Dear Readers/followers,

You may recall my coverage of the company SpartanNash (NASDAQ:SPTN) a year ago or so. A reader recently inquired as to whether I had sold my stake in the business given the relatively negative trend we’ve seen. My answer to that question was a simple but firm “no”.

In this article, I’ll reveal to you why I don’t believe that the company is worth as little as the market is currently pricing it at, why I believe there to be significant upside here, and why any valuation below a 10x P/E, which by the way is where we are today, is at a point where I would say that the company can be bought with a significant upside.

SpartanNash is small. At the current level, it manages no more than a sub-$700M market cap, which makes this one of the smaller US-based stocks in this category that I cover. At 50% long-term debt to capital, it also isn’t terribly low leverage, which is otherwise a fairly general and fairly common thread for these businesses.

But the upside given the company’s operations, is still there.

Let’s see what we have here and provide an update on this company.

SpartanNash – The upside is still there, despite everything

A fair question may be that considering the company’s unflattering trend since my last article, which you can find here, if the upside I spoke of at the time is gone here – to which I would say that no, it isn’t.

As I’ve mentioned in the pieces before, any investment into qualitative food production, logistics, or food-adjacent services that you make is not a net negative in my book. These are segments that, just like utilities and similar segments, hold significant upside over time even if we are currently in an environment where such companies are being valued lower and lower, due to increasing risk-free rates, increased cost of debt, and overall inflation and cost increases. That being said, we do need to be aware of the risks, and SpartanNash isn’t risk-free.

As I have, and the company has mentioned before, this is a business in the midst of a transformative change. Net margins did collapse, and and the company had a lot of work to do. The high leverage, relatively, means that the interest coverage is sub-par for the sector, and there’s not a whole lot of cash on hand – 0.02x cash to debt as of my last article.

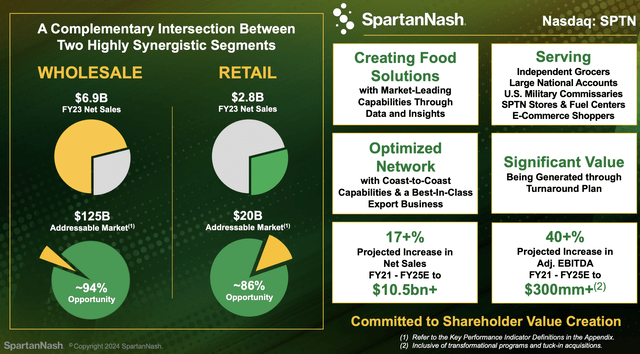

However, SpartanNash remains a solid play on two highly synergistic sectors – retail and whole sale – with a significant sales number, as well as a high TAM. Yu know, if you follow my work, that I don’t consider TAM more than slightly relevant to any business – but sales here is impressive. Also, the company is forecasting some fairly significant sales and EBITDA growth numbers – and unlike with other, riskier businesses, I do not see these as unrealistic.

SpartanNash IR (SpartanNash IR)

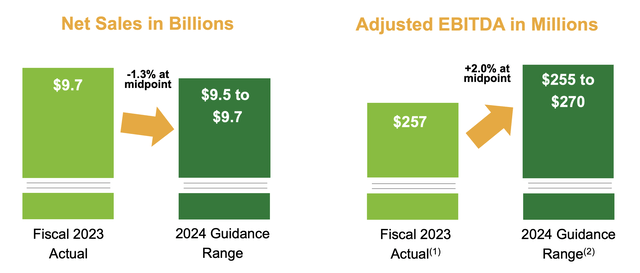

The upside in earnings and performance is further confirmed by quarterly sales of over $2.8B, positive net earnings increasing by 14.4% YoY, and a stable EBITDA – somewhat down, but only 2.4% during the company’s transformation. There’s a slight improvement in Net margin (really more of a rounding error, don’t boast of a 7 bps improvement when you’re a sub-$1B company), and the current guidance for the full year looks something like this.

