Introduction

As I have dedicated a portion of my investment portfolio to fixed income, I am still looking for additional exposure to preferred equity. As the interest rates on the financial markets will move down, the price of fixed rate preferred shares will go up (assuming the creditworthiness of the issuer remains unchanged). I sold my preferred shares in Sunstone Hotel Investors, Inc. (NYSE:SHO) a few months ago on a temporary price spike, but I am wondering if I should re-establish a long position.

A look at the Q1 results and the expectations for this year

When looking at preferred shares, I focus on two elements: the preferred dividend coverage ratio and the asset coverage ratio. In other words, “how safe are the preferred dividends” and “how safe is the preferred equity?”

SHO Investor Relations

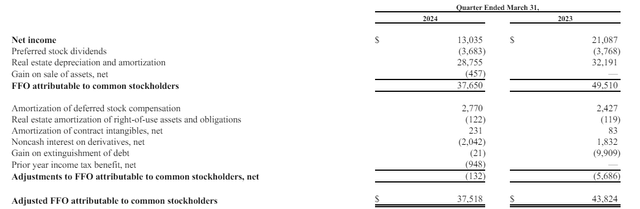

In the first quarter of this year, Sunstone Hotel Investors reported a net income of $13M but as the net profit of a REIT is relatively meaningless, I wanted to see the FFO and AFFO performance of Sunstone. As you can see below, the total FFO attributable to the common shareholders was $37.7M and after making small adjustments, the AFFO was just $0.1M lower at $37.5M.

SHO Investor Relations

Based on the average share count of 202.6M shares in the first quarter, the AFFO per share was approximately $0.18. That is a decrease compