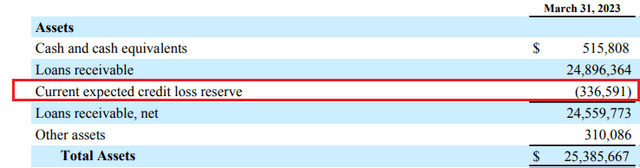

In the first quarter of 2023, BXMT reported a CECL reserve of $336.6 million.

BXMT – IR

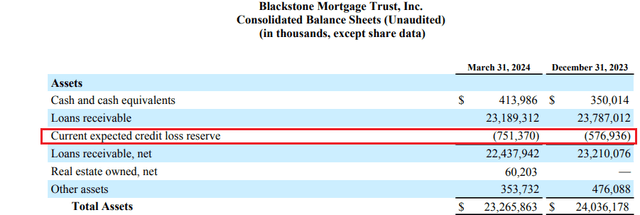

By December 2023 the CECL reserve grew to $576.9 million and as of 1Q-24 the CECL reserve totaled $751.4 million.

BXMT – IR

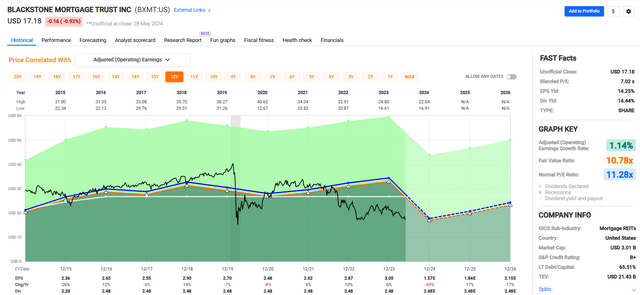

Impaired loans have started to significantly impact earnings. A consensus of analysts expects earnings per share to fall from $3.05 in 2023 to just $1.57 in 2024, representing a decrease of roughly -49%.

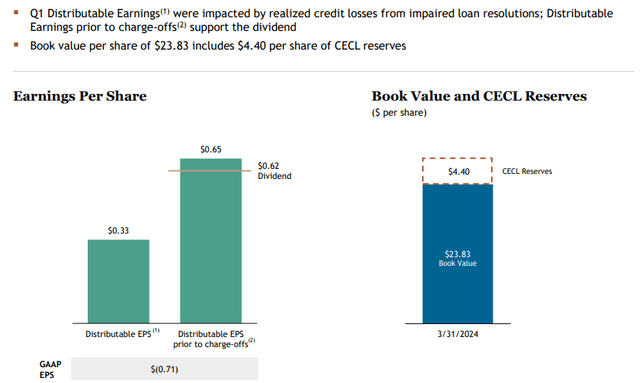

During 1Q-24 the company generated distributable EPS “prior to charge-offs” of $0.65 and paid a $0.62 dividend.

However, after accounting for charge-offs, distributable earnings came in at $0.33 per share, giving the company a Q1 dividend payout ratio of 187.88% when using distributable earnings.

BXMT – IR

In 2023, the company’s dividend was covered with a dividend payout ratio of 81.31%.

However, due to the significant expected drop in earnings, stemming from loan impairments on office properties, the mortgage REITs earnings are not expected to cover its dividend for the next several years.

We believe there’s a good chance BXMT may possibly be forced to cut its dividend due to its heavy exposure to office properties.

Currently, the stock pays a 14.44% dividend yield and trades at a P/E of 7.02x, compared to its normal P/E ratio of 11.28x.

We rate Blackstone Mortgage Trust a Hold due to the challenging payout ratio.

FAST Graphs

Gladstone Commercial Corporation (GOOD)

GOOD is an externally managed REIT that specializes in the acquisition and management of net leased industrial and office properties across the U.S.

The company has a market cap of approximately $616.8 million and a 16.7 million SF portfolio that consists of 132 properties leased to 110 tenants with an occupancy of 98.9% and an average remaining lease term of 6.7 years.

GOOD’s investment strategy is currently centered on single tenant or anchored multi-tenant industrial assets which are leased on a net lease basis. It looks for long lease terms with a target of seven-plus years and engages in sale-leasebacks (“SLBs”), third-party purchases, and build-to-suit projects.

