Investment action

I recommended a buy rating for Burlington Stores (NYSE:BURL) when I wrote about it in late March this year, as I expected, BURL to meet its 5-year target, and in the near term, BURL should easily meet the high end of its guidance. Based on my current outlook and analysis, I recommend a buy rating. My key update to my thesis is that I now have more confidence that BURL can meet its long-term targets of 11% CAGR and 10% EBIT margin. The 1Q24 results were really encouraging, and I believe the momentum can continue for the rest of the year, enabling BURL to beat its FY24 SSS growth guidance.

Review

BURL reported earnings a few days ago. In the report, 1Q24 sales grew 10.5%, beating consensus expectations of 9.6%, to ~$2.4 billion. In terms of same-store sales [SSS], BURL grew it by 2%. In terms of profitability, gross margin came in at 43.5%, in line with consensus. This was an expansion of 120 bps vs. 1Q24, driven mainly by merchandise margin expansion. Down the P&L, EBIT margin saw 5.5%, a 140 vs 1Q23 and 100bps above consensus estimates of 4.5%. Given the strong start to the year, management raised its FY24 EPS guidance, now expecting adj. EPS of $7.35 to $7.75, an upgrade from the previous range of $7 to $7.60. Driving the EPS guide was an expectation of flat to 2% SSS growth for the full year. Nearer-term. The outlook for 2Q24 was adj. EPS of $0.83 to $0.93 and SSSG growth of flat to 2%.

I reiterate my buy rating for BURL, as I believe the upside remains attractive over the medium term. The market has reacted very positively to BURL’s 1Q24 results, showing that they are pricing with more confidence that BURL can hit their targets. I, too, was very encouraged by the 1Q24 results, and I believe the momentum remains strong.

Author’s work

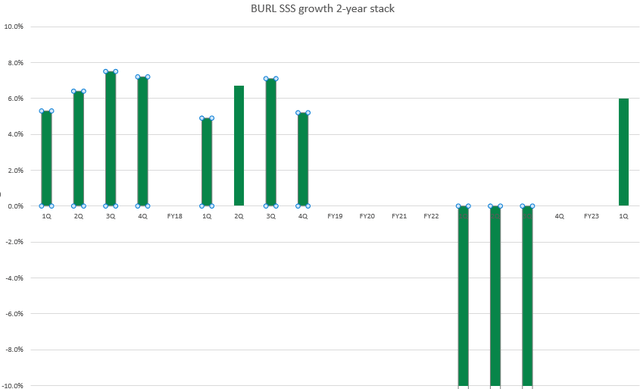

Firstly, while SSS growth was flattish vs. 4Q23 at 2%, SSS growth on a 2-year stack basis accelerated to 6%, which was in line with pre-covid levels, which I saw as clear evidence that BURL continues to benefit from the current macro backdrop. In fact, I believe BURL is doing a lot better than what was reported on an underlying basis, as 1Q24 was heavily impacted by the bad weather in February and also slower tax refunds. The latter has huge impacts on BURL because it impacts the lower-income customer group (as a value/discount retailer, BURL has a large exposure to this group of customers). On a monthly cadence basis, SSS growth exited 1Q24 at 4% (March and April saw 4% SSS growth, according to management). Which means, if not for those headwinds, 2-year stack SSS growth could be nearer to 8% (assuming February is also at similar levels to 4%), which is higher than pre-covid levels.

To be fair, strong management execution skills played a large part in the 4% SSS growth performance in March and April, which is commendable and made me even more bullish on the business ability to meet their FY28 targets. In particular, they deliberately slowed seasonal item sales later in the quarter, which allowed BURL to take advantage of the increased demand for cold weather sales given the slower start to core spring/seasonal sales. Notably, management pointed out that comp sales on clearance merchandise fell by double digits compared to regular pricing products, which saw a 4% SSS rise. Even better, regular selling SSS growth accelerated to 6% in March and April, which, in my opinion, shows great momentum for SSS in the business.

