Thesis Summary

Alibaba Group Holding Limited (NYSE:BABA) continues to trade near all-time lows, but it has seen a nice rally, followed by a bit of a pull-back in the last month.

In the last few weeks, many famed investors and large hedge funds have disclosed opening positions in Alibaba and other Chinese stocks.

Most importantly, though, there have been various reports that the CCP is going to further support the economy and specifically the housing market.

It seems to me like the CCP is giving the green light to investors, and this time it’s not just words.

While I maintain that China is still a risky place to invest, BABA is perhaps the lowest-risk investment given its size and history.

I am maintaining a strong buy rating on BABA given its attractive price, strong likelihood of government stimulus and also the evidence that shows large funds are starting to buy back into China.

BABA’s Back in Fashion

In my last piece on BABA, I discussed the fact that an improving macro and political situation would be very helpful for Alibaba. Now, this has not quite played out as we expected. While I would argue that tensions have somewhat eased in the last couple of months, China’s economy has continued to struggle. However, I see signs of this changing, and I am not the only one.

A Form 13F report submitted by the Canada Pension Plan Investment Board (CPPIB) showed that the investment institution acquired shares in several Chinese companies on the US stock market, including Alibaba, Li Auto, JD.com and NetEase in the fourth quarter. Specifically, the company acquired 3.6 million shares of Alibaba valued at $279 million, making it the largest new position added by the fund.

Soros Fund Management raised its holding of Alibaba to 75,000 shares, an increase of 87.5 percent, during the fourth quarter.”

Source: Global Times.

It seems like the Canadian Pension Plan has some strong conviction in BABA, since it is now the largest new position in its portfolio. The Soros Fund Management almost doubled its position, and these are just a couple of many examples.

Of course, funds buy and sell multiple stocks every quarter. By itself, I would not see this as enough of a sign, but combined with the latest actions of the CCP, I feel like something big may be brewing.

Some Real Stimulus

There has been a lot of talk of Chinese stimulus before, but it has not quite materialized. The issue is that China has always been a lot more conservative than the U.S. with its policies. Now, however, we are seeing an unprecedented form of direct fiscal stimulus that will soon hit the economy.

Last Friday, the People’s Bank of China said it would make $42.25 billion available to local governments to shore up the property market. While this may not sound like a lot, the measure should unlock 500 billion yuan in financing for purchases in the housing sector.

At this stage, it’s mainly SOEs and local governments to implement the policies, but their resources may be too limited to move the needle at the macro level,” he said. “Later on, we might see more efforts from the central government.

Source: Larry Hu, Chief China economist at Macquarie.

But even if it is local governments implementing the policies, the funding will be coming from the Central Bank itself, which doesn’t really have a limitation on the funds it can extend.

And this is not all. Next Saturday, the China Securities Regulatory Commission (CSRC) is expected to announce new market-related policies at the Lujiazui Forum.

To top things off, all this comes at a time when the IMF has actually bolstered its forecast for Chinese GDP, which is expected to grow 5% in 2024.

Alibaba; Still the best China play?

With all of this, now might be a good time to dip your feet in Chinese stocks and markets, and I believe Alibaba is one of the best ones.

Although there are certainly stocks with more upside potential, these are also more risky. Alibaba, on the other hand, is a household name with a long and established track record in the stock market.

