The U.S. faces an ongoing housing shortage, with no clear end in sight. One beneficiary of this tailwind is UMH Properties, Inc. (NYSE:UMH), a leading manufacturer and distributor of manufactured homes.

“Demand for affordable housing in our markets and across the country remain incredibly strong. Our communities continue to fill sites with homes for rent and sale.

Our improvements have transformed depressed communities into first-class communities, creating waiting lists for our homes. This business plan has allowed us to profitably increase the supply of quality affordable housing in the markets we serve. Within the next five years, our community should be full and there will be limited lots available to place homes on. The housing crisis and the inability for conventional builders to deliver housing at an affordable price point highlight the tailwinds behind UMH in our industry.” (Q1 ’24 earnings call.)

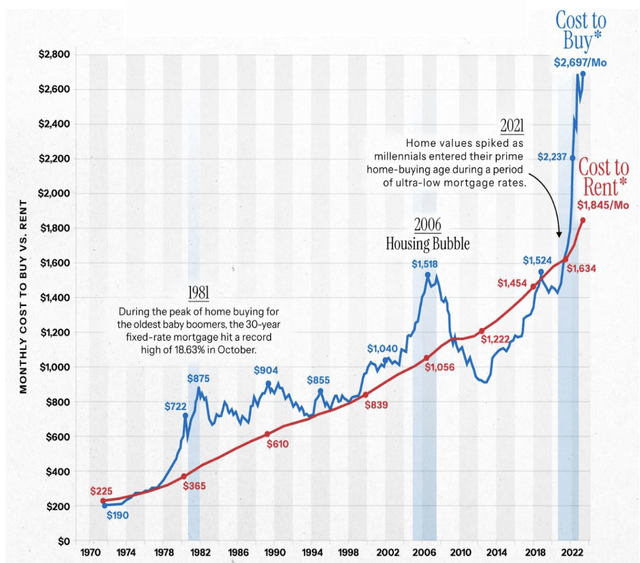

The shortage has driven up the cost to buy and the cost to rent in the past decade:

UMH Site

Performance:

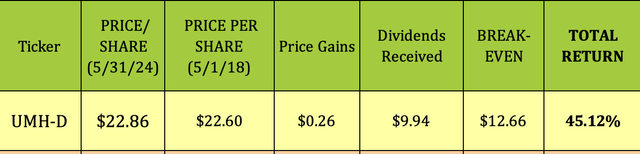

We added the UMH Properties, 6.375% Series D Cumulative Redeemable Preferred Stock (NYSE:UMH.PR.D) to the HDS+ portfolio on 5/1/18. Since then, it has delivered a solid ~45% total return, comprised mostly from its quarterly dividends:

Hidden Dividend Stocks Plus

Company Profile:

