Investment Thesis

Shopify (NYSE:SHOP) shares experienced a steep decline after the company released its first quarter earnings for 2024. While revenues of $1.86 billion surpassed analyst expectations, the company reported a net loss compared to a profit in the same period last year. However, this loss stemmed from a charge associated with the sale of Shopify’s logistics business.

The decline year-over-year was primarily due to the sale of the logistics business and lower headcount, partially offset by increases in marketing spend.

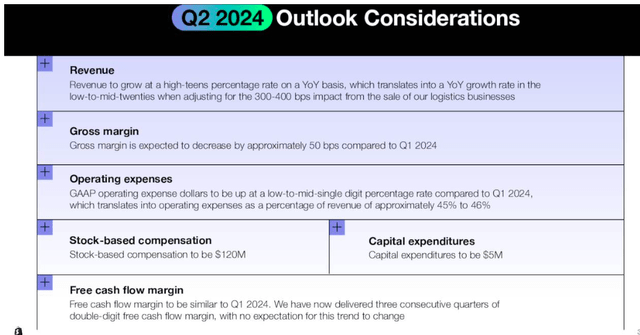

Investors were most concerned by Shopify’s guidance for the current quarter. Revenue growth is projected to be in the high teens YoY, which represents a slowdown compared to recent quarters. This fell short of expectations for continued high-growth performance. Additionally, the company anticipates operating expenses to rise at a rate exceeding analysts’ predictions. Gross margin is also expected to decrease slightly due to the divestiture of the logistics business.

Shopify earnings presentation

I believe this is a challenging economic scenario with a slowdown in economic spending; however, I believe Shopify is still well-positioned for long-term success. However, factors like revenue growth over time and rising expenses need to be monitored. The combination of the mixed earnings report and cautious guidance resulted in a significant drop of 18% in the share price.

In this article, I will go into the details of the company and see if it’s a candidate for my growth at reasonable price portfolio over the long term. To accomplish this, I will review factors including, management, corporate strategy, and financial health.

At the end, you will read that I find Shopify undervalued with growth potential. I find that while Shopify’s current performance and guidance suggest short-term headwinds, I remain positive on its long-term prospects. The economic cycle can certainly pressure stock prices, especially for companies exposed to consumer spending. However, Shopify’s core business- e-commerce- is poised for continued growth thanks to the ever-increasing shift to online shopping worldwide, as reflected by Shopify’s increase in Gross Merchandise Value (GMV) and international growth.

Shopify earnings presentation

Additionally, the company boasts characteristics that indicate its potential to thrive for the next decade. These include a strong market position, a diversified revenue stream, and a focus on innovation. Therefore, despite current volatility, I’m initiating coverage of Shopify with a Buy rating.

Management Evaluation

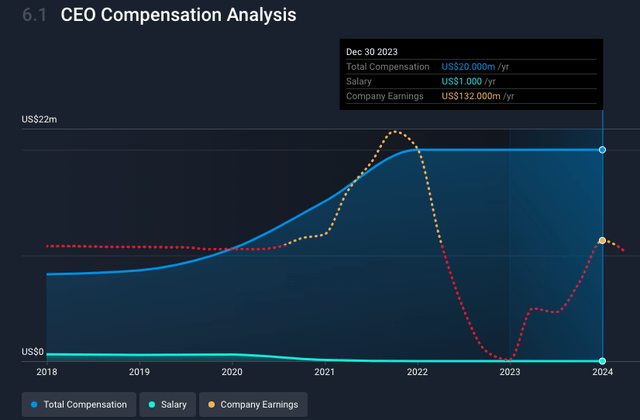

Shopify’s CEO, Tobias Lutke, cofounded the company in 2004 and has been instrumental in its growth, serving as both CTO and CEO. Despite a low Glassdoor rating, likely due to workforce reductions last year, his long-term commitment is evident. Lutke owns a significant 6% portion of the company with 40% voting power and receives most of his compensation in stock awards with $20 million in the last two years and $15 million the year before rather than taking a cash salary which is just $1 (yes, $1). This strong alignment with shareholders’ interests suggests he’s invested in Shopify’s success for the long haul, and therefore I find he has a “high alignment ratio” with the company’s long-term success. Although, I believe he should let someone with more management experience run the company growth strategy.

