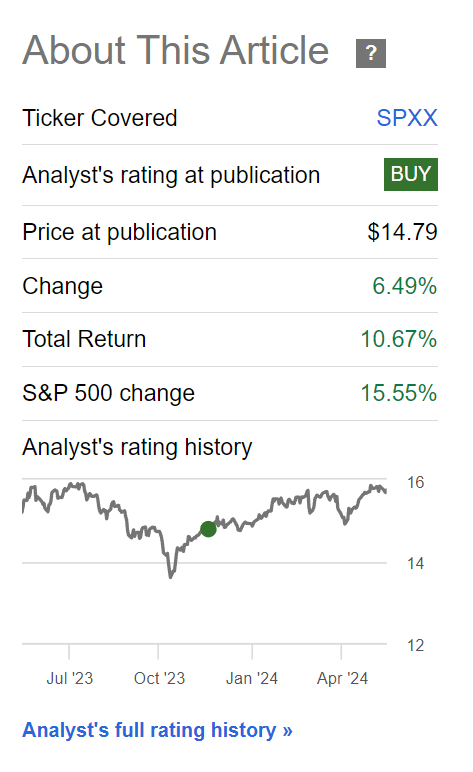

A few months ago, I wrote a bullish article on the Nuveen S&P 500 Dynamic Overwrite Fund (NYSE:SPXX), noting that the SPXX fund was trading at an attractive 9% discount to NAV with a time-tested strategy.

Since my upgrade, the SPXX fund has performed well, delivering 10.7% in total returns. However, this is still less than the S&P 500 Index’s 15.6% returns.

Figure 1 – SPXX has returned 10.7% return since December 2023 (Seeking Alpha)

Was this underperformance expected, and should investors continue to hold the SPXX fund?

By its nature, the SPXX fund is expected to underperform broad equity markets, as it trades away some portfolio upside in exchange for premium income. The SPXX fund has actually outperformed in the past few months with a 65% upside capture, as markets have been remarkably calm.

However, with the S&P 500 Index trading at some of the highest valuation multiples in history, I fear forward returns may not be as robust. If equity markets suffer a protracted bear market, the SPXX fund will likely suffer poor returns. I am downgrading the SPXX fund to a hold recommendation.

Brief Fund Overview

The Nuveen S&P 500 Dynamic Overwrite Fund is a closed-end fund (“CEF”) holding an equity portfolio that tracks the S&P 500 Index. The SPXX fund also dynamically writes call options on the index to generate income.

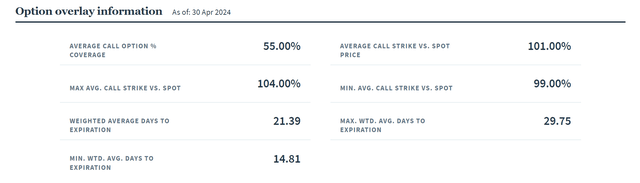

The SPXX fund sells call options covering a varying percentage of the fund’s equity portfolio, depending on the manager’s outlook. Under normal market conditions, the SPXX fund aims to sell call options on 35-75% of the notional value of the fund’s equity portfolio. This allows investors to retain some upside capture from the fund’s equity exposures while supplementing the fund’s income.

As of April 30, 2024, the SPXX fund has overwritten 55% of the portfolio with monthly call options priced at an average of 101% of the S&P 500 Index’s spot price (Figure 2).

Figure 2 – SPXX has currently overwritten 55% of the fund (nuveen.com)

65% Upside Capture Has Actually Outperformed Expectations

To reiterate, the SPXX fund employs a ‘covered-call’ strategy on the S&P 500 Index to generate income to fund its generous distributions (Figure 3).

Figure 3 – Illustrative covered call strategy (investopedia)

The main drawback of the covered call strategy is that the SPXX fund gives up on any upside above and beyond the strike price of the options sold. Since the SPXX fund overwrites ~55% of its portfolio at any given time, investors should expect the SPXX fund to give up approximately 50-60% of the upside of its equity portfolio.