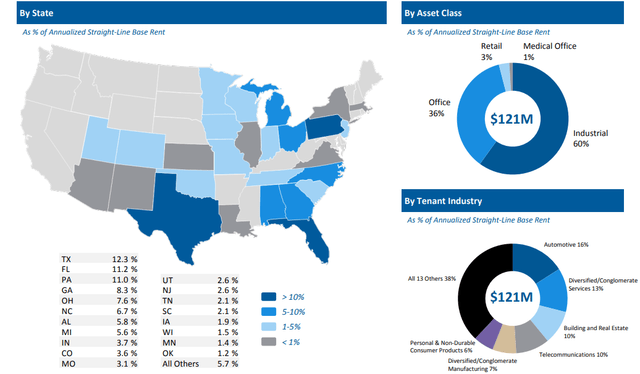

As previously mentioned, the vast majority of GOOD’s investments are in industrial and office real estate. Approximately 60% of the company’s portfolio consists of industrial and 36% consists of office properties. The company also owns retail and medical office buildings which represent 3% and 1% of its portfolio, respectively.

The company’s largest tenant industry is automotive which makes up 16% of its annualized straight-line rent, followed by diversified/conglomerate services at 13% and building and real estate at 10%.

GOOD’s properties are spread across the United States. Its largest concentration is in Texas, where it generates 12.3% of its rent, followed by Florida and Pennsylvania which make up roughly 11% each.

GOOD – IR

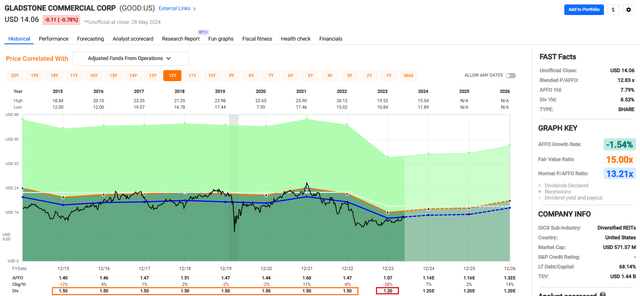

Gladstone released its 1Q-24 operating results earlier this month and reported total operating revenue during the quarter of $35.7 million, compared to total operating revenue of $36.6 million in the first quarter of 2023.

Core FFO during 1Q-24 was reported at $13.9 million, or $0.34 cents per share, compared to Core FFO of $14.99 million, or $0.37 cents per share in the first quarter of 2023. On a per share basis, the change in core FFO represents a year-over-year decrease of almost 9%.

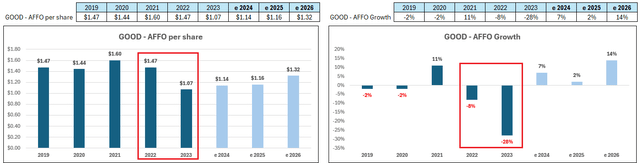

GOOD has had a tough time since the pandemic with AFFO falling from $1.60 per share in 2020 to $1.07 per share in 2023. The company increased its AFFO per share by 11% in 2021, but then AFFO fell by -8% in 2022 and then fell another -28% last year.

The company paid a monthly dividend of $0.125 in 2022, or an annualized amount of $1.50 per share. At the beginning of 2023 it cut its monthly dividend to $0.10, or $1.20 per share annualized, and has maintained its dividend at this rate.

FAST Graphs (compiled by iREIT)

Even after the roughly -20% dividend cut made at the beginning of 2023 the company’s AFFO that year did not cover its dividend. Last year GOOD generated $1.07 per share in AFFO and paid a dividend of $1.20 per share.

Analysts expect AFFO to increase over the next several years to $1.32 per share by 2026. If this pans out then GOOD’s dividend won’t be covered by earnings in 2024 or 2025 and by 2026 the company would have an AFFO payout ratio of ~91%.

I think analyst expectations are optimistic given that GOOD has not had an AFFO payout ratio under 100% since 2015, with the exception of 2018 and 2021 when the payout ratio was 99.67% and 93.89%, respectively.

In my opinion, the company’s dividend policy has not been shareholder-friendly over the recent past decade.

The company maintained its annual dividend rate of $1.50 per share from 2015 to 2022 and then cut it by -20% in 2023. Not to mention the company appears to be in the habit of paying out more than it earns, which is unsustainable.

Currently, the stock pays an 8.53% dividend yield and is trading at a P/AFFO of 12.83x, compared to its normal AFFO multiple of 13.21x.

We rate Gladstone Commercial a Hold due to the unimpressive dividend record.

FAST Graphs

TPG RE Finance Trust, Inc. (TRTX)

TRTX is an externally managed mortgage REIT. The company specializes in the origination and acquisition of debt instruments which primarily consist of first mortgage loans and participation interests in first mortgage loans that are collateralized by commercial real estate in both primary and secondary markets throughout the U.S.

