Cracker Barrel Old Country Store (NASDAQ:CBRL) has no choice. It has to change.

The stock had long been cherished as an equity-income play. (Many old headlines visible in the Seeking Alpha CBRL Analysis archive confirm this.) And its yield recently topped 9%.

But that angle is now gone.

CBRL stock, anticipating a dividend cut, fell 36% from the start of this year until May 15th. That’s just before management announced that the company would, indeed, slash the quarterly payout from $1.30 to $0.25 starting with the July 2024 payment.

This doesn’t necessarily mean CBRL is a dumpster fire. But it has had to experience a significant and quick turnover in its shareholder base.

Its huge population of equity-income shareholders had to sell given the stock’s now mundane yield near 2%. Meanwhile a new shareholder population has been slower to emerge.

Owning the stock today involves a completely different investment theme…

Brand Rejuvenation — Necessary, But Hard to Do Successfully

The investment case for or against CBRL now depends on its success as a “special situation” based on its newly launched brand rejuvenation program.

Such efforts are undertaken for brands that lose relevance to, or don’t resonate with modern audiences.

AlphaGraphics suggests this is “necessary for all businesses at one point or another.” None can remain static because environment and consumer tastes change.

Brand rejuvenation can generate excitement, boost sales, regain relevance, and separate from competition.

Julie Masino, CBRL’s new CEO since November 1, 2023, believes the company’s brand needs that very thing. And she launched a program to do that.

Hence the dividend cut. Masino believes the money would be better spent to revitalize the brand.

The company’s recent performance supports Masino’s priorities.

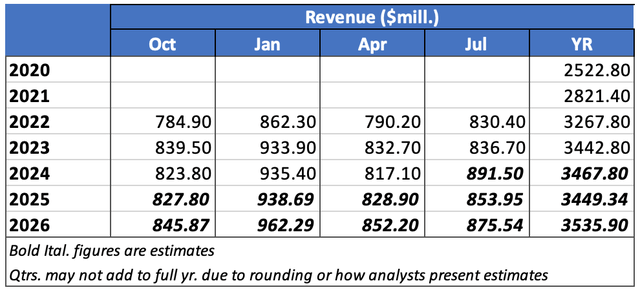

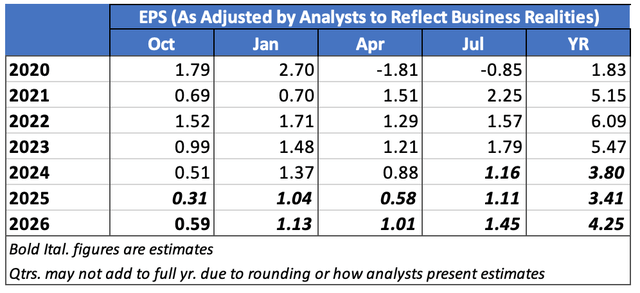

We see this CBRL’S quarterly Sales and EPS trends.

Seeking Alpha Estimates Presentation Seeking Alpha Estimates Presentation

To be fair, CBRL isn’t the only restaurant chain facing challenges today. Food and labor costs are up. And more recently, consumers have been showing less inclination to spend.

But CBRL can’t blame everything on the economy.

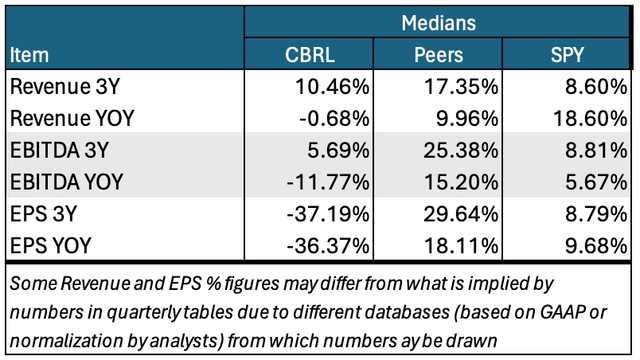

It’s been underperforming its Restaurant peers for a while now.

Author’s computations and summary from data displayed in Seeking Alpha Portfolios

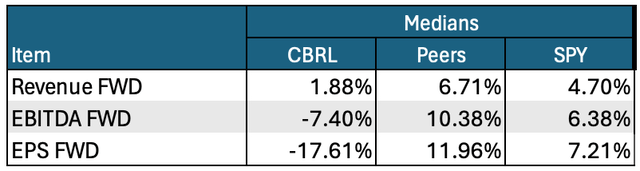

And based on CBRL’s business as it now stands, analysts expect it to continue underperforming in the future.