simplywall.st

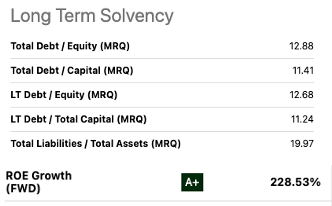

Jeff Hoffmeister, Shopify’s CFO since 2022, has a background in managing high-growth tech companies. Despite joining during a period of layoffs that impacted employee morale as seen in the company reviews on Glassdoor, he’s overseen positive financial trends. Under his leadership, Shopify has managed debt effectively to finance projects, and both FCF and ROE have been steadily increasing. I find this financial performance might be adept at balancing growth with responsible financial management.

Seeking Alpha

Overall, I find Shopify leadership a mixed bag. CEO, Tobias Lutke, has deep company knowledge and shareholder alignment. However, layoffs under his watch likely contributed to the low Glassdoor rating. CFO Hoffmeister brings tech finance experience, managing debt and boosting FCF and ROE. Yet, his arrival coincides with layoffs and his impact on long-term growth strategy remains unclear.

Glassdoor

Shopify management have strengths, but I find that they fall short of expectations for a growth company, and therefore I give them a rating of just “Meets Expectations”. Lutke commitment is admirable, but his experience might be insufficient for Shopify’s current growth phase. Hoffmeister’s financial skills are valuable, but his recent appointment leaves his strategic influence uncertain. Further, the biggest challenge I find is the need for a clear growth strategy.

Corporate Strategy

Shopify’s growth hinges on expanding its ecosystem. They focus on adding new stores to their marketplace, giving merchants more sales channels like social commerce, and enabling omnichannel experiences. They contrast with Amazon’s strategy of leveraging its massive customer base to grow its marketplace and prioritize cloud computing services (AWS) for additional revenue streams.

I have created the table below comparing Costco current strategy to some of it current competitors:

|

Shopify |

Amazon (AMZN) |

eBay (EBAY) |

Wix (WIX) |

|

|

Corporate Strategy |

Ecommerce platform for SMB to sell directly to consumers-Focus on expanding its app marketplace and offering additional sales channels, including social commerce. |

Online marketplace offering a platform for third-party sellers-Growth strategy emphasizes cloud computing services (AWS) and expansion into new markets |

Online marketplace for buyers and sellers-Focuses on attracting new sellers through lower fees and improving user experience. |

Website creation platform with ecommerce functionality- Growth strategy emphasizes increasing international sales and building stronger community for sellers. |

|

Advantages |

Easy to set up and use, customizable stores, strong app marketplace for additional features. |

Massive customer base, fulfillment and logistics services. Brand recognition. |

Established brand, large buyer base, wide variety of products, lower fees for high-volume sellers. |

Easy to use drag-and-drop website builder, beautiful design templates, affordable pricing |

|

Disadvantages |

Transaction fees can be expensive for high-volume sellers, limited control over fulfillment. |

Highly competitive, strict seller guidelines, high fees for FBA sellers. |

Highly competitive, lower margins due to auction format, less control over branding |

Limited customization, compared to Shopify, may not be ideal for complex e-commerce needs. |

Source: From companies’ website, presentations, Seeking Alpha

I believe that while Shopify offers ease of use and customization, it charges transaction fees and may not be ideal for high-volume sellers due to limited fulfillment control. It’s hard to compare market share as Shopify model is not the same as traditional online marketplaces like Amazon’s, eBay’s or Etsy (ETSY). Shopify aims to empower merchants by offering all the tools to allow them to set up an independent online shop.

Shopify.com

Shopify’s competitive advantage is its financial strength and dedication to independent online stores to build their brand and sell exclusive products that otherwise wouldn’t’ be able to do in the Amazon marketplace.

Further, their financial strengths give it a strategic advantage for growth. This focus allows them to invest heavily in growth initiatives like international access compared to smaller competitors like Wix Stores (WIX), BigCommerce (BIGC), Squarespace (SQSP), and open-source solutions like WooCommerce.