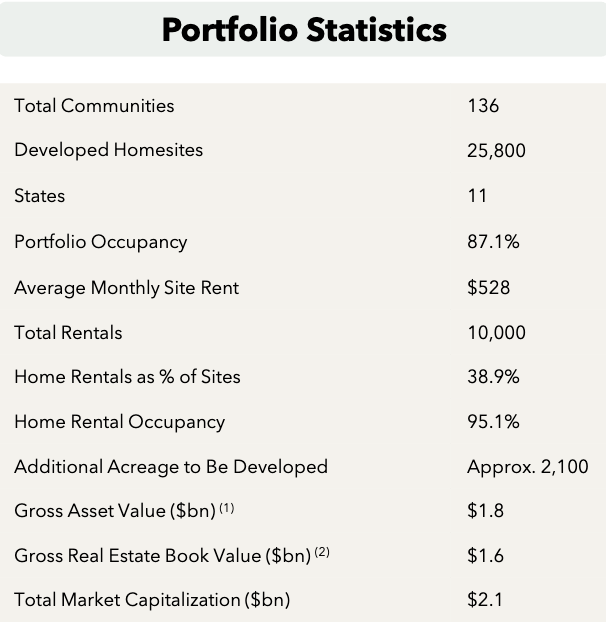

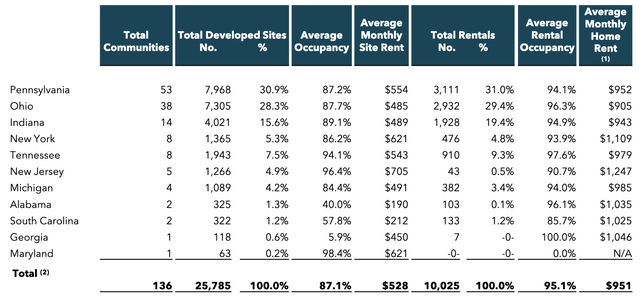

UMH Properties, Inc. is a public equity REIT (real estate investment trust) headquartered in Freehold, NJ. The Company owns and operates a portfolio of 136 manufactured home communities with 25,800 developed home sites.

In 2023, occupancy averaged ~87%, with home rental occupancy at ~95%, representing 39% of sites.

UMH Site

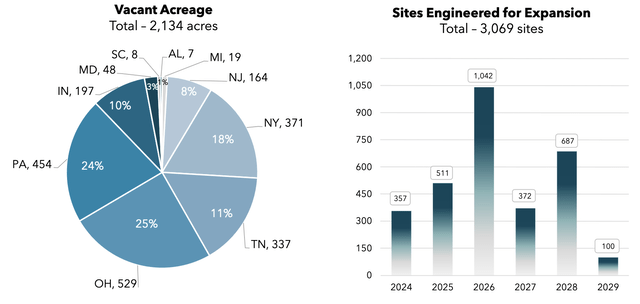

UMH also has room for expansion, with ~2100 acres for development. It generally can put 4 homes on an acre, at a cost of ~$75K/home.

UMH Site

PA and Ohio are its biggest areas, with 31% and 28% of its developed sites, followed by Indiana, at 15.6%, Tennessee, at 7.5%, and NY, at 5.3%. It also has sites in 6 other states. NJ has the highest average monthly rent, at $1,247, followed by NY, at $1,109.

One of the interesting side notes about UMH’s portfolio is that it’s concentrated in the Marcellus and Utica Shale Regions, which are large natural gas fields located beneath much of Pennsylvania, Ohio, West Virginia, and New York. UMH has 78 communities, and 12,300 sites in this area.

UMH Site

UMH’s Sales & Finance unit, which does both of these functions, has sold 5700 homes since 1996. Its portfolio of ~1600 homes is spread across 109 communities. It has an $80.5M loan portfolio, which generates ~$11M in principal and interest annually. Most loans require a 10% down payment, with 15-25 year amortization.

Earnings:

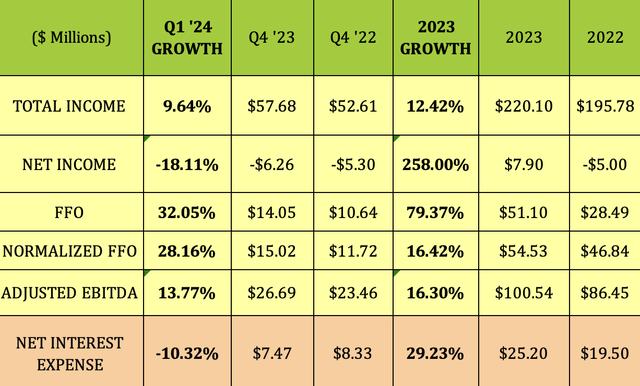

Q1 ’24: Normalized FFO, which excludes amortization and non-recurring items, was $15 million, vs. $11.7 million in Q1 2023, up 28%. Total Income rose 9.6%, primarily due to an increase in same property occupancy, the addition of rental homes, and an increase in rental rates. EBITDA rose 13.77%.

Net Income was -$6.26M, down 18%, due mainly to a ~$2M rise in non-cash markdowns of marketable securities. Net interest expense actually decreased 10% in Q1 ’24.

2023: It was a good year for UMH, with income up over 12%, and Net Income swinging from a -$5M loss to a $7.9M gain. FFO surged 79%, while Normalized FFO rose 16.4%. EBITDA rose ~16%. Net interest expense rose to $5.7M, up 29%.

