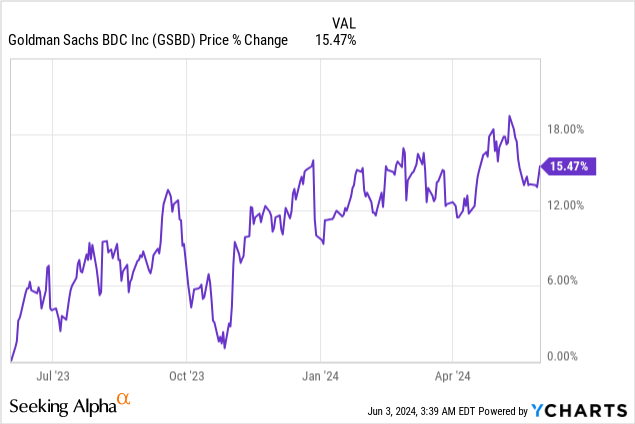

I found myself adding to my position in Goldman Sachs BDC (NYSE:GSBD) last week as the company’s share price stabilized after an undeserved sell-off earlier in May. In my opinion, Goldman Sachs BDC’s first lien strategy paired with its ability to consistently deliver high distribution coverage ratios skewed the risk profile further to the upside, especially now that the BDC’s shares trade at a lower price-to-NAV ratio. Goldman Sachs BDC also has revaluation potential as the Federal Reserve does not seem too eager to want to lower federal fund rates in the near term, which should benefit the company’s variable rate loans investments!

Previous rating

In my first work on the BDC in January 2024 — An Attractive Income Buy With A 12% Yield — I pointed to Goldman Sachs BDC’s reboot of the loan origination business and very reasonable distribution coverage of more than 1.20X as reasons to buy GSBD. I believe that Goldman Sachs BDC continues to be a very solid choice in the BDC sector, especially with shares dipping in May, resulting in a lower NAV mark-up.

First lien strategy

I like BDCs that chiefly run a first lien strategy and forgo the opportunity to earn higher yields on higher-risk investments such as unsubordinated or unsecured debt. This is my personal taste due to my desire to establish income streams that are low risk and have a high chance of being durable over time. The fastest way to mess up your dividend stream is to buy BDCs with either weak distribution coverage that have seen consistent declines in net asset value or that are tilted toward lower-quality debt investments.

In my opinion, investors can avoid a lot of disappointment (and potentially losses) if they focus on those BDCs that have very good distribution coverage (1.20X or higher) and that have a strong concentration in first liens, like Goldman Sachs BDC.

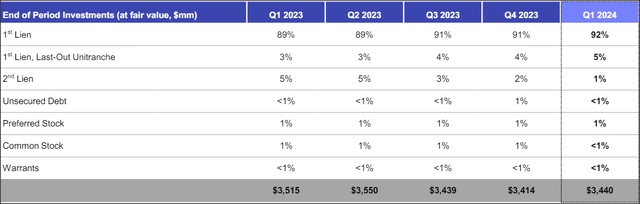

Goldman Sachs BDC is chiefly oriented towards a first lien strategy with a massive 97% of investments being a first lien.

Goldman Sachs BDC

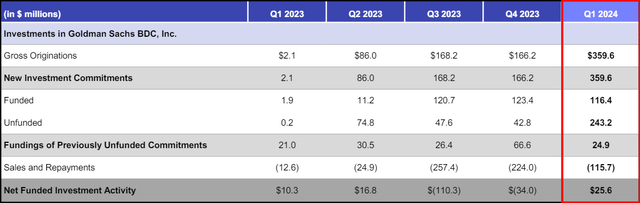

Goldman Sachs BDC’s gross originations hit $359.6M in Q1’24 which was by far the highest amount in the last year. I expect tailwinds for new gross originations in a lower-rate world, but also see an upside case for the BDC if the Federal Reserve doesn’t make changes to the federal fund rate in the remainder of the year. The reason for this is that Goldman Sachs BDC is mainly investing in variable rate loans that generate higher interest income for the BDC in a rising-rate world. Since Goldman Sachs BDC has 97% first liens in its portfolio (and only a very small share of non-first lien investments), the BDC is set to benefit from higher interest rates more than other BDCs with lower debt investment percentages.