Author’s computations and summary from data displayed in Seeking Alpha Portfolios

Given this, we can’t project good things from CBRL stock unless we assume it will depart from business as usual. We need a shock unrelated to ongoing fundamentals.

That’s the essence of a special situation.

Investopedia describes it as “an unusual event that …. by definition has little to do with the underlying fundamentals of the stock or any other rationale that investors ordinarily use to select investments.”

That label often applies to things like spinoffs, merger-acquisition or balance-sheet overhaul.

But in writing for Kiplinger last year, Louis Navellier explained how it can apply to transformational business opportunities or changes. (He even included Quanta Services (PWR) as a future-better-than-past transformation.)

I believe CBRL’s brand rejuvenation fits this mold.

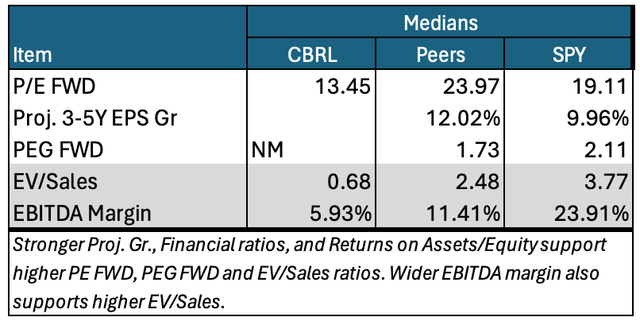

If the market comes to anticipate success, we can expect meaningful improvement in CBRL’s now meager valuations.

Author’s computations and summary from data displayed in Seeking Alpha Portfolios

(Valuation is so tenuous now we don’t even have reliable long-term EPS growth forecasts. Hence, we can’t even compute a PEG FWD.)

On paper, situations can be exciting… assuming transformations succeed.

But for CBRL, this is a time for restrained enthusiasm and critical thinking.

We need that because of how difficult this path can be. To see that, we need look no further than Coca-Cola (KO).

Readers who came of age by 1985 probably remember the mess Coca-Cola, a premier brand-based marketing powerhouse, made with “New Coke.”

Rival PepsiCo (PEP) gained market share against Coca Cola during the 1970s and into the early 1980s.

Independent taste testers often preferred Pepsi. Coca Cola’s internal blind taste tests confirmed that.

So, Coca Cola altered its formula.

It had previously tweaked it a bit without any fanfare. But in 1985, then-C.E.O. Roberto Goizueta went for a public splash.

He boldly introduced New Coke, with what he said was a “smoother, rounder, yet bolder—a more harmonious flavor.”

Members of the press thought New Coke tased a lot like Pepsi. That would hardly be a Coca-Cola marketing triumph.

It went worse among the public. Coca-Cola wound up fielding 8,000 angry phone calls per day.

Finally, on July 11, 1985, just 79 days after new Coke was launched, the company apologized to its customers and launched Coca-Cola Classic. That rose to become the number one soft drink.

It was rebranded Coca-Cola II in 1990 and abandoned altogether in 2002. So today, the Coca-Cola you see is the pre-1985 Coca-Cola.

Fortunately for Coca-Cola, it had the size, stature and fundamental strength to recover from that spectacular screwup (and some might say, come out ahead in the end).

It’s not as if Coca-Cola went into the episode blind. New Coke was backed by 190,000 taste tests.

But as Christopher Klein wrote for History.com, “[n]ever did its market research testers ask subjects how they would feel if the new formula replaced the old one.”

Lesson learned: Emotion can trump objective merit.

McDonald’s (MCD) and Wendy’s (WEN) likewise show the power of brand attachment versus fact.

Consumers often prefer the taste of Wendy’s sandwiches. But at the end of this year’s first quarter, MCD had a 25.63% market share. WEN was way down, at 2.18%.

One burger reviewer put MCD on top, but not because of objective quality. He said:

[O]nly one thing mattered in the end: McDonald’s Quarter Pounder with Cheese tasted like we remembered. A bite of burger and a bite or two of McDonald’s fries brought back real memories of going to McDonald’s as a kid. It tasted familiar but still good enough to keep up with today’s better-burger pace.

