Lululemon Athletica Inc. (NASDAQ:LULU) is well-known for high-quality yoga pants, and they are expanding their product categories into running shoes and men’s category. I favor Lululemon’s superior comparable store sales growth and their direct-to-consumer initiative. I believe Lululemon still has a huge runway for future growth, especially in the international markets, and I am initiating with a “Buy” rating with a one-year price target of $350 per share.

Category Expansion and International Market Growth

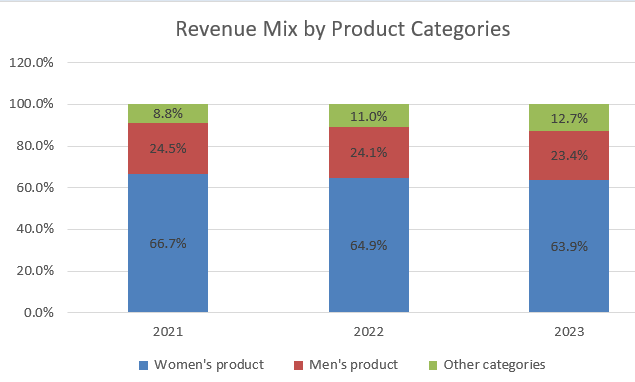

Lululemon offers performance apparel, footwear, and accessories marketed under the Lululemon brand, and the company has already expanded its original yoga category into footwear and some other sports categories such as running and training. The revenue contribution from women’s products has dropped from 66.7% in FY21 to 63.9% in FY23.

Lululemon 10Ks

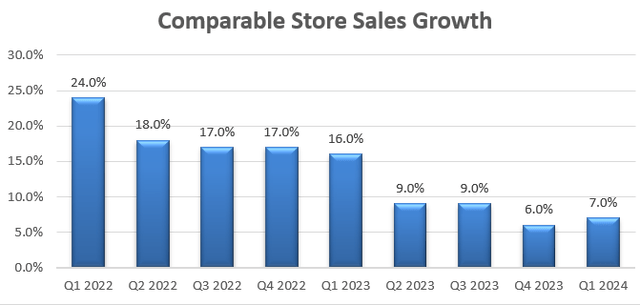

Lululemon has been delivering strong revenue growth over the past few years, with 19% comparable sales growth in FY22 and 9% in FY23. I think the strong growth has been driven by the following factors:

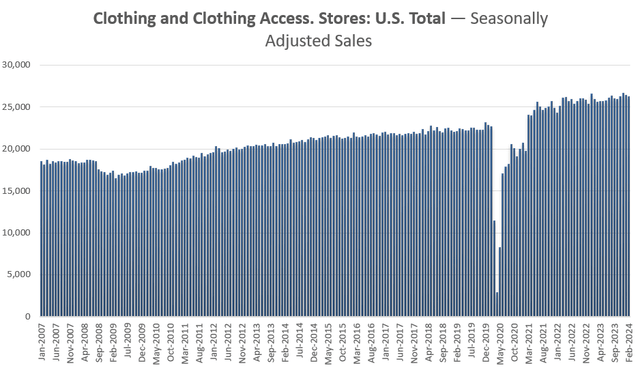

- The overall clothing and clothing accessories market in the U.S. has been quite healthy over the past few years, as depicted in the chart below. While the market got disrupted by supply chain during the pandemic, the market has recovered in the post-pandemic era.

Bureau of Economic Analysis

- One of Lululemon’s key advantages is its fast product innovation, incorporating fashions into its product designs. For instance, the company is going to launch leggings that use hydrogen yarn in July. In addition, as indicated over the earnings call, Lululemon has identified some new growth areas such as running, golfing and training. I anticipate the company will continue leveraging its fashion-design capabilities in the near future.

- International market only accounted for 21% of total revenues in FY23, and the company believes the international markets can achieve 50% of total revenues in the future. Notably, China represents 10% of total business, and is growing rapidly. In Q1 FY24, China grew by 52% year-over-year. Lululemon only has 127 stores in China, and I think the market will have a huge runway for future growth.

Recent Quarter Review

Lululemon reported its Q1 FY24 result on May 5th after the market close with 7% comparable store sales growth. This marks a continuing deceleration compared to previous quarters.

Lululemon Quarterly Earnings

The slowdown is driven by the following reasons:

- The Americans market had a flattish growth in comparable sales growth in the quarter. During the earnings call, the management explained that they missed the growth opportunity in women’s and bag categories, by not maximizing color palette and core assortments, especially in leggings.

