The KraneShares Bosera MSCI China A 50 Connect Index ETF (NYSEARCA:KBA) tracks the MSCI China A 50 Connect Index. The China A 50 Connect Index is made up of the 50 largest China A Shares companies. For the uninitiated, China A-Shares refers to stocks of Chinese companies traded on the Shanghai and Shenzhen stock exchanges. By investing in KBA, investors can gain diversified exposure to some of the largest and most liquid Chinese companies. The fund was incepted in 2014, and at the time of writing has roughly $203M in assets.

3 pillars of Chinese equity market woes

Investors paying attention to international markets are well aware that there have been significant headwinds, both in terms of underperformance and volatility, for Chinese equity markets over the past few years. They are generally attributed to the following:

1.) China’s zero COVID policy: China had one of the strictest COVID policies globally. The long tail of this very strict lockdown is still impacting Chinese companies and consumers.

2.) Property market crisis: Evergrande’s collapse in 2020 led to a crack-down on excessive borrowing to help rein in debt burdens for developers. This has been a drag on the once burgeoning real estate sector in the country ever since.

3.) Increased geopolitical tensions: Investor sentiment has been impacted by China’s escalating geopolitical tensions with both the US and Taiwan. These tensions are accelerated by the global race to shore up AI supply chains, as well as China’s increased military presence around the island of Taiwan.

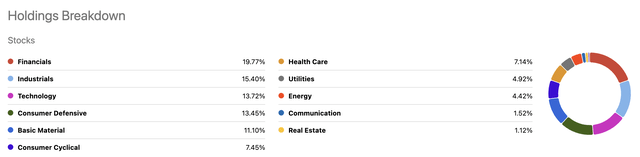

Well diversified across sectors and holdings

This is a well-diversified sector fund, with top allocations going to financials, industrials, tech, and consumer defensives. The fund’s smallest allocations go to energy, communications, and real estate. KBA employs a sector balancing methodology.

Seeking Alpha

At the individual holdings level, we see a similar diversification story. The top 10 holdings make up about 47% of the fund’s total assets. The largest allocation goes to liquor distributor Kweichow Moutai Co, which is known for its popular brand of Chinese alcohol Baijiu. While Kweichow has a 5-year total return of ~88%, it has returned -1.6% on a trailing 1-year basis. The second largest position goes to Contemporary Amperex Technology, a lithium-ion battery manufacturer, down 10.7% on a trailing 1-year basis.

Seeking Alpha

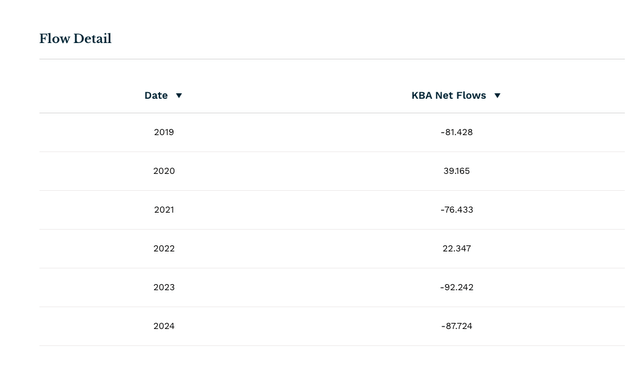

Flows have not recovered in 2024

KBA has struggled with flows in the preceding 5-year period. Sluggish flows have plagued many Chinese funds due to the issues described above. However, the fund did see positive net inflows in 2020 and 2022, despite the COVID period. Year-to-date, the fund has already amassed nearly as many outflows as 2023. However, we are only 5 months into the year and if there is a sustained rally in Chinese equity markets we could see this figure diminish.

ETF.com

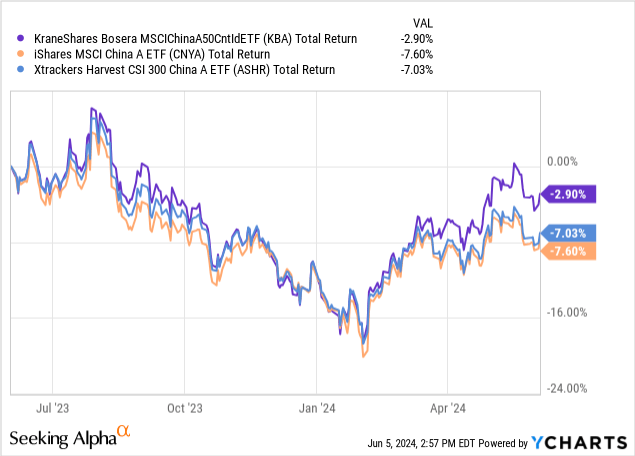

Performance comparison

When comparing KBA to two similar A shares funds, CNYA and ASHR, we can see all funds are in the red on a trailing 1-year basis. However, KBA is still outperforming its competitor funds. This is likely due to KBA’s sector balancing methodology, which is a differentiator from these other A shares fund.

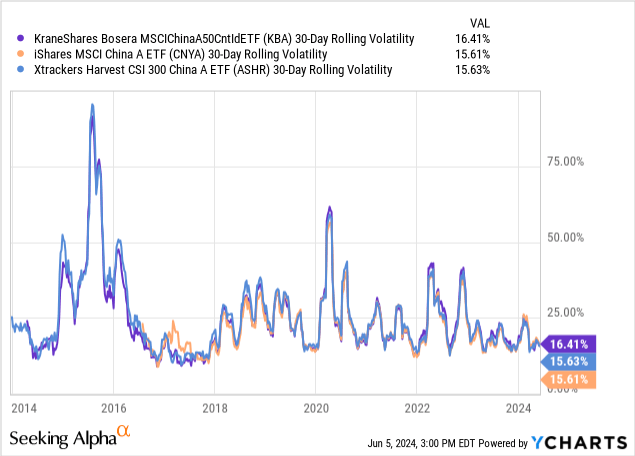

From a risk perspective, KBA’s volatility is slightly elevated, while the other two funds are more in line with one another. All of these figures are more elevated than a standard emerging markets probability profile. The 30-day rolling volatility for the iShares MSCI Emerging Markets fund is currently ~14%. This is in line with expectations given the challenges that have been unique to China within the recent period.

Dawn breaking on the Chinese equity market, or is it a value trap?

Select sectors in China have started to make a comeback in 2024, due in part to support by the Chinese government. However, it remains to be seen how long the optimism will remain. The question I’m asking myself is whether or not COVID catalyzed a correction in Chinese markets that is more structural than anything else. China as the global demographic darling has long since passed. India is now the most populated country in the world. COVID has done long-term damage to investors’ psyches. However, it is hard to overlook the favorable valuation multiple for KBA. It has a current book value of 1.58 and a P/E of 13.5x. It’s currently yielding 2.17%. Regardless if foreign investors are more skeptical than ever, this fund is still heavy companies that will enjoy sustained domestic demand.

Conclusion

KBA provides exposure to one of the largest global markets and has made strides since the Chinese equity market slowdown that began in the immediate aftermath of COVID. It has struggled from a flows perspective. Recent crises have forced the government’s hand to take proper inventory of the current business climate. I think the market’s retreat could ultimately be a boon for investors, as efforts to augment corporate governance could push equities further. With the current valuation multiples and global positioning, I currently rate KBA as a buy.

Read the full article here