Shopify website

Valuation

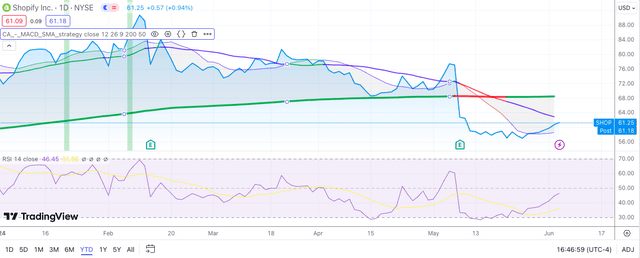

Shopify currently trades at around $61.25, still down around -20% since its last reported earnings in early May.

To assess its value, I employed a conservative 11% discount rate, this rate reflects the minimum return an investor expects to receive for their investments. Here, I am using a 5% risk-free rate, combined with the additional risk premium for holding stocks versus risk-free investments, I’m using 6% for this risk premium. While this could be further refined, lower or higher, I’m using it as a starting point only to get a gauge for unbiased market expectations.

Then, using a simple 10-year two staged DCF model, I reversed the formula to solve for the high-growth rate. To achieve this, I assumed a terminal growth rate of 4% in the second stage. Predicting growth beyond a 10-year horizon is challenging, but in my experience, a 4% rate reflects a more sustainable long-term trajectory for mature companies. You can find historical GDP growth data to explore past trends here. Again, these assumptions can be higher or lower, but from my experience I feel comfortable using a 4% rate as a base case scenario. The formula used is:

$61 = (sum^10 EPS (1 + “X”) / 1+r)) + TV (sum^10 EPS (1+g) / (1+r))

Solving for g = 28%

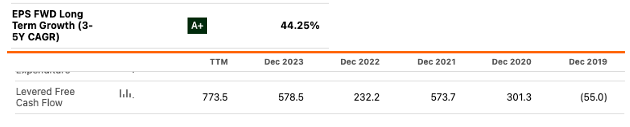

This suggests that the market currently prices SHOP EPS to grow at a rate of 28%. According to Seeking Alpha, analyst consensus EPS is expected to grow at a 44.25% and its FCF is trending higher.

Seeking Alpha

Therefore, I believe SHOP is undervalued at this point. However, it’s important to note that despite this undervaluation, I am expecting a clearer message from management about a more concrete growth strategy. I will be a buyer on this weakness as I believe they will figure it out, and I also understand that the stock might be pressured due to the current uncertainty in the economic cycle.

Technical Analysis

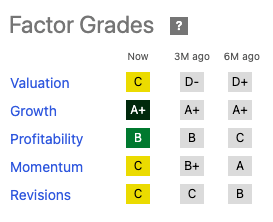

SHOP has had a hard time bouncing after it reported earnings, creating a support level at around $57-$60. Its RSI is at around 46, having crossed it 14-day average of 36 and pointing to keep increasing, indicating that the stock might increase in value. However, momentum according to Seeking Alpha still neutral:

Seeking Alpha

I believe the market is waiting for concrete evidence of Shopify’s growth initiatives translating into results. The current uncertainty surrounding the company, coupled with the broader headwinds in consumer discretionary stocks, is creating a volatile environment. Shopify’s reliance on consumer spending add another layer of complexity. However, I believe in the company long-term potential success due to its strong market position and healthy financials.

TradingView

Therefore, I expect some short-term volatility in the stock price, potentially ranging between $60-$68 until the next earnings report. While cautiously optimistic, I consider the company as a growth at a reasonable price over the long term.

Next earnings are July 26th

Takeaway

Shopify’s recent earnings miss and cautious guidance caused a drop, but a closer look reveals a potential long-term winner growing at a reasonable price. Strong fundamentals like a dominant market position and focus on innovation positions them for future growth in the booming e-commerce market. I consider the stock undervalued due to short-term headwinds from an economy slowdown, and I’m also adding to this an unclear growth strategy from management. However, I am confident management will eventually figure it out and believe in Shopify’s long-term potential, starting my coverage with a cautious Buy.

Read the full article here