Investment Thesis

Axcelis Technologies (NASDAQ:ACLS) was one of the first companies I covered on Seeking Alpha. At the time, it looked expensive, and expectations were very high. Since then, the stock price has declined significantly, and I thought it would be a good time to provide a follow-up.

As you’ll read in this analysis, although the company’s products remain vital for semiconductor manufacturers, Axcelis failed to maintain its growth momentum. This is due to several factors, including weak demand for consumer electronics and EVs, as well as the company’s limited exposure to AI. There are still long-term opportunities to generate more earnings, but they appear further in the future.

This lost growth momentum, combined with the limited safety margin, prompted me to maintain my “Hold” rating on the company. In this article, I will briefly go over the business description, recent developments, outlook for the near future, and valuation.

Business Description

Although I have previously discussed how the company earns money in my previous articles about Axcelis, I will briefly go over it once again. For a more detailed description, please refer to my older articles.

Axcelis Technologies plays a crucial role in the semiconductor industry. Semiconductor chips are used in various electronic products from personal computers and mobile phones to automobiles and sensors. Demand for these products can have different drivers, with some being exposed to consumers more while others power the artificial intelligence surge we are experiencing right now.

While companies like Nvidia (NVDA) can design and engineer these chips, the actual manufacturing process is complex and requires substantial investments. That is why there are pure-play semiconductor manufacturers. These are called foundries. Axcelis provides ion implementation and other processing equipment to these manufacturers. I will not get into the technical details, but this equipment helps modify a semiconductor’s electrical properties, which is a crucial process.

This is a very complex technology that requires years of research and know-how. That is why there are only a handful of big players in this industry, including Axcelis and Applied Materials (AMAT).

Recent Developments and Stock Performance

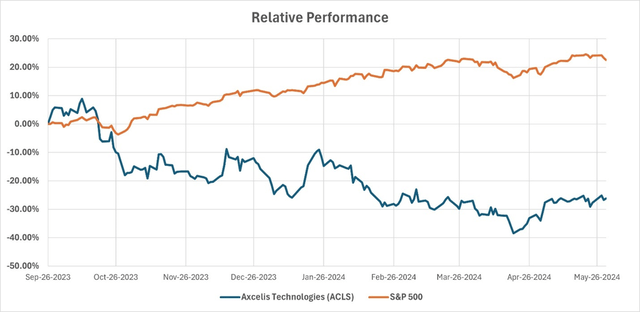

Since my initial analysis here on Seeking Alpha, the stock has been going downhill. It has massively underperformed the S&P 500 index, as shown below.

S&P Capital IQ

There are several reasons for this, which we will explore in the outlook section. To summarize, growth opportunities have not materialized, and the company has been left out of the AI ecosystem.

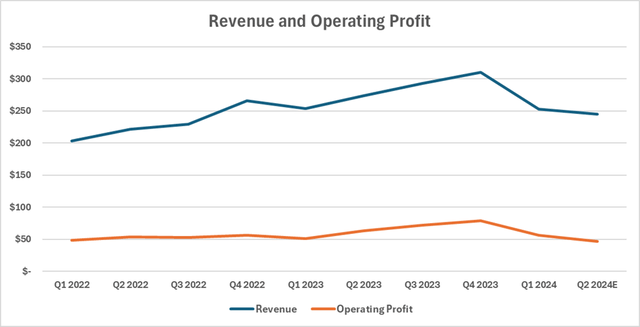

In the most recent quarter (Q1), the company beat EPS and revenue estimates. Revenue was slightly down compared to the same period last year. Management guided for lower revenue and operating profit in Q2 compared to the same quarter last year. Below is a chart showing Axcelis’ quarterly actual and expected revenue and operating income.

S&P Capital IQ

It’s clear growth is not meeting market expectations from the stock chart. Revenue and operating profit were flat year-over-year in Q1, and are expected to decline next quarter. This is one of the reasons for the stock’s decline. In the next section, we will discuss why the company is experiencing stagnant growth.