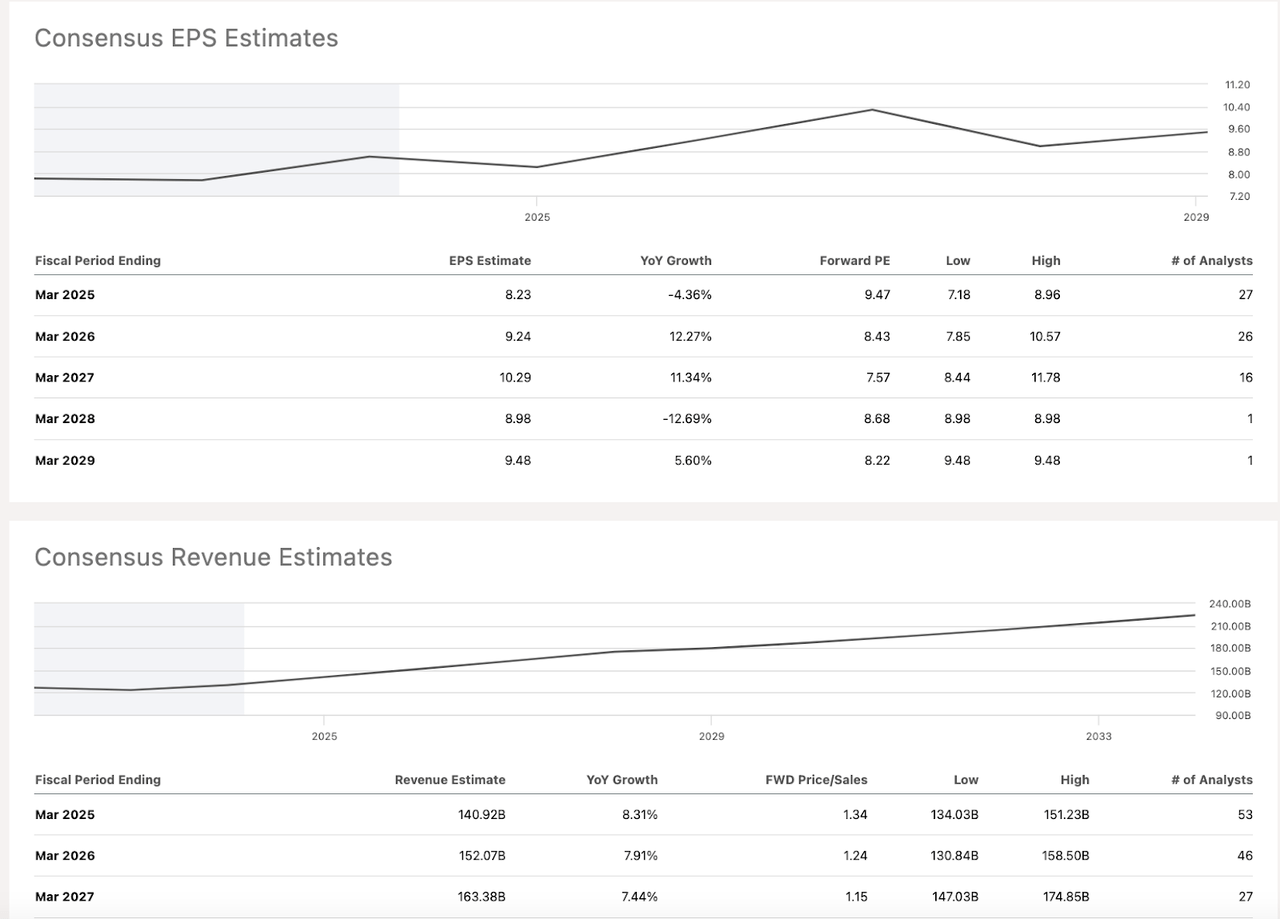

The stock has struggled somewhat with its EPS growth.

BABA Revenue and EPS estimates (Seeking Alpha)

With that said, EPS are expected to bottom in 2025 and then grow at over 10% yearly until 2028. Meanwhile, revenue growth is expected to come in at around 8% for the next 3 years.

It is certainly not crazy growth, but this means it is also that much easier for BABA to surpass these conservative estimates, in my opinion.