CBRL is Stepping Up to the Challenge

Emotion’s role is especially relevant to CBRL.

As I’ll discuss further below, this is not a cookie-cutter casual restaurant chain. It has a very distinct appearance, image, business model, menu and location footprint.

Masino was right to claim CBRL “is one of the most iconic brands in the history of American casual and family dining.”

But iconic alone doesn’t put money in the till. Nor does it add dollars to dividends or the stock price.

In contrast to KO’s New Coke experience, CBRL needs this rejuvenation to succeed. If it fails, the company’s best-case scenario may be long-term mediocrity.

So, let’s turn now to consider the plan. And, of course, the ultimate question for us is what it means for the stock.

For starters, Masino’s credentials give cause for optimism.

Early career stints included stops at Godiva Chocolatier, Coach, J. Crew, and Macy’s, Ms. Masino later held various leadership positions within Starbucks (SBUX).

Before joining CBRL, Masino spent five and half years at Taco Bell.

In the U.S. division, she pushed various business model, technological and culinary changes that spurred eight consecutive quarters of positive comparable store growth.

Then she moved to the international group. There, expansion to more than 1,000 restaurants in 32 countries.

Presumably, other incumbent CBRL folks understand the restaurants. But given the company’s recent performance and Masino’s resume, the bull case would stand on a knowledgable outsider bringing a fresh perspective, CBRL needs.

Where CBRL Was and Is

I suggest starting by taking another look at the image that leads off this article.

Here’s how management introduces the chain.

CBRL IR CBRL IR CBRL IR

Note especially the third paragraph of text on the left side of the image just above. That expresses CBRL’s aspirations.

Clearly, its standard exterior is unique. It’s nothing like Applebee’s, Olive Garden, or any of the countess other casual dining chain restaurants you’ve seen.

And it’s not just on the surface. The feel you get from the exterior continues on the inside.

The dining rooms are country themed, often with local memorabilia.

CBRL IR

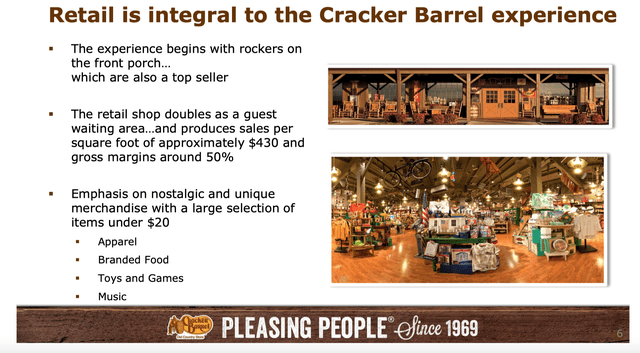

But what really sets CBRL apart are its gift shops. These aren’t little side nooks. They are substantial operations in their own right.

CBRL IR

According to Wikipedia…

The gift shops sell gifts including simple toys representative of the 1950s and 1960s, toy vehicles, puzzles, and woodcrafts. Also sold are country music CDs, DVDs of early classic television, cookbooks, baking mixes, kitchen novelty decor, and early classic brands of candy and snack foods.

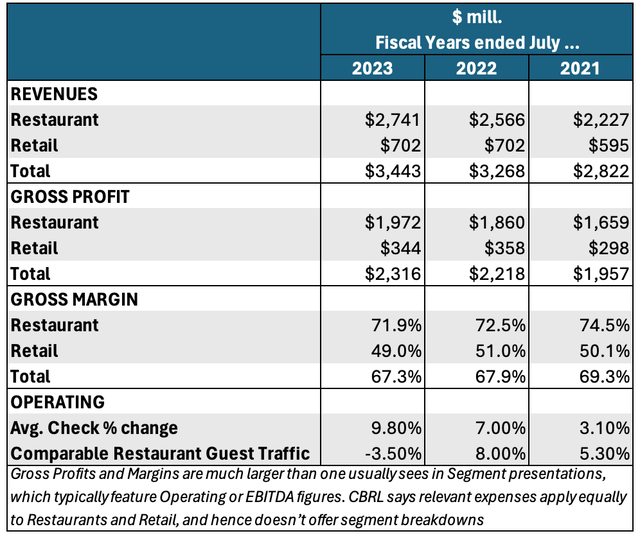

The company considers the shops as being so thoroughly integrated with the restaurant as to refrain from letting its accountants present formal segment breakdowns.