Outlook For The Near Future

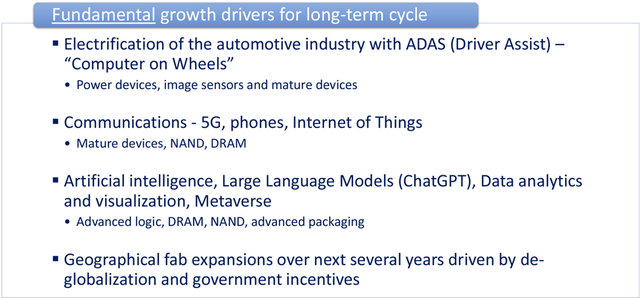

The earnings presentation from May 2024 highlights key fundamental growth drivers, which you can find below.

May 2024 Investor Presentation

I believe these have the potential to be huge drivers of earnings for the business. However, the key word here is long-term. Remember, the further out the earnings are projected, the higher the discount rate the market applies (or should apply). While I am confident in the firm’s ability to convert these growth drivers into actual earnings, I am skeptical about the timing.

Let’s break down each of the bullet points above one by one.

Electrification is transforming everything, from household items to how we drive. I recognize the business opportunity with EVs and other technological advancements in cars such as driver assistance systems. However, I believe one should also recognize the current state of the innovators in the automotive industry. The technology pioneer Tesla is losing market share to its Chinese competitors, while more traditional players revert to internal combustion engines or hybrid, postponing or canceling their EV projects. Additionally, car sales remain below pre-pandemic levels and are projected to decline as consumers weaken due to sustained high interest rates and inflation. Combined with regulatory hurdles, it seems Axcelis has a long way to go before seeing significant improvements in this area.

Communications is an intriguing field for investments. The potential of a fully implemented Internet of Things is mind-blowing. We are upgrading our phones, and 5G is becoming increasingly available. The US government has been trying to incentivize communications companies to invest more and improve the country’s infrastructure. However, this has not materialized so far. High interest rates have constrained this investment. There is a chance investment will resume once the Fed starts cutting rates, but that also doesn’t seem to be happening soon. As the FedWatch Tool shows, 46.5% of the market thinks rates will be down to only 500-525 bps in November 2024.

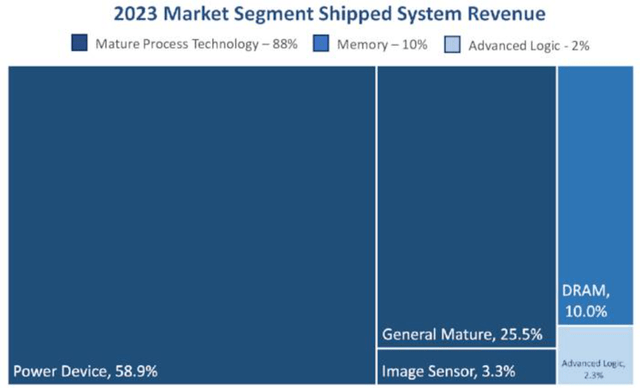

Artificial intelligence has been undoubtedly the story of 2024 so far. We have seen improvements we thought were not possible. Essentially, these are language models trained on immense data, and they continue gathering more and more data. That means we need more semiconductor chips for data storage. My concern is twofold. First, I worry that most of the infrastructure investments for AI have already been made. Once sufficient infrastructure is in place, it will be the AI technology and machine learning models that make the difference, as the infrastructure will already exist. Decreasing investment in AI infrastructure would mean reduced investment in semiconductor manufacturing capacity, and therefore in Axcelis’ products. My second concern is even if this continues to be a high-growth area, Axcelis doesn’t participate in it that much. The chart below shows the market segmentation of the company’s shipped system revenue. Memory chips and advanced logic account for only 12% of sales. The company is primarily exposed to power devices and general mature products, which are used in consumer electronics and vehicles.