Goldman Sachs BDC

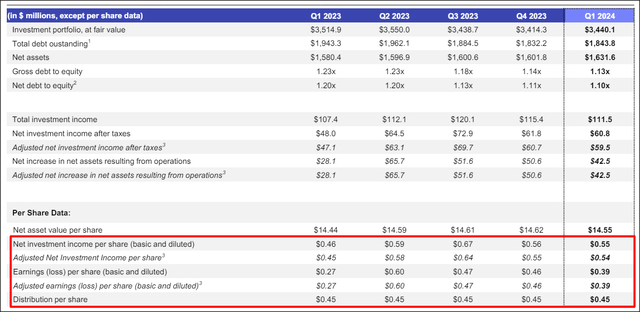

Goldman Sachs BDC had 1.22X distribution coverage (based off of regular net investment income) in Q1’24 compared to 1.24X in Q4’23 and 1.27X in FY 2023 (see red box in the chart below). The distribution coverage analysis therefore indicates that the BDC has a very robust coverage profile and is not at immediate risk of having to lower its dividend. The BDC’s net investment income increased 27% year over year, chiefly due to the company’s investments in loans that pay a variable loan rate. While some of these tailwinds are set to soften going forward, high interest rates are still going to benefit Goldman Sachs BDC in the immediate future.

Goldman Sachs BDC

Why I am buying more shares of Goldman Sachs BDC for my portfolio…

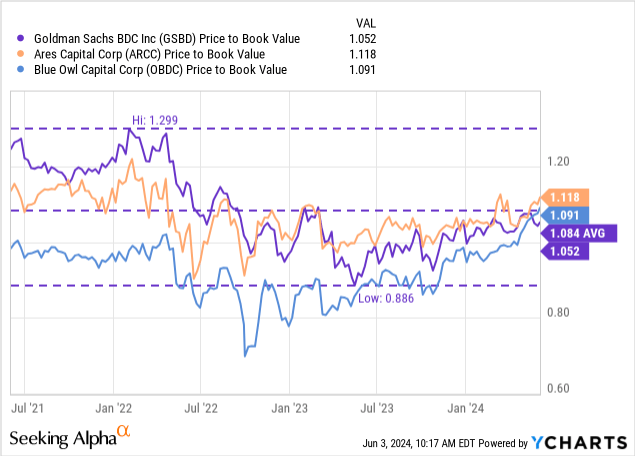

Goldman Sachs BDC has a healthy distribution coverage profile and the BDC is not that expensive: Goldman Sachs BDC is currently priced at a P/NAV ratio of 1.05X, which is below the company’s 3-year average price-to-book ratio of 1.08X. Rival BDCs, such as Blue Owl Capital (OBDC) and Ares Capital (ARCC) trade at P/NAV ratios of 1.09-1.12X, so Goldman Sachs BDC does not offer a total bargain relative to these well-run BDCs, but the main reason to own shares of GSBD relates to the company’s very strong coverage profile.

I rate both Ares Capital and Blue Owl Capital buys for income as well based on distribution coverage, portfolio composition and valuation: Ares Capital had a distribution coverage ratio of 1.15X in Q1’24 while Blue Owl Capital generated 1.12X coverage in the last quarter. I also recommended OBDC despite shares just reaching new 1-year highs, as I believe the BDC’s quality is worth the price. In the BDC market, as everywhere else, quality tends to come with a higher price sticker — Hercules Capital (HTGC) is another example — and Goldman Sachs BDC definitely belongs to this group, in my opinion.

In early FY 2022, Goldman Sachs BDC’s shares traded at an up to 30% premium to net asset value as the market rebounded from COVID-19 induced sell-offs. I don’t believe we are going to see that much of a repricing, but considering how well GSBD is doing right now, I definitely see a very solid risk profile for investors at the current valuation point.

In the longer term, considering that the BDC continues to cover its dividend at a NII/dividend ratio of 120% or higher, I believe we have a bit of upside left. Based on rival BDC valuations, GSBD could trade at a P/NAV ratio of 1.10X — which would then imply a fair value ~$16 — but the main reason to own shares of the BDC is the very solid 12% yield.

Risks with GSBD

Distribution coverage is supremely important for dividend investors, which is why I spend a lot of time analyzing the coverage situation of various BDCs. While Goldman Sachs BDC currently covers its distribution with net investment income, this may not always be the case: a change in the NII trend could foreshadow a deterioration in the distribution coverage (which is the most important metric for me to track going forward).

Final thoughts

Goldman Sachs BDC is growing and delivering consistency with its net investment income and distribution coverage profile. And, most recently, the share price dropped undeservedly in May, creating an engagement opportunity for long-term investors that are interested, potentially, in scooping up a well-supported 12% dividend yield. Goldman Sachs BDC’s first lien strategy, strong NII growth, and lower net asset value premium are all reasons why I doubled down on this high-yielding income play last week. A higher for longer rate environment is also set to benefit Goldman Sachs BDC as the company is overly focused on variable rate loans… given that GSBD is overly focused on income-producing first lien investments, the company would be set to benefit from higher rates significantly!

Read the full article here