Nevertheless, I can use other information from pages 35-36 of the most recent 10K filing to cobble together my own informal segment breakdown.

Author’s summary of data from CBRL 2023 10K pages 35-36

Before getting into the food, I want to make an important point about the chain’s location footprint.

I covered CBRL back in the 1990s while I was at Value Line. Back then management proudly explained its philosophy of appealing to travelers. It did so by locating most units near Interstate exits.

The executive with whom I regularly (I think the then-CFO, but it was a long time ago so don’t hold me to that) spoke glowingly about the chain’s Interstate exit footprint.

As best as I recall (and this quote is extremely approximate) he said, “many road-trip vacationers actually build their itineraries around where cracker Barrel restaurants are located.”

I raised my eyebrow a bit and asked about plans to expand to other locales, away from the exits. I was curious if the chain wanted to bring in more locals.

I never got a definitive answer. But I suspected in-town locales were a low priority.

Masino didn’t touch on the footprint in her May 16th strategy briefing. But page 9 of the latest 10K says “As of September 13, 2023, approximately 83% of our stores are located along interstate highways. Our remaining stores are located off-interstate or near tourist destinations.”

Especially interesting is this from Wikipedia…

Cracker Barrel is known for the loyalty of its customers, particularly travelers who are likely to spend more at restaurants than locals. From 1977 to 2017, married couple Ray and Wilma Yoder drove a combined total of more than 5 million miles (an average of 342 miles per day) to visit 644 Cracker Barrel locations. When the company opened their 645th restaurant, in Tualatin, Oregon, in August 2017 (on Ray Yoder’s 81st birthday), it flew the Yoders out for the grand opening and presented them with custom aprons and rocking chairs, among other gifts.

Shades of the film “Up in the Air” and the George Clooney character receiving from the airline chief pilot fancy pin-on wings for having accumulated 1 million frequent flier miles! Anyway…

Masino’s characterization of this brand as “iconic” is looking credible.

The food looks like it confirms that.

Here’s a tiny sample of what you’ll find if you go on the Crackerbarrel.com and click on “Eat.” (Your results may vary since the site zeros in on a location near you.)

crackerbarrel.com crackerbarrel.com crackerbarrel.com crackerbarrel.com

This should give you a sense of Masino’s starting point. So, let’s now turn our gaze forward.

CBRL’s Strategic Plan

I like what I heard from the recording of Masino’s May 16th briefing.

But I hate that I have to rely on what I heard and the notes I took.

As with many companies there’s an audio recording available on the CBRL web site. In contrast to typical investor-relations practice, there is no transcript.

Here are the highlights as per my recollection and notes…

- CBRL will “refine and enhance” the brand; it won’t be “reinventing or overhauling” it. The company will work to retain its emotional connection with long-time guests while building such connections with new customers.

- This will be a 10-plus year program.

- CBRL studied CBRL and non-CBRL casual restaurant guests. It wound up with middle ranks in terms of many attributes. But it didn’t lead in any of them.

- CBRL’s menu must appeal to current tastes while remaining authentically CBRL. It has been and will continue introducing many new items. Initial tests have been encouraging and new menu items will gradually roll out to more units.

- The company will also work to optimize pricing. It will raise them in some cases. In other instances, prices will be cut.

- Masino acknowledged that the store design and atmosphere relied “a little too much on what was perceived to be the timeless nature of our concept.”

- The company is pursuing pilot remodels. These involve new color palettes, different lighting, and more comfortable seating. CBRL aims for a “brighter and lighter” look.

- The company will continue to refurbish deliberately and carefully based on testing.

- In 2025 CBRL will debut a smaller prototype having the same number of seats.

- The retail operation will update its “treasure hunt experience. It will work with other brands and introduce “shops within shops”. It will also work to rationalize its many SKUs.

- The company wants to enhance to-go service and off-premises delivery.

On the May 30th earnings call, Masino reported on some early experience with the program.

- CBRL saw “solid improvements across the metrics that are most highly correlated with same-store sales growth.”

- Hourly turnover improved by 10 percentage points year to year.

- The key speed metric improved by about 8%.

- The “off-premises missing item scores improved by 18%.”

- “The average skill level for the key positions of cook and server increased by 3%.”