SpartanNash IR (SpartanNash IR)

This is kind of what I like to see – not the lower sales, but the EBITDA improvement potential. It means the company is profit-focused rather than top-line-focused – far too many companies are still too laser-focused on that top line – including a food-related company I recently wrote about, HelloFresh SE.

it’s not that I consider the top line irrelevant, it’s just not that relevant when the top line is all you have and you’re profit-negative. For far too long, investors have accepted the argument that “with enough volume, there’ll be profit”.

If you don’t have profit with over a $1B top line, chances are you’ll never get there.

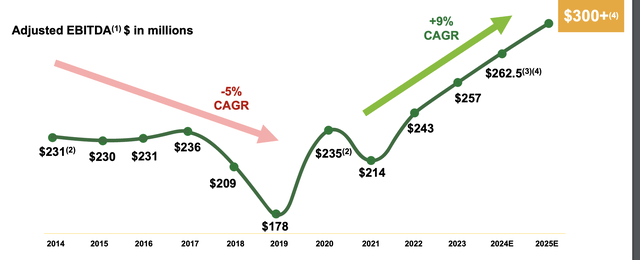

Meanwhile, SpartanNash’s turnaround is driving the company in the right direction. From troughing during COVID-19 – understandably, given the company’s sectors and segments – we’re now driving towards that $300M in EBITDA.

SpartanNash IR (SpartanNash IR)

And that is with some fairly significant headwinds that SpartanNash has faced during this turnaround, including labor costs, logistical costs, food inflation, market demand volatility, and the like. However, the company is still delivering on its strategic commitments.

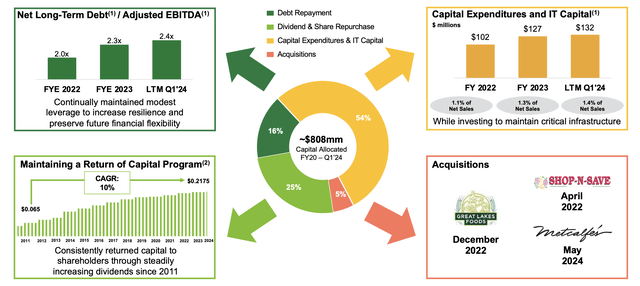

The company’s approach to its capital allocation at this time remains very conservative. CapEx and IT to sales is around 1-2% – that’s it at this time, given the company’s state. However, not much is going into debt repayment. The company views the 2.4x net debt/EBITDA as good enough. I don’t agree, but this is something that can be discussed. Far more, 25% of capital, is actually going to shareholder returns – only eclipsed by CapEx. A very small part is going towards M&A.

SpartanNash IR (SpartanNash IR)

To be completely frank with you, nothing much has changed since my last article in how I view the company and its long-term potential. It could be said that the company has not yet materialized the upside that some expected or hoped for, but the fact is that I never expected them to manage this at such a fast rate.

My arguments for SpartanNash continue to be centered around the core operations, complemented by a very strong number of company-specific key advantages, including the military segment. SPTN continues to maintain its military segment, distributing dry groceries, frozen foods, beverages, and meats to U.S. military commissaries and exchanges. This is somewhat unique, as the company, with the third-party partner Coastal Pacific Food Distributors, is the only delivery solution to service the Defense Commissary Agency to this degree in the entire world.

This won’t make this one a “BUY” alone, but complemented with the turnaround I see happening under the hood here, it’s enough to both keep me invested at a well-covered yield of over 4.4%, and even potentially invest more.

Let me clarify my valuation for the business at this state.

SpartanNash – The valuation is attractive with a PT of $30/share or above.

