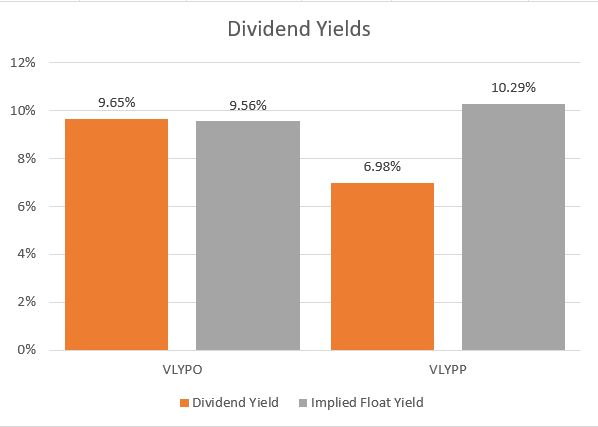

Valley National Bancorp (VLY) is a regional bank that has seen its share of struggles as it relates to high interest rates and troubles within the banking sector. The bank’s stock recently sold off and is approaching a 52-week low. Additionally, the bank has two preferred share offerings (NASDAQ:VLYPO) (NASDAQ:VLYPP) that each pay high yield dividends. VLYPO is currently yielding 9.55% on a floating rate while VLYPP is paying 6.9% and scheduled to float next June at a rate of over 10% if interest rates remain at their current levels. Last year, I analyzed why I was avoiding the bank. Based on the recent financial statements, I am still choosing not to participate in any of the share offerings.

Microsoft Excel API

Valley National Bancorp Financial Performance

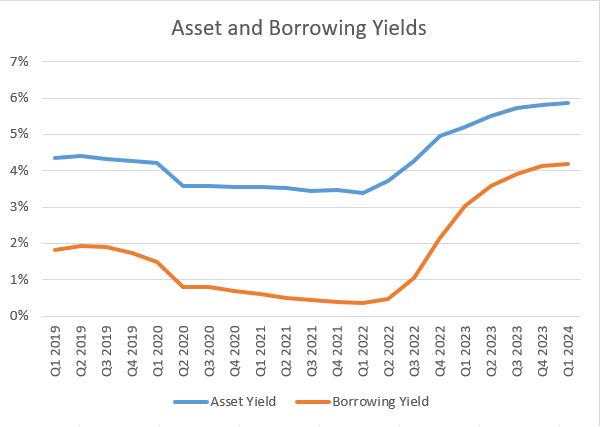

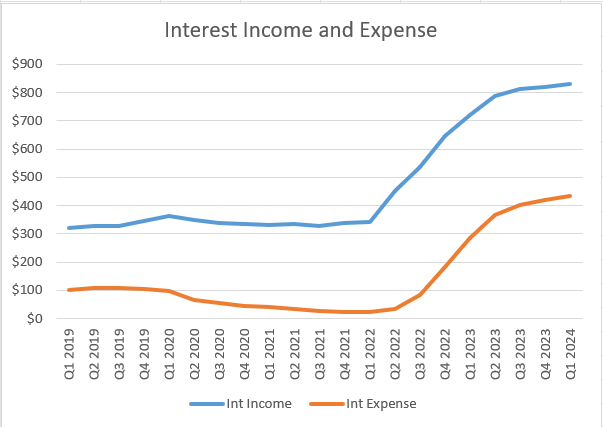

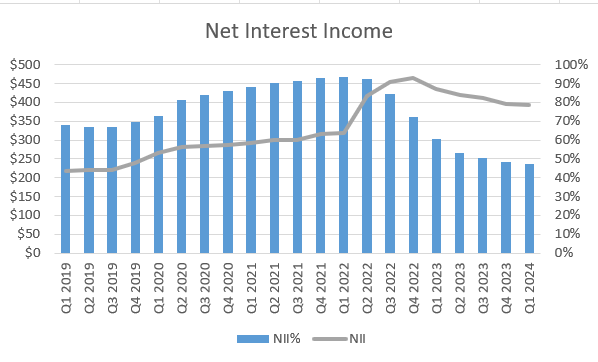

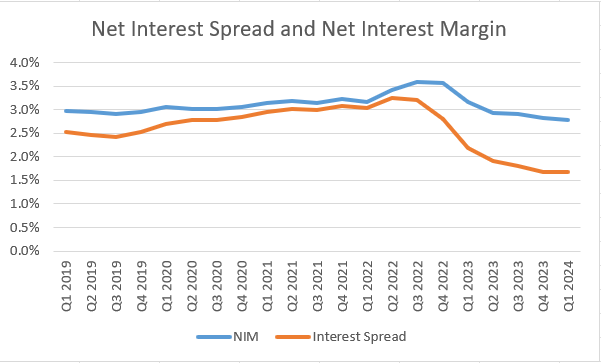

Like many regional banks, Valley National has been dealing with the effects of higher interest rates for a longer than anticipated time. Asset yields and borrowing costs both rose rapidly in late 2022 and into 2023 as the Federal Reserve increased interest rates to battle inflation. The change in interest rates caused increases in the bank’s interest income and interest expense. Unfortunately, the bank’s net interest income (interest income less interest expense) has been in steady decline since late 2022.

