Shares of Sonoco Products (NYSE:SON) have been a poor performer over the past year, losing 2% of their value even as the broader market has rallied given excess inventory and weak pricing. However, shares have performed better of late, aided by a solid Q1 earnings report. I last covered SON in December, rating shares a “buy,” and since then, they have rallied and been a market performer, returning 12.7% vs the market’s 12.3% gains. Shares do remain substantially below my $72 target, and with new financials, now is an opportune time to determine if SON can rally further and outperform the market. Given the negative surprises in the business, investors should be glad about market-like returns and reduce positions.

Seeking Alpha

In the company’s first quarter reported on April 30th, Sonoco earned $1.12 in adjusted EPS, beating consensus by a nickel, as revenue fell by 5% to $1.6 billion. Relative to my initial expectations for the year, Sonoco has been underperforming. Sonoco had a 14.9% EBITDA Margin, down 110bps from last year. Given the company began implementing price increases in late 2023 across its paper portfolio, I was expecting the company to deliver wider margins, but these increases are not yet delivering results for shareholders, in part because non-paper pricing is weak. With thinner margins and weaker volumes, Sonoco generated $245 million in EBITDA from $276 million last year.

In fact, prices were down from last year, and as a consequence the differential in price/cost was a $67 million headwind whereas I was expecting it to be closer to neutral. Even in paper where it has implemented price increases, price/cost has been a headwind. This came even as North American and European paper demand has been recovering, which should provide pricing power. While Sonoco has raised prices, it is seeing input prices rise faster.

SON is blaming this margin tightening on timing, and it believes that price increases will help to catch up with higher input costs, and as a consequence, it expects EBITDA margins to expand across the year. However, the magnitude and timing of this recovery is very much an open question, and the lack of progress on this front in Q1 is concerning. Ongoing wage inflation, which has weighed on paper margins, may continue to pressure results as well, as paper mill staffing has been difficult in a fairly tight labor market.

Drilling into results further, in its consumer unit, sales fell 5% to $911 million, but EBITDA was flat at $129 million. Snacks and confectionery volume were weak, driving the weakness. It does expect overall consumer volumes to rise this year. However in Q1, North American consumer volumes were “lower than originally forecast” with Europe “sluggish.” Additionally thus far in Q2, North American consumer volumes “remain challenged.” These downside misses, and ongoing weakness, call into question whether volumes will rise as much as Sonoco expects. While the company has been blaming the macro environment, I am not certain there are not idiosyncratic headwinds as well.

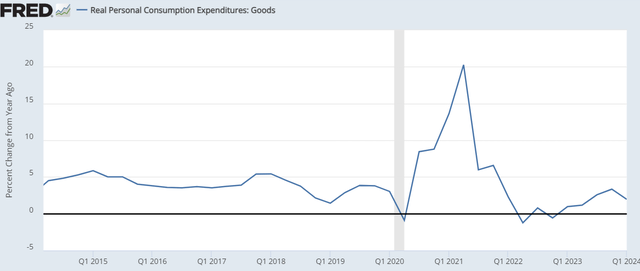

Packaging volumes are generally correlated with how many things consumers are buying; more items bought means more demand for the packaging of those items. Real goods consumptions has turned back positive after dipping 2022-2023. At ~2%, growth is not particularly fast, but volumes are increasing. This is an environment where Sonoco should be reporting stable, if not growing, volumes.

St. Louis Federal Reserve

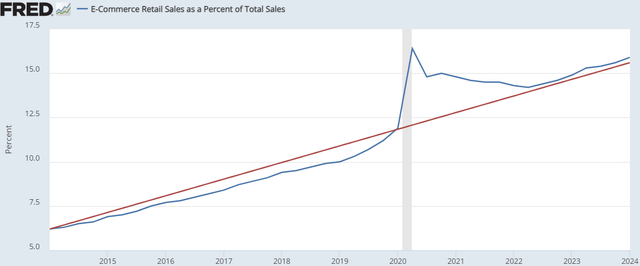

Moreover, one source of volatility since COVID has been shifts in e-commerce consumption patterns. During the pandemic, there was a massive shift towards online retail when physical stores were closed, and then this reversed as the economy reopened. Online orders require more cardboard and packaging to ship goods, and many retailers over-ordered cardboard to ensure they had adequate packaging. As online consumption slowed, they then worked off this excess inventory, reducing Sonoco’s sales. However, Sonoco has said customer inventories have improved, and as you can see, online penetration is rising again and broadly in-line with the pre-COVID trend. In Q1, e-commerce penetration rose from 15.6% to 15.9% sequentially. This volatility and headwind should be behind results and actually be a modest tailwind, yet it is not really showing up in volumes.