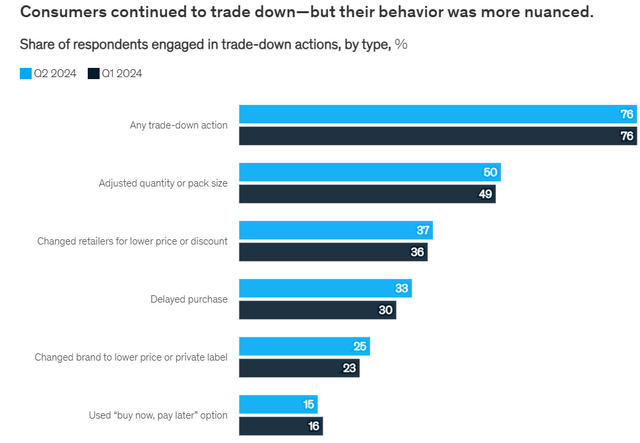

- Amid the high-interest rate macro environment, consumer spending tends to be weak, especially in discretionary spending categories. According to a recent survey conducted by McKinsey, U.S. consumers continue to trade down their spending, or adjust their quantity or pack size.

McKinsey Report

If the current high-interest rate persists, I’d forecast Lululemon will continue to have a challenging growth in the U.S. market.

FY24 Outlook

Lululemon maintained its guidance for the full year, forecasting 10%-11% revenue growth and a 10bps margin expansion. For its near-term growth, I am considering the following:

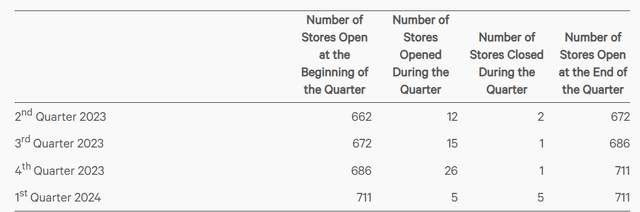

- New Store Openings: Lululemon currently has 711 stores in total, and the company believes they have a huge runway for new store openings. In FY24, the company plans to open 5-10 new stores and renovate 15–20 stores. Based on my calculations, the new store opening could contribute around 5% of growth to its top line.

Lululemon Q1 FY24 Earnings

- Comparable Store Sales Growth: in the near-term, I anticipate the company will continue delivering 6%-7% of comparable store sales, assuming 2% growth in North America, 30% in China and 25% growth in other international markets. Lululemon only has around $2 billion revenue outside the U.S. market, indicating substantial potential for international market growth.

As such, I assume the company will deliver 12% total revenue growth in the near term.

Valuation

The revenue contribution from new store opening will decelerate gradually in the future due to higher base. I estimate that the new store opening will contribute around 3% growth to its topline from FY28, when the company’s total number of stores will reach 770. Assuming the same comparable sales growth, the total revenue is forecast to grow by 10% from FY28, then slow down to 8% from FY31.

The growth in e-commerce is a major margin driver for the company. E-commerce represents around 45% of total revenue, growing at mid-teens in the past. Lululemon has done an impressive job promoting its direct-to-consumer business model, and they currently have around 20 million members in North America. The fast-growing e-commerce business will help the company drive its operating margin.

I forecast a 30bps annual margin expansion in the model, assuming 20bps leverage from gross profits and 10bps leverage from SG&A.

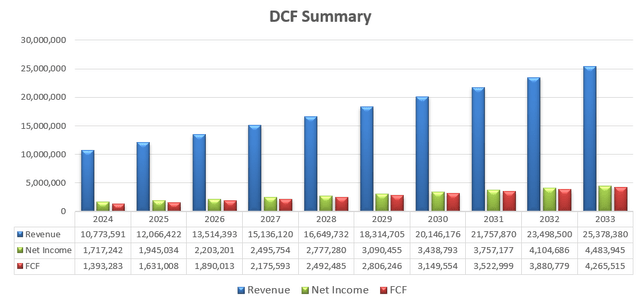

With these assumptions, the DCF summary is:

Lululemon DCF – Author’s Calculations

The free cash flow from equity is calculated as follows:

Lululemon FCFE- Author’s Calculations

The cost of equity is calculated to be 13.3% assuming: risk-free rate 4.22% ((US 10Y Treasury Yield)); Beta 1.3 ((Seeking Alpha)); equity market premium 7%.

Discounting all the future FCFE, the one-year price target is estimated to be $350 per share.

Risks

- China Operations: China represents 10% of total revenue, growing at 50%+ in revenue. Several consumer brands including Nike (NKE), adidas (OTCQX:ADDYY) and Estée Lauder (EL) have already experienced sluggish growth in China due to weak consumption sentiments in China. With only 127 stores in China, Lululemon is still establishing its presence and popularity, but it’s possible that growth in China may taper off as the business scales up.

- Lululemon is quite successful in the yoga market, and the company is expanding into other categories such as shoes and bags. They are going to face strong competitions from existing players such as Nike. It might be difficult for Lululemon to achieve the same level of success in these new categories.

- In May 2024, Lululemon announced the departure of its Chief Product Officer, without any plan to replace the role in the future. The leadership departure raises concerns about potential issues with product designing within the firm.

Conclusion

In my view, Lululemon Athletica Inc. has demonstrated a solid strategy and strong execution in areas such as fashion design, product development, e-commerce and international market expansions. The company still has a hung runway for the future growth. I am initiating with a “Buy” rating with a one-year price target of $350 per share.

Read the full article here