Bank Earnings

Bank Earnings

Bank Earnings

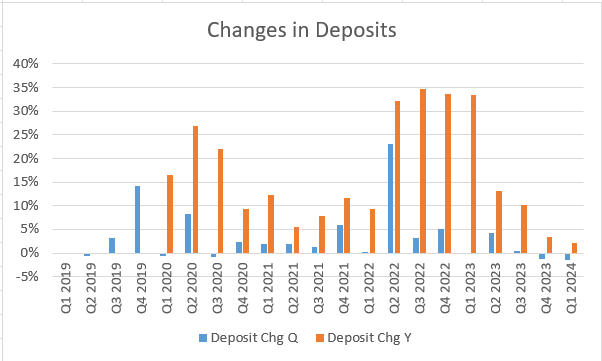

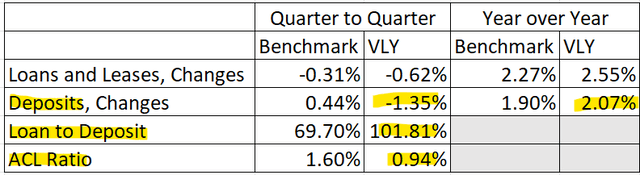

On the balance sheet side, Valley National Bancorp has been dealing with two straight quarters of deposit declines. This makes the bank more dependent on debt financing, which carries a higher interest rate and negatively impacts earnings. In the first quarter, Valley National’s borrowings nudged up, but a big change came in the bank’s shift away from short-term borrowing and into long-term borrowing. Depending on the terms of the loans, Valley National may be dealing with higher interest expenses long after the current rate regime ends.

Bank Earnings

SEC 10-Q

Risks to VLY

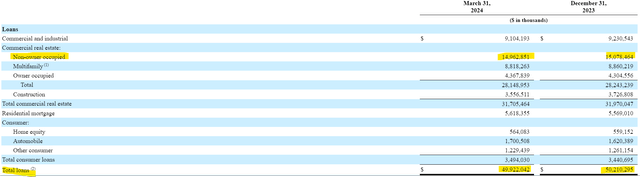

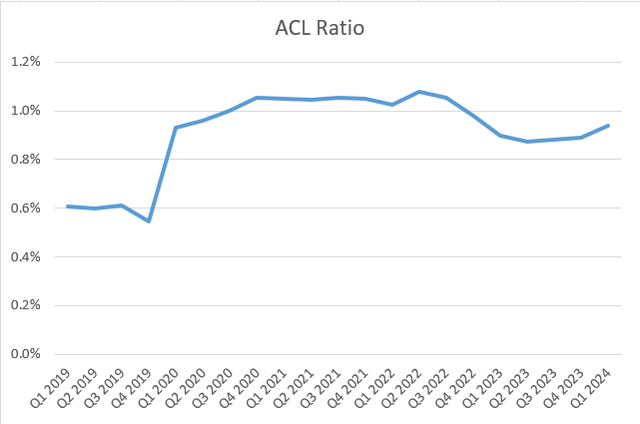

A key risk to the viability of Valley National Bancorp remains its exposure to commercial real estate (CRE), specifically non-owner occupied CRE. These loans account for approximately 30% of the bank’s entire loan portfolio. In fact, Wedbush lists Valley among its highest exposed banks to CRE. An additional concern here is that the bank’s allowance for credit losses is under 1.0%, which is below the industry average of 1.6%. Even if the bank navigates the changes in the CRE market, I believe their earnings are going to be impaired by the need to raise their credit loss allowance.

SEC 10-Q

Bank Earnings

Bank Earnings & Federal Reserve Commercial Banking Report

Another concern is the bank’s level of uninsured deposits. At the end of the first quarter, nearly a quarter of the bank’s deposits were estimated as not insured. While Valley National does have the liquidity to cover these deposits, investors should again be mindful of the cost of such transactions, which would involve higher interest expenses and lower earnings.

SEC 10-Q

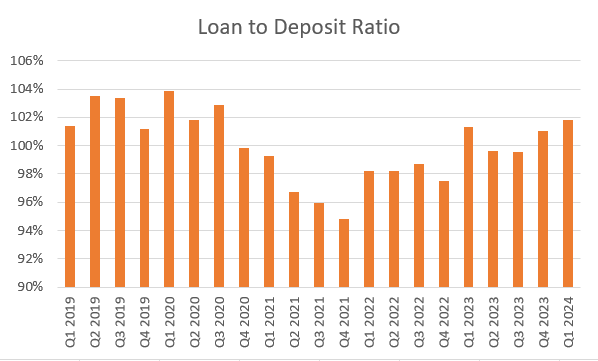

Additionally, the bank’s high loan to deposit ratio is problematic. While declining during COVID, it has since bounced back up to over 100%. This high ratio combined with the low interest spread (near 1.5%) left me concerned about how much the bank would be able to lend if it did lose deposits. The loan portfolio of the bank does not appear to be sufficiently generating the earnings necessary to support these levels, and that could become more problematic with deposit flight.

Bank Earnings

Bank Earnings

Conclusion

While I would not classify Valley National Bancorp as a threat to imminently fail, I do see risks that could cause the bank to go through the same volatile journey as New York Community Bancorp went through earlier this year. That volatility would undoubtedly cause preferred shares to sell off and would likely impair the value of common shares for the foreseeable future, therefore I am sitting out on the bank’s common and preferred shares in favor of better opportunities in the industry.

Read the full article here