The company primarily focuses on floating rate commercial mortgage loans that are used to finance some form of property improvement or transition, such as redevelopment, re-tenanting, refurbishment or some other form of repositioning.

Periodically, the company will invest in other real estate-related debt products including subordinate mortgage loans, preferred equity, mezzanine loans, as well as collateralized loan obligations (“CLOs”) and commercial mortgage-backed securities (“CMBS”).

When assessing the viability of a mortgage loan, the company targets floating-rate loans on principal balances exceeding $35 million and has an “As-is” LTV of 80%.

The collateral securing the company’s mortgage loans includes multifamily, office, mixed-use, hospitality, industrial, and self-storage.

At the end of 1Q-24, TRTX had a $3.5 billion loan investment portfolio with an average loan size of $69.4 million and a weighted average all-in yield of 9.25%. 100% of its loans are floating-rate and its portfolio has a weighted average risk rating of 3.0 and a W.A. LTV of 67.4%.

TRTX – IR

TRTX has the same issue that many mortgage REITs currently face with approximately 20% of its loan portfolio exposed to the office sector.

The company has significantly reduced its office exposure over the last several years and has achieved a 68% reduction in office loan commitments since the end of 2021.

However, even after the reduction, TRTX has $722.9 million in office loan commitments, which represents roughly 20% of its portfolio.

TRTX – IR

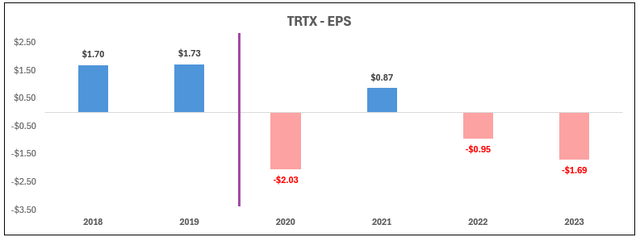

Prior to the pandemic, in 2018 and 2019 TRTX had a dividend payout ratio of 100.80% and 99.60%, respectively. The company was walking a tightrope in terms of its dividend coverage but at least it was generating positive earnings.

Then came the pandemic in 2020 which took TRTX’s earnings per share from $1.73 to negative -$2.00. The company generated positive earnings the following year and reported EPS of $0.87 in 2021, but then earnings fell by -210%, to -1.00 per share in 2022. In 2023, the company once again reported a net loss of -$1.70 per share.

Since the pandemic, TRTX has had a net loss in three out of the last four years.

FAST Graphs (complied by iREIT)

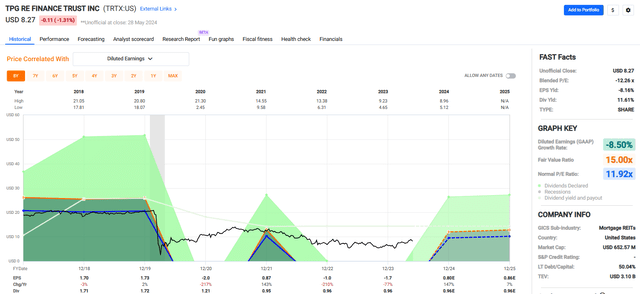

The dividend has followed suit with the 2018 dividend of $1.71 being eroded to just $0.96 per share last year.

Analysts expect the company to generate positive earnings over the next two years. Even if these projections are correct, it would result in a 2026 EPS of $0.86 vs. a 2026 dividend of $0.96, representing a dividend payout ratio of ~111.63%.

It remains to be seen how the company’s dividend policy will take shape over the next several years as it continues to recover from the pandemic.

My bet is that a dividend cut may possibly be likely.

The company is not opposed to such action as it cut its dividend by -29.65% in 2020, and then by -21.49% the following year.

Currently, the stock pays a dividend yield of 11.61%, but this looks like a suckers yield to me. The stock is trading at a P/E of -12.26x compared to its normal P/E ratio of 11.92x.

We rate TPG RE Finance Trust a Hold due to the unimpressive dividend history.

FAST Graphs

In Closing

The dividend cut associated with American Realty Capital (formerly ARCP) was a huge wake-up call for me.

I no longer take the word of any management team, instead, our team conducts granular research to ensure that the dividend is not only safe but sustainable.

Although there was no way that I could have predicted what happened at ARCP, I was able to instinctively downgrade the company to a hold based on a variety of data, including a high payout ratio.

As always, thank you for reading, and I look forward to your comments below.

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

Read the full article here