If we look at SPXX’s historical returns, the range of upside capture ranges from 28% on a trailing 3-year basis (Figure 4) to 51% on a 10-year basis (Figure 5).

Figure 4 – SPXX returned 8.8% compared to S&P 500 Index returns of 31.6% on 3-year trailing basis (Seeking Alpha) Figure 4 – SPXX returned 115.8% compared to S&P 500 Index returns of 225.7% on 10-year trailing basis (Seeking Alpha)

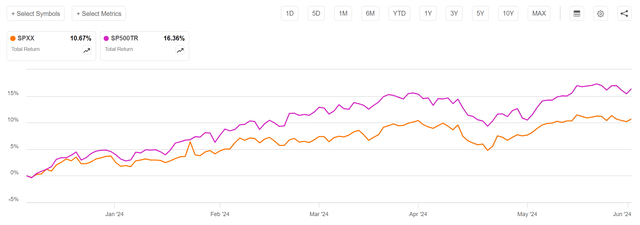

So SPXX’s market returns since my December article, 10.7% in market returns compared to the S&P 500’s 16.4% total returns, have actually outperformed expectations with 65% upside capture (Figure 5).

Figure 5 – SPXX returned 10.7% compared to S&P 500 Index returns of 16.4% since December 3, 2023 (Seeking Alpha)

What is important to note is that SPXX’s upside capture varies and depends on general equity markets.

What Happens In A Bear Market?

Another drawback of the covered-call strategy is that while upside returns are capped by the calls sold, downside returns are uncapped, as the fund can lose just as much on the underlying asset, offset somewhat by the premium income received for selling calls.

For example, during the early days of the COVID-19 pandemic, the SPXX fund suffered a 34% drawdown on market price compared to a 43% drawdown on the S&P 500 Index (Figure 6).

Figure 6 – SPXX suffered a 34% drawdown during COVID-19 pandemic (Seeking Alpha)

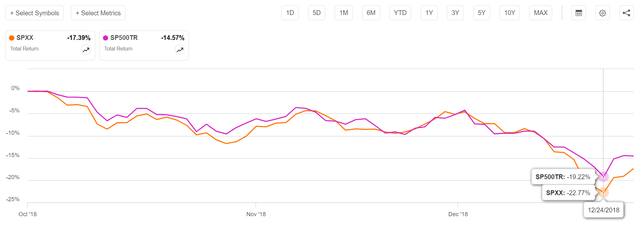

During the 2018 trade war scare, the SPXX fund actually suffered a 22.8% drawdown on market price, larger than the S&P 500’s 19.2% (Figure 7).

Figure 7 – SPXX suffered a 22% drawdown during 2018 trade war (Seeking Alpha)

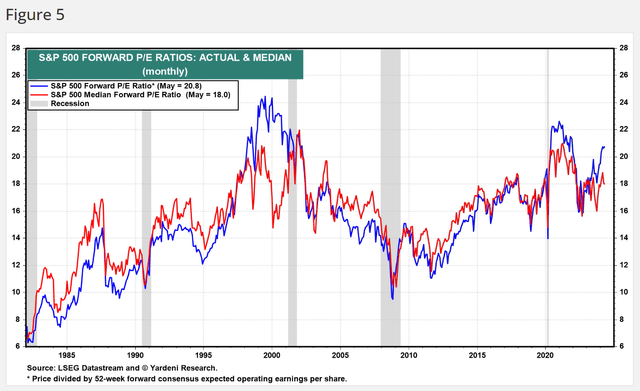

Stretched Valuations Warrant Caution

Looking forward, my biggest worry is that U.S. equity markets are trading at very stretched valuations, with the S&P 500 Index trading at 20.8x Fwd P/E, the highest valuation multiple since the 2000 dot-com bubble and early 2021 (Figure 8).

