Note: All amounts discussed are in Canadian Dollars and the stock price refers to the TSX stock price and not the OTC counterpart.

We would buy this here even if Nexus Industrial REIT cut its distribution by 50% tomorrow.

Source: Nexus Industrial: A Look At The Safety Of The 8.5% Yield.

This excerpt is from our coverage from a couple of months ago on Nexus Industrial REIT (TSX:NXR.UN:CA). The reasons were many, and we outlined them in that piece. The NOI boost lurking around the corner due to the below-market rents currently enjoyed by their tenants, balanced lease expirations and debt maturities shielding the portfolio from a hard economic landing, and the stock trading at an over 40% discount to its IFRS NAV, to name a few. While the 8.5% yield was an added incentive, the value was what drove us to add to our existing position, effectively doubling it.

The underlying value is what is most important to us rather than just a high dividend yield. We want to own quality properties at a large discount. Value has rarely been this cheap relative to growth stocks and you want to step up here. We added to our position recently and effectively doubled it. We are maintaining our “buy under $7.50.” as before.

Source: “Nexus Industrial: A Look At The Safety Of The 8.5% Yield.”

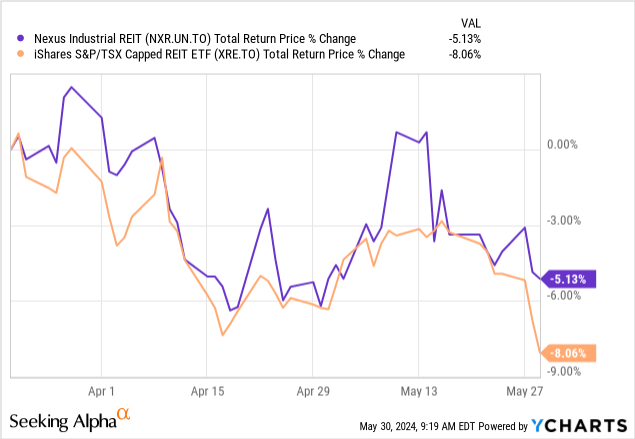

The ride has been anything but smooth since then.

On a total return basis, the dividends have stemmed some bleeding from the price decline.

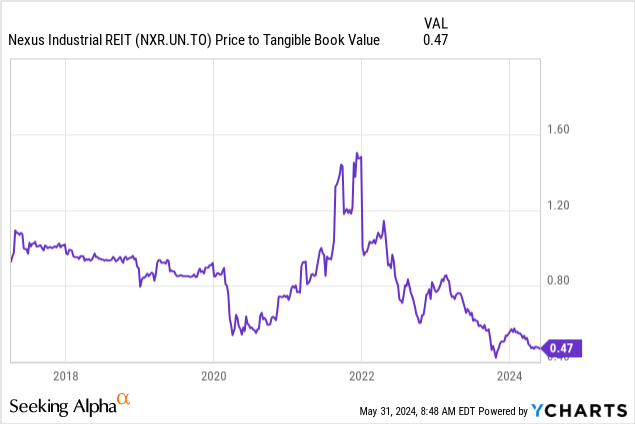

The compelling discount to its tangible book value has deepened, and the dividend is now over 9%. With the payout reaching 100% of the AFFO in Q4-2024, the sustainability of the dividends was in question, but we put the probability of a cut as low.

We had a buy under $7.50 back in March. Let us review the recent numbers to see if we should add more at this time or wait and see.

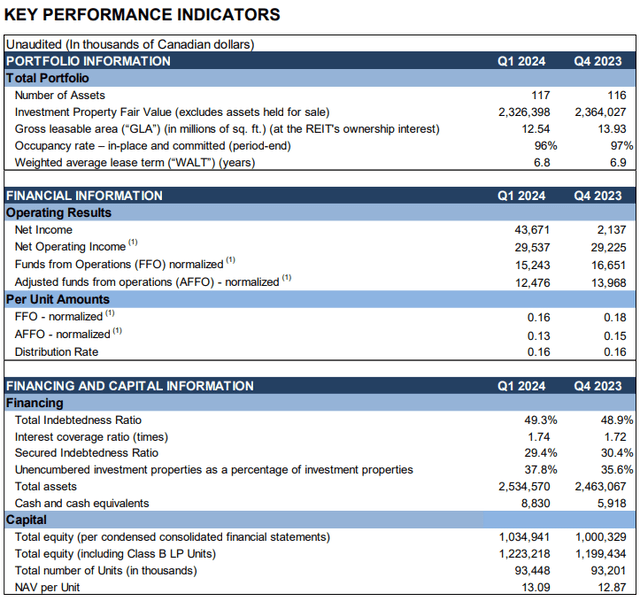

Q1 2024

The first quarter for 2024 was a bit soft, as the REIT was hit with a slightly higher vacancy rate and higher interest expense. Funds from operations came in at 16 cents versus 18 cents last year, and Adjusted FFO (AFFO) dropped to 13 cents.