May 2024 Investor Presentation

Lastly, it is true that there are planned fab expansions in upcoming years. One of these examples is Intel (INTC), which is trying to become the foundry of the Western Hemisphere. As they will need semiconductor equipment, it would mean higher demand for Axcelis’ products. However, I remain skeptical about the timing of these additional earnings. It will take considerable time for Intel and others to build operational fabs and place orders. Intel’s target to become the #2 foundry is only for 2030.

Overall, I think long-term drivers are strong. That is why (combined with the valuation that I’ll get into) this is not a short thesis. However, I think these are too long-term and should be discounted accordingly.

Valuation

Let’s get into the valuation part and see what the fair value looks like for this company.

My target price in my initial short thesis was $107. In the follow-up article, I maintained that target but closed the short position with a hold thesis as the macro environment seemed to be improving. The stock actually fell below that target price, and now slightly recovered to $113 at the time of this article’s writing. The target price has only slightly changed since the last analysis.

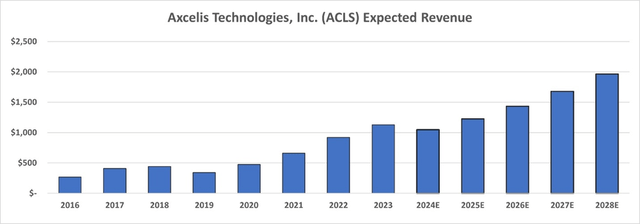

This is a positive scenario, where I assume that the company will manage to maintain its post-pandemic revenue growth with the exception of 2024, as management is guiding for lower revenue. This results in a revenue of slightly above $1 billion in 2024 and nearly $2 billion in 2028. See below:

S&P Capital IQ & Author

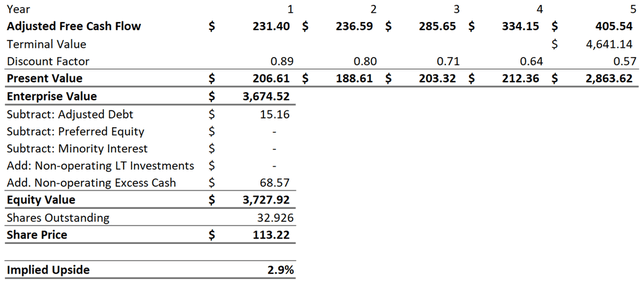

With my margin, capital expenditure, and net working capital change expectations, this revenue translates to an adjusted free cash flow of $231 million in 2024 and $405 million in 2028.

As a reminder, I separate cash and short-term investments into operating and excess in my calculations. I use a certain percentage of revenue, typically between 5-10% to calculate operating cash. This is meant to be a ballpark calculation for the amount that is going to be spent on the day-to-day operations of the company for a year. The rest is excess cash. This excess cash can be claimed by the shareholders, but not the operating one, as the business needs it.

Using these numbers and methods, we find an equity value of $3.72 billion, which means a target share price of $113.22. This is a 2.9% upside over the current share price at the time of this article’s writing and does not provide enough margin of safety to make this a buy.

Author

Conclusion

Axcelis Technologies plays a significant role in the entire semiconductor supply chain. I believe it has solid long-term tailwinds that will help it boost its top and bottom line. However, the timing of these expected earnings is uncertain.

The four main areas of long-term growth highlighted by management are all facing problems. These challenges either stem from high interest rates, which create an unattractive investment environment or from demand issues in consumer electronics and EVs. Additionally, the company does not benefit massively from the need for more data thanks to the developments in AI, as it only has a small exposure to that industry.

Although the company is now a lot cheaper compared to when I first analyzed it and the implied upside is positive, there is neither a good margin of safety nor a compelling short-term catalyst for the stock to achieve higher valuations.

That is why I maintain my “Hold” rating on Axcelis. I will keep tracking this company and publish another analysis if the thesis is no longer valid.

Read the full article here