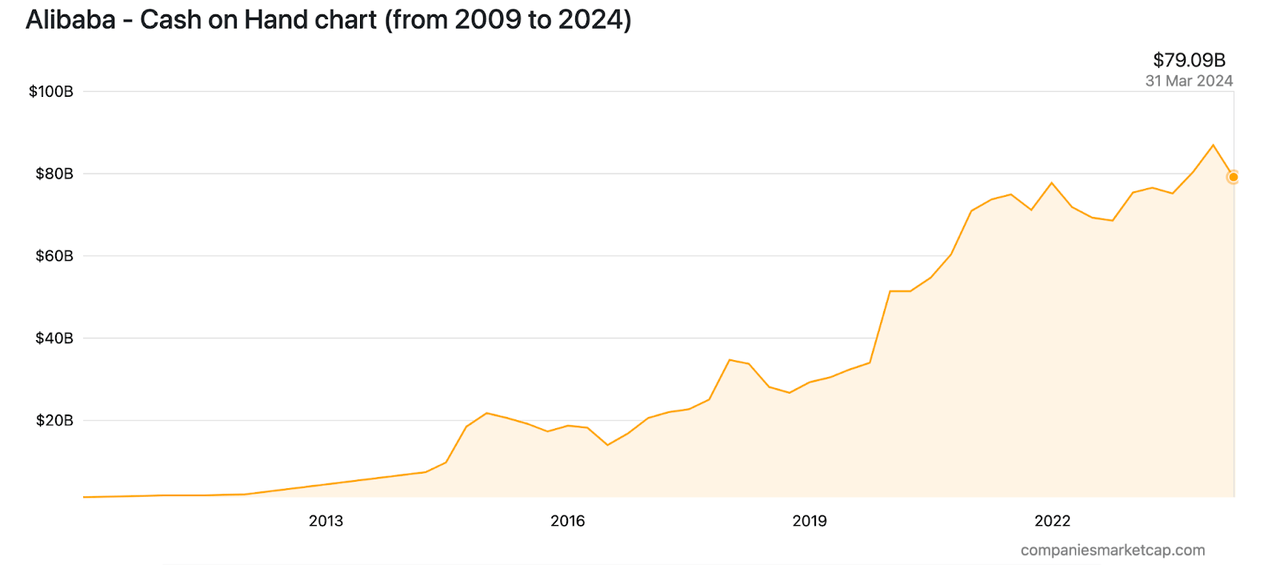

Ultimately, it is cash that moves markets, especially with a foreign stock like BABA. Returning cash through a dividend or buybacks will go a long way in helping the valuation.

Cash on Hand (companiesmarketcap.com)

Alibaba currently holds almost $80 billion in disposable cash in its balance sheet.

As political relations and the economy begin to normalize, I’d expect to see Alibaba return to its previous trading multiples, or at least an average.

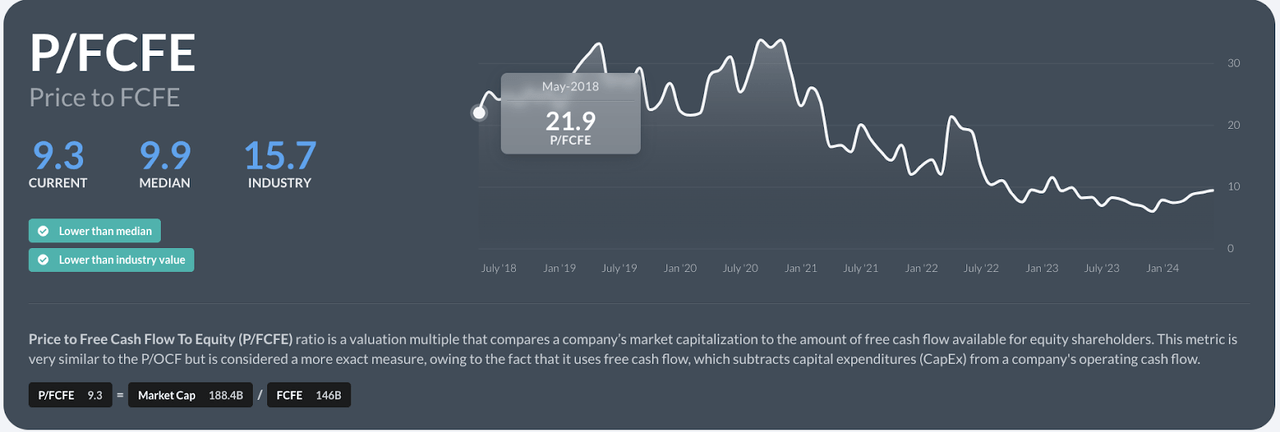

P/FCFEE (Alpha Spread)

We can see that the P/FCFE is historically low for BABA. This traded at 22x P/FCFE in 2018, reaching a high of 30x cash flow by 2020.

At today’s ratio of 9.3, I think we at least have an upside to meet the industry average of 15, meaning the stock could appreciate a good 70% from here.

Takeaway

Investing in Alibaba doesn’t come without risk, of course, and most investors are well aware of what these are. The ADR structure puts off many investors, as does the fact that the CCP has such overwhelming control over its companies.

Nonetheless, Alibaba Group Holding Limited stock is cheaply priced and seems to have found a bottom. It looks like the PBoC and CCP are finally ready to step up their support of the economy, and this is great news for BABA and, the way I see it, for investors in Chinese stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here