Q1-2024 MD&A

We will note that both those numbers were below consensus estimates. We generally don’t want to make excuses for the company when they miss, but there was interesting commentary around this that investors should definitely read. Let’s see what they said about the first vacancy.

We realized these vacancies at two properties. The first property was our 29,000 square foot specialty cross-dock building and associated excess land located at 102 Second Avenue in Southeast Calgary.

Our tenant outgrew the location and moved to another building of ours, a newly acquired 83,000 square foot facility at High Plains Drive in Rocky View, Northeast of Calgary. This left the property vacant for the part of the quarter. However, we have leased this space to a new tenant for the building portion effective August 1st.

And since the excess land is well located and is not required by the new tenant, we have an opportunity to construct a new 115,000 square foot small bay industrial building on the property, a highly desirable build in this location. At market rates, this will return approximately a 12% yield on a $15 million investment, which we expect to complete in early 2025. Combined, this will bring us ahead of where we were with the Canada Cartage as a sole tenant.

Source: Nexus Q1-2024 Conference Call Transcript.

That is a fairly solid outcome and one that continues to point out that quality industrial space remains in deficit. Let’s look at the second one.

The second property was our 220,000 square foot Exeter Road building, multi-tenant property in London, Ontario. During the quarter, one of our tenants vacated to upsize from their 44,000 square foot space to a 70,000 square foot space in another one of our buildings at a significant rental lift.

At the same time, we had a second tenant vacate from a challenging office portion of space adjacent to this, leaving us with a total of 68,000 square feet vacant. We’re currently in the final negotiations with a new tenant for the full 68,000 square feet with significant rental lift for occupancy expected to be in August.

It is a testament to the strength of our portfolio that when our tenants looked upsize, they looked to do so with us. Similarly, I’m impressed at how quickly and profitably we have been able to backfill the space

Source: Nexus Q1-2024 Conference Call Transcript.

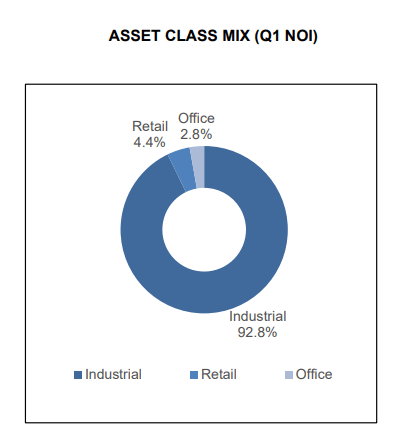

The REIT estimates that the current rent on the portfolio is still 24% below market rents. This is an easy one to get behind as the bulk of the net operating income (NOI) is from industrial and a pittance comes from office.

Q1-2024 MD&A

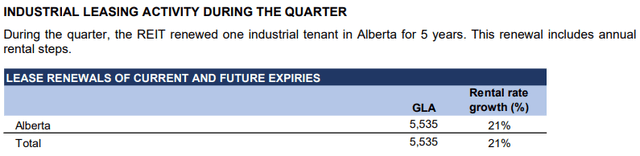

The significant leasing activity on the renewal front during the quarter showed something similar as well.