Figure 8 – S&P 500 Index trading at stretched valuations (yardeni.com)

This suggests equity markets may be vulnerable to a steep pullback if the economy deteriorates or if the market’s current infatuation with AI-related stocks wanes. If the equity markets pull back significantly in the coming months, I expect covered-call strategies like the SPXX fund to suffer a very high downside capture.

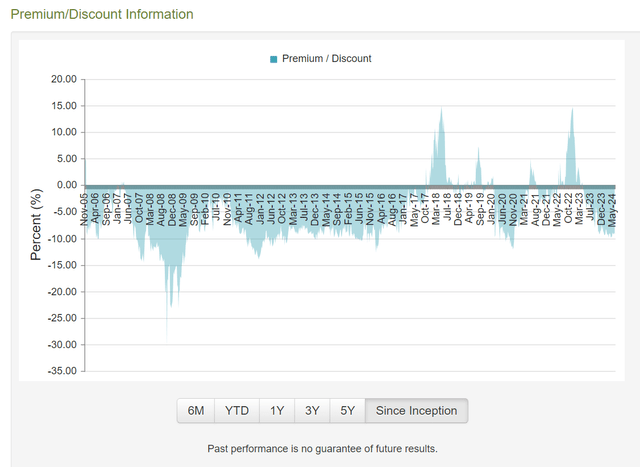

Discount To NAV May Be Saving Grace

The reason the SPXX declined more than the markets in 2018 was that the fund was actually trading at a substantial premium to net asset value (“NAV”) in 2018 (Figure 9).

Figure 9 – SPXX premium/discount to NAV (cefconnect.com)

As a reminder, closed-end funds are a type of investment fund with a fixed number of shares that are issued to investors through an initial public offering (“IPO”) like regular stocks.

After the IPO, CEFs shares can be bought and sold on a stock exchange like regular stocks, and their valuations can deviate significantly from their NAV, depending on investor demand. If there is a lot of investor demand for a particular fund, it may trade at a substantial premium to NAV, like how SPXX was in 2018.

Currently, the SPXX fund is trading at a steep 9% discount to NAV, among the highest in its history. So unless markets go into a deep panic like in the 2008 Great Financial Crisis, SPXX’s 9% discount to NAV does provide the fund with a fair amount of ‘margin of safety’ against further declines.

Risk To Cautious View

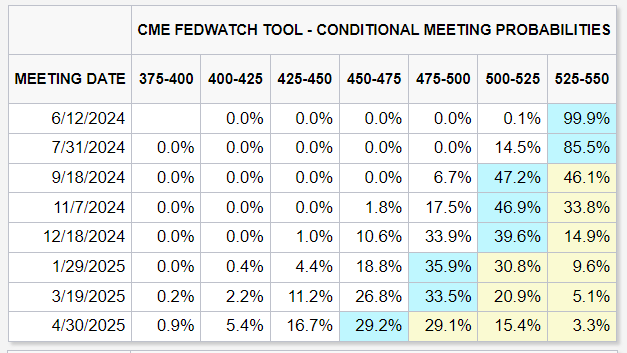

On the upside, with equity markets trading near all-time highs, it may be hard for investors to contemplate any downsides to the current market. Every worry has been brushed aside. For example, in early 2024, investors were expecting the Fed to cut interest rates 7 times this year to support the markets. However, currently, bond investors are pricing in just one rate cut, and yet equity market valuations have not suffered one iota (Figure 10).

Figure 10 – Investors have priced out Fed rate cuts (CME)

If the equity markets continue to grind sideways to higher, then the SPXX fund may continue to deliver better than expected performance (i.e. >50% upside capture), as its premium income will be additive to its portfolio returns.

Conclusion

In conclusion, I am downgrading the SPXX fund back to a hold due to my cautious view of the equity markets’ valuation. While I like the SPXX fund’s valuation discount to NAV, I worry that SPXX’s covered-call strategy may not offer much in the way of downside protection if a protracted bear market were to develop.

Read the full article here