St. Louis Federal Reserve

While consumer volumes were down, industrial volumes were broadly stable with North America outperforming and Latin America underperforming, though pricing remains a headwind. Sales fell 4% to $593 million while EBITDA fell 21% to $95 million, given margin pressure. Over time, Sonoco aims to shift its focus to 75% consumer and 25% industrial, via organic growth and divestitures. Along these lines, it sold its Protective Solutions unit for $80 million.

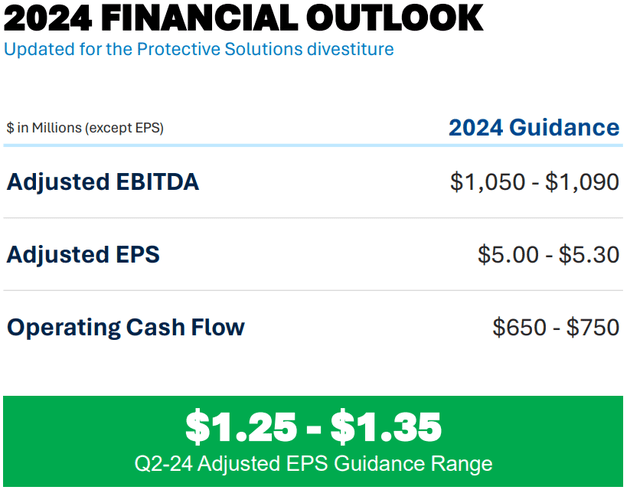

In the quarter, Sonoco generated $166 million in operating cash flow, up from $98 million last year. This translated to $80 million of free cash flow. For the full year, as you can see below, the company expects to generate $650-750 million in operating cash flow. Given it plans to spend $350 million of cap-ex, that should lead to $300-$400 million of free cash flow and about $5-5.30 in EPS.

Sonoco Products

For 2024, I was looking for 5% pricing gains and 3% volume growth, which I believed could lead to $625 million in run-rate free cash flow. At a 9% free cash flow yield, this is how I arrived at a $72 fair value. However, it looks like pricing and volume could both run closer to flat, which is why free cash flow is substantially lower than I expected. Now, its 3.5% dividend costs $200 million, so free cash flow does safely cover its payout.

The company targets 2-3x debt to EBITDA leverage, and with $3.1 billion in debt and $172 million in cash, leverage should stay just below the 3x area. Proceeds from asset sales that go to reduce debt can also bring leverage below 2.5x over the next year. Its debt has a 6.9 year average maturity, reducing interest rate sensitivity.

Given the fact consumption is rising, we should see some modest improvement in volumes, though I remain concerned Sonoco’s volume growth underperforms the economy, and announced price hikes should also provide some support, so I do expect to see incremental EBITDA growth from the $980 million Q1 run-rate. Assuming about 1% sequential growth, SON should generate about $1.03-1.06 billion in EBITDA, so I see risks skewed toward it delivering the low-end of guidance rather than high end.

At $300 million in free cash flow, SON has a 5.6% free cash flow yield, much below the 9% yield based on my estimates. I significantly overestimated Sonoco’s ability to raise prices, and its volume underperformance has been disquieting. Its commentary on volumes also leaves me concerned about its guidance, and I see results migrating toward the low-end. Considering weakness in the business, I view its market-like return this year as pleasantly surprising. My buy rating was driven by an overly bullish view of the business. At 12x earnings, I view Sonoco as fair value, given its commodity business and mixed execution, and we need to see better results before investors can believe in a long-term growth story. Macro conditions should keep results from deteriorating, so I do not view a “sell” rating as justified but am moving to “hold.” Shares are likely to continue being a market performer, and I would allocate towards companies more clearly delivering against expectations.

Read the full article here