Q1-2024 MD&A

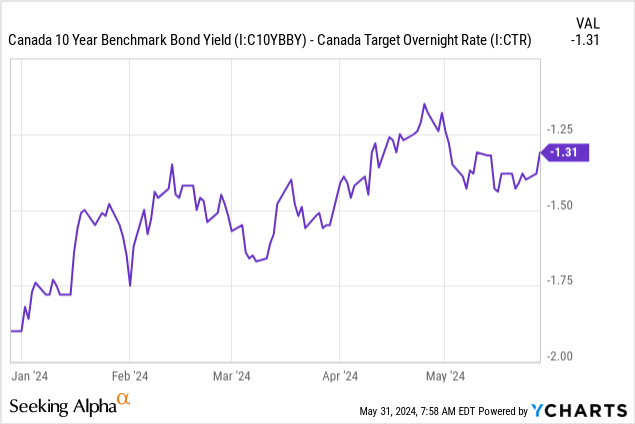

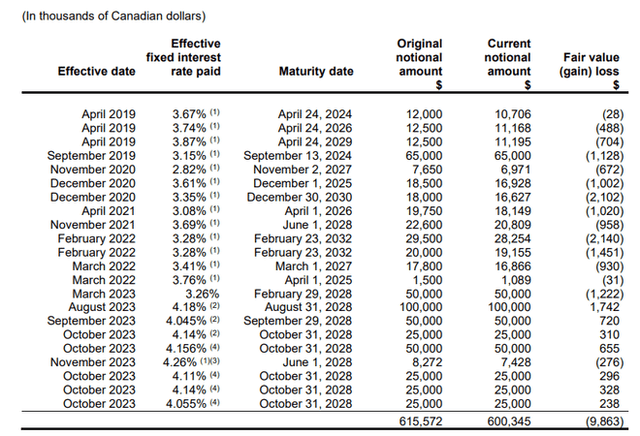

The REIT entered into additional interest rate swaps in the quarter that took advantage of the inverted yield curve. This should reduce its borrowing costs by about 1.6% on $100 million of borrowing. This was good timing, as the Canadian yield curve is now less inverted as rate cuts get priced out.

By fixing this in Q1-2024, Nexus “locked in” those rate cut expectations, even if they won’t happen. The REIT bought one industrial property for $35 million in Alberta during the quarter. It also stated that it plans to sell about $200 million of properties in the back half of 2024.

Outlook

If you are hanging near the 100% payout ratio, you tend to worry about negative surprises. You did get one (negative surprise) this quarter and the payout ratio looks extremely uncomfortable. Management believes the payout ratio has peaked. We generally discard every promise of dividend continuity that comes from management. That is not specific to Nexus. We have this view about every single company. This disdain is amplified in REITs where equity issuance is their lifeblood and prematurely telegraphing a dividend cut is generally a bad policy choice.

In this case, looking at the facts, we believe the payout ratio has peaked. That does not necessarily mean the dividend is safe.

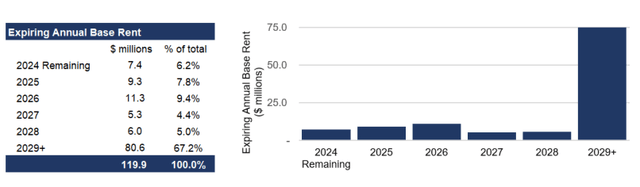

The AFFO payout ratio will fall below 100% only in 2025, and a lot can happen between now and then. The good news for Nexus is that it has other forms of buffer to tide it over the high payout ratio. Its expiring base rents are extremely modest and cumulatively well below market rents. So, the odds are high that it can afford the payout ratio until the underlying earnings power catches up.

Q1-2024 MD&A

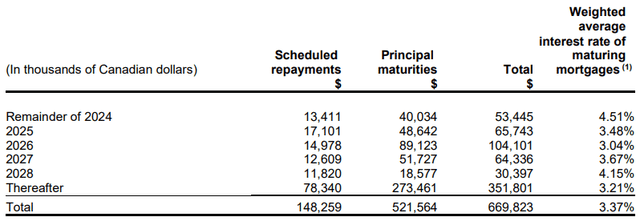

Its debt maturities also look extremely manageable, with just $110 million to be refinanced by the end of 2025. That is half the property sales it plans to make in 2024.

Q1-2024 MD&A

Nexus has a lot of its interest exposure hedged as well. Some hedges run right until October 2028.

Q1-2024 MD&A

In other words, every other base is well covered and the odds of the dividend staying unscathed are high. This was the REIT that maintained it through COVID-19 as well, and management may want to preserve that record if it aims to make it really big. So, at present, we give this low odds of a cut.

Verdict

The key reason to own this has nothing to do with whether it pays 64 cents or 46 cents in 2025. If those 18 cents make the difference to your investing decision, you have come to the wrong Seeking Alpha article. The dividend is important to the extent it conveys a message about the health of the company. We believe that the underlying properties are worth well exceeding the enterprise value and the implied cap rate of well over 7%, is unfair considering the portfolio quality. That said, there is a reason we sold this REIT near $12 in 2021 (it traded at 1.2X NAV) and did not issue a buy rating until it was under $7.50. You need a big margin of safety when the payout ratio is high and the REIT is relatively small. At present, we have it.

We did not see anything from Nexus Industrial REIT this quarter to change our view on the bullish front. We maintain our “buy under $7.50.”

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here