Hidden Dividend Stocks Plus

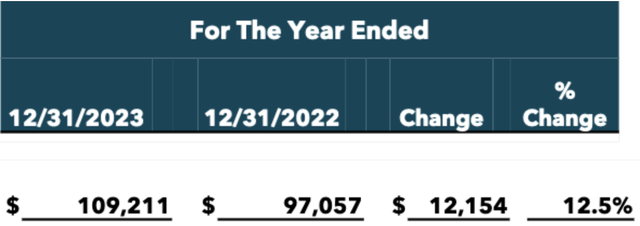

A key Real Estate figure, Same Property Net Operating Income, NOI, rose 12.5% in 2023, hitting $109.2M:

UMH Site

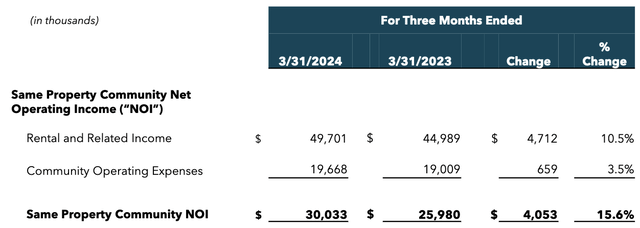

In Q1 ’24, NOI rose 15.6%, continuing that rising trend:

UMH Site

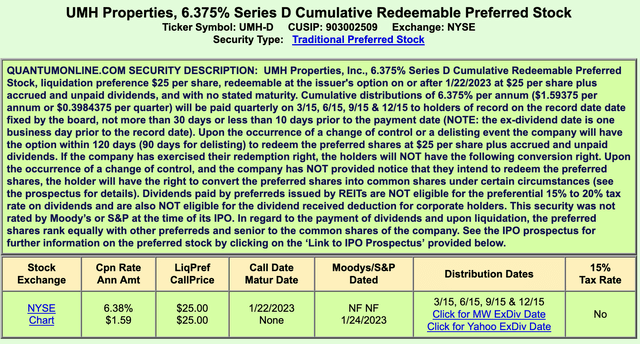

Preferred Dividends:

These are cumulative shares, meaning that UMH must pay preferred shareholders any skipped dividends BEFORE paying common shareholders. They’re also senior to UMH’s common shares in a liquidation event.

Quantum Online

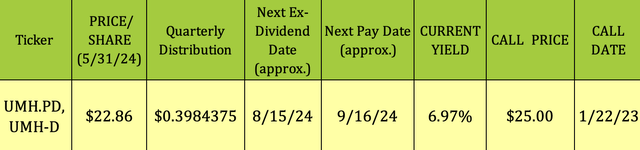

UMH-D goes ex-dividend in a Feb./May/Aug./Nov. schedule – it should go ex-dividend next on ~8/15/24, with a ~9/16/24 pay date.

At $22.75, the current yield is ~7%:

Hidden Dividend Stocks Plus

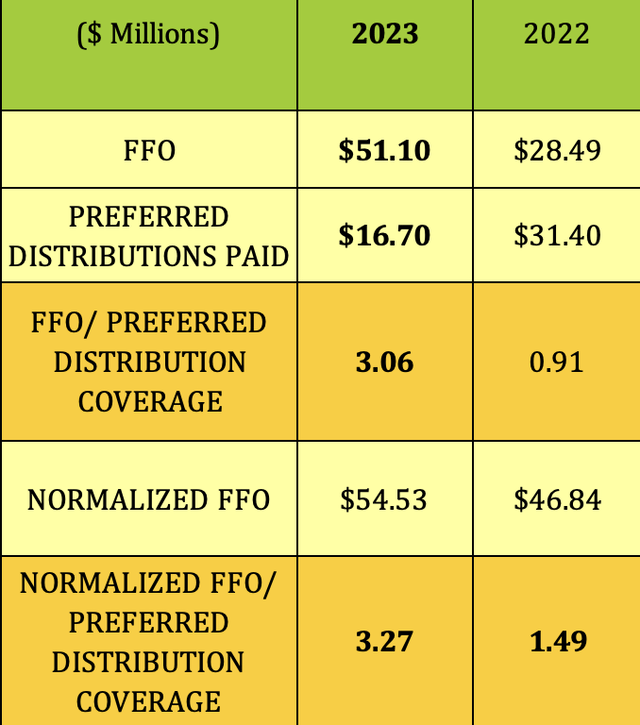

UMH’s preferred coverage improved a great deal in 2023, with FFO/Preferred Dividend coverage jumping over 3X, to 3.06X, while Normalized FFO coverage increased from 1.49X in 2022 to 3.27X in 2023:

Hidden Dividend Stocks Plus

Potential Redemption:

With 11,801 million UMH-D shares outstanding as of 3/31/24, it would cost UMH ~$295M to redeem these shares. UMH’s current debt cost is 6.79%, which is higher than the 6.375% rate on these shares, so we don’t expect them to redeem these shares until interest rates come down much more.

Taxes:

These are nonqualified dividends.

Profitability & Leverage:

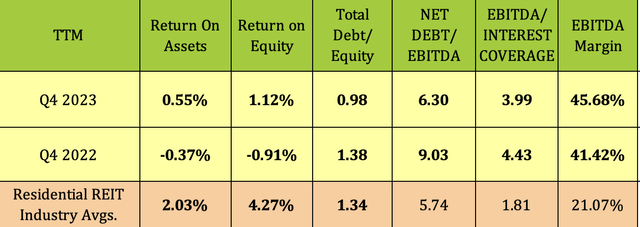

ROA and ROE both improved in 2023, although they remained below industry averages, whereas UMH’s EBITDA Margin is much higher than average for its industry.

UMH’s debt leverage improved a lot in 2023. It has somewhat higher Net Debt/EBITDA leverage, of 6.3X, vs. the 5.74X industry average, whereas its Total Debt/Equity ratio improved to .98X as of 12/31/23, vs. 1.34X for the industry avg.

As with most other companies, UMH’s interest coverage decreased a bit because of rising rates, but still remained much stronger than average:

Hidden Dividend Stocks Plus

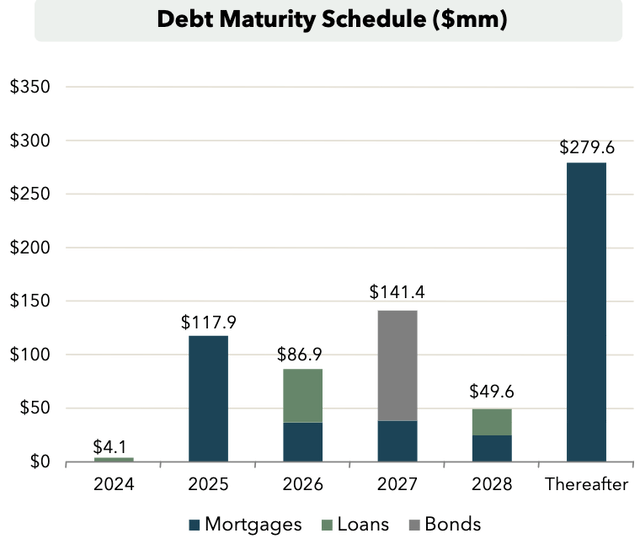

Debt & Liquidity:

UMH ended Q1 ’24 with $39.9 million in cash and cash equivalents and $130 million available on its unsecured revolving credit facility, with an additional $400 million potentially available pursuant to an accordion feature. It also had $194 million available on our other lines of credit for the financing of home sales and the purchase of inventory and rental homes.

In April 2024, management expanded the borrowing capacity of UMH’s unsecured revolving credit facility from $180 million in available borrowings to $260 million in available borrowings.

Total debt was 92% fixed rate at quarter end, with a weighted average interest rate on short-term borrowings of 6.79% at 3/31/24.

UMH has minimal debt due in 2024, with ~118M due in 2025.

Hidden Dividend Stocks Plus

UMH issued and sold 194,000 shares of its Series D preferred stock during the first quarter of 2024 through the preferred ATM program, generating net proceeds of approximately $4.4 million.

Parting Thoughts:

We rate UMH-D a Buy, up to $25.00, based upon the improving dividend coverage, and UMH’s solid position in the manufactured housing industry. We see UMH riding this secular trend for years to come.

Read the full article here