- CBRL’s Google star rating rose from 4.1 to 4.2.

I like all that.

I’m still wondering whether CBRL will work harder to attract more locals. But I especially appreciate Masino’s sensitivity to the specialness of the CBRL brand and her determination to not mess that up.

Clearly, she’s a pro who understands the lessons of New Coke and the appeal of meh-tasting McDonald’s.

But she’s also attuned to the food and nuts-and-bolts of the overall customer experience.

The question for us is how long we should continue to watch and wait before buying in — to the program and the stock.

I’ll address that after touching upon some obvious risks.

Risks

We can put this together from what’s already been discussed.

With CBRL’s long-tenure as a good equity income play having vaporized, we need a new investment case for the stock.

Ex the brand rejuvenation, CBRL is likely to continue underperforming its peers.

The risk is that the brand rejuvenation may not succeed.

This is more than a formal boilerplate-type risk such as lawyers make managements shove into 10K documents. The New Coke example shows how real this risk is.

What to do About CBRL Stock

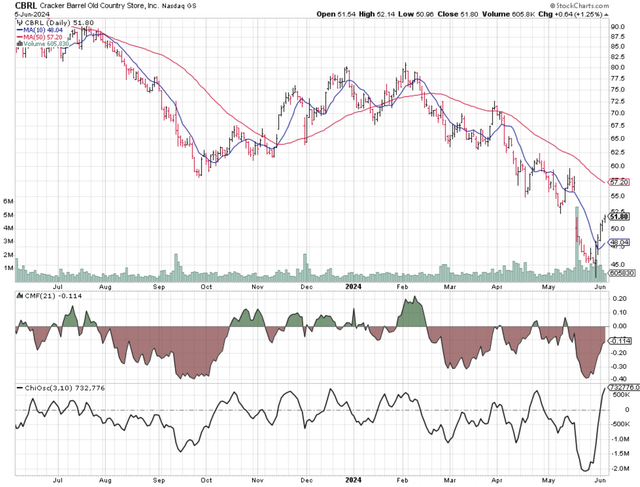

The price chart shows the Street going through the critical thinking phase regarding CBRL’s brand rejuvenation.

StockCharts.com

The Chaikin Money Flow (CMF) and Chaikin Oscillator (CO) indicators both measure which party to trades is more motivated. CMF does it for institutional investors. CO does it for the market in general.

This is valuable information. Buyers being more motivated than sellers exerts upward pressure on stock prices, and vice versa.

We see, from the CO, that buyers in the overall market are taking stakes. That probably reflects optimism about the rejuvenation.

We see, too, how the stock price bounced off its post-dividend cut bottom. That’s pointing the

10-day exponential moving average (EMA) upward.

Those are noteworthy positives.

But the CMF indicator remains quite bad. That suggests institutions aren’t enthusiastic.

Perhaps they’re as peeved as I am by the absence of a May 16th transcript. And maybe they, too, are wondering about whether CBRL will stretch beyond its travelers-Interstate tradition. (Masino’s talk about digital and off-premises may be pointing that way.)

We’ll see.

Decades ago, I may not have cared. I might have simply said the big guys are wrong.

But today, institutional trading dominates the market. So, there’s something to be said for might (measured by dollars committed) makes right.

The generalized tendency toward buying definitely prevents me from saying Sell.

I’m tempted to stay Neutral until the 10-day EMA crosses above the 50-day EMA, or the CMF shows more improvement toward, or perhaps moving beyond, neutrality.

But I see the 10-day EMA and the CMF are already moving in the right direction. I recall, too, how well the stock reacted to Masino’s May 30th update and progress report. It jumped 6% that day.

So I’m going to speculate here…

As I’ve said before, my investment stance depends mainly on whether I think a stock will be better than, in line with, or worse than market.

Here’s how I apply that to the Seeking Alpha rating system:

- “Strong Buy” means I see the stock as being better than the market and I’m bullish about the direction of the market.

- “Buy” means I see the stock as being better than the market but am not confident about the market’s near-term direction.

- “Hold” means I see the stock as moving in line with the market.

- “Sell” means I see the stock as being worse than the market but am not confident about the market’s near-term direction.

- “Strong Sell” means I see the stock as being worse than the market and I’m bearish about the direction of the market.

Based on this scale, I’m rating CBRL as a Special Situation “Buy.”

Read the full article here