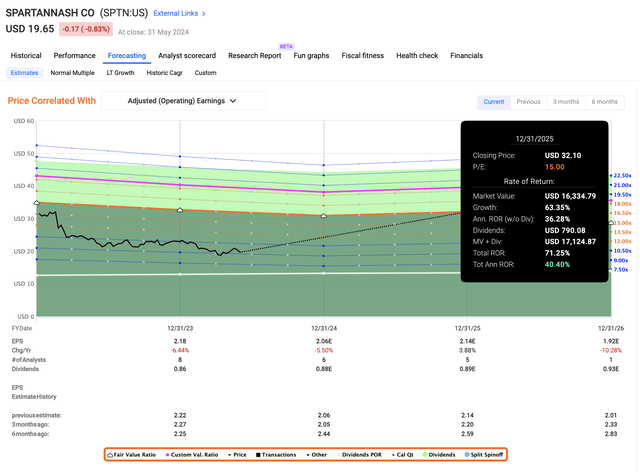

In my last article, I gave the company a PT of around $30/share. The current forecast is for the EPS to continue to decline marginally, and there is one analyst forecasting a double-digit EPS decline trend in 2026 – which I have not been able to find any rationale for outside of that target alone – so at this point, I don’t give it much credence.

I’d also like to point out that SpartanNash most often either manages or sometimes beats its estimates – over 75% of the time. (Paywalled F.A.S.T graphs link). Only around 20% does it actually miss negatively with an MoE of around 20% on a two-year basis.

My argument is that a food service company like this with a solid track record, even a small one like this, should conceivably be worth at least a 12-15x P/E multiple – especially if they manage to turn things around. It’s important to note here that I expect these things to turn around. If you do not believe this to be the case, then this is probably not a good investment for you.

But if you, like me, see that SpartanNash could turn around here, then you could see an upside of up to 40% annually until 2025E based on only a 15x P/E, to a PT of around $32/share. This is above my $30/share, so in my mind, the company does not even need to manage that.

F.A.S.T Graphs SpartanNash Upside (F.A.S.T Graphs SpartanNash Upside)

To my estimate, the company only needs to manage around $28-$29 or a 13-13.5x P/E, which gives us 30% per year at this point. Granted, the low growth estimated at this time and even a decline in this year could cause this company to trade sideways for some time – but that’s where the patience comes in, and this is why the yield is so crucial when I invest. I don’t just want to be paid in capital appreciation, I also want “interest” for my money.

In this case, I’m getting interest at 4.43% at a coverage of well below 60% payout, which to me is good enough to continue to take this risk, in exchange for the upside of market-beating return potential.

As long as I don’t see any deterioration of this thesis, then I’ll continue to invest like this, and in this company. I don’t sell just because a company hasn’t reached its peak – I sell because a thesis breaks.

SpartanNash’s thesis has not broken.

What we have here is a company that due to macro, inflation, and an ongoing, turnaround is being penalized on the market. Penalizing such a company is completely valid. To this degree, I would consider that perhaps a bit too much.

Risks here continue to be margin deterioration and a failure for the turnaround. Some of the targets and recovery have been “Pushed out” in terms of timing – but I do not equate this to the upside or the turnaround never coming.

At this point, many investors are seeking shelter in high-valued tech stocks. I do the exact opposite. I try to find the lowest-valued quality plays with a good upside, because anyone “promising” me quadruple digit upside in a short time, and anything that “sounds to good to be true”, likely is. This doesn’t mean I don’t invest in tech – I do, and I do so successfully. But I’m extremely picky with how I invest in it.

At this point, I say SpartanNash is a continued “BUY”, with the following thesis.

Thesis

- The company now has an upside to a PT of $30/share, which was my previous PT as well. The main difference is that we’re now close to $20/share, as opposed to over $30/share as in my last article. Any working company becomes attractive at the right price, and after a 40% drop, it’s time for SpartanNash to become attractive.

- The company is fundamentally appealing – and here, I believe you can actually start buying common shares of SpartanNash, I recently added more shares to my position in the company as well.

- I value SPTN to a $30/share PT, with a “BUY” rating at the current valuation. This marks a rating change for me for the company.

- I’ve looked at the current options market, but did not find anything attractive enough for me to invest in – though I’ll keep looking and updating if a cash-secured put catches my eye.

- As of this article update in June of 2024, I keep my eye on the eventual price and may add to the company going forward.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I consider the company both cheap and has an upside here, and for that reason, I’m holding my thesis at a “Buy” here.

Read the full article here