While management has guided for flat to 2% SSS growth in 2Q24, I am more inclined to believe that BURL is going to beat this guidance as management characterized the 2Q24 comp guide as conservative. He even specifically mentioned that they will beat the guide if recent trends hold.

Okay, let me move on to the outlook for the second quarter. Our Comp guidance for Q2 is flat to 2%. We recognize that based on our most recent trend, there could be upside to this forecast. But there are a couple of reasons to remain cautious. 1Q24 call

This is a very interesting comment because this guide was given at the end of May, which means that management effectively has the entire month of May SSS growth data already. For them to be confident enough to say they can beat them based on recent trends, it suggests that May SSS growth is still trending above 2%. Coupled with the fact that SSS growth exited April at 4%, there is a high chance that May SSS growth is still trending at ~3% levels. Using my assumption, in order for BURL to not beat the high end of the guide, June and July have to achieve below 1.5% SSS growth on average. In my opinion, this is unlikely to happen because the current macroeconomic conditions remain uncertain and poor. The latest US inflation data showed no signs of positive change in inflation, and consumer spending power remains pressured. If this goes on, I think it will be increasingly unlikely that the Fed can cut rates as easily as they want. But all these are positive “tailwinds” for BURL as it continues to benefit from consumers looking for value buys. I expect that the current tailwind will persist into 2H24 as well, given my belief that the macro conditions are unlikely to turn for the better in just a few months, and that BURL should see more trade down motions as BURL offers more higher quality brands – according to management, merchants are assorting into higher-quality brands through upfront purchases (i.e., merchants are negotiating with vendors to purchase the products before the season starts) into 2H24.

Author’s work

Based on my analysis, if we assume that this momentum continues for the rest of the year and that BURL continues to achieve 8% 2-year stack SSS growth, it implies FY24 will achieve 4% SSS growth, and that is a 2% beat vs. management FY24 guidance.

Valuation

Author’s work

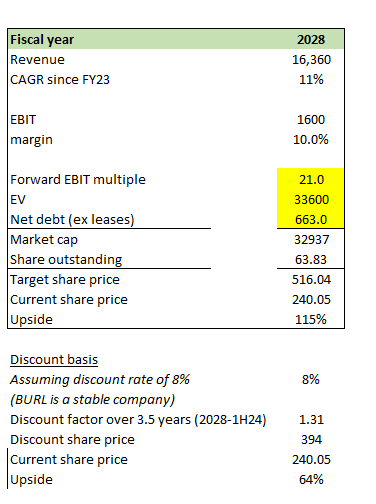

I have written about my model mechanics (BURL to achieve a 5-year outlook) previously, and in this post, I would like to just get readers to focus on FY28 as I have more confidence that BURL can achieve this target. My model assumes that BURL can achieve its 5-year outlook (FY28 targets) of 11% growth CAGR and 10% EBIT margin. The reason for using the 21 forward EBIT multiple is because this is the BURL historical average, and while I think the stock could trade higher because of a higher margin profile, I think being conservative will not do any harm. Even at 21x, I believe BURL is worth $516 in FY28 and $394 on a discount basis.

Risk

2H24 SSS growth is going to experience clearance headwinds (vs. last year), especially in 3Q24, which is going to grow against a 6% SSS growth comp in 3Q23. This may cause BURL to report a slowdown in SSS growth, and the market may not like this sequential step down. This could put pressure on the stock price as some investors (that are more conservative) will sell their shares to lock in profits, especially considering that BURL’s stock is now up ~26% on a YTD basis.

Final thoughts

My recommendation is a buy rating for BURL. I am expecting BURL to beat its FY24 SSS growth guidance given the favorable macro tailwind and that it seems conservative. Longer-term, I continue to believe BURL is well-positioned to navigate the current macro environment and achieve its long-term targets. Valuation remains attractive, and I see a possible path to BURL trading at $516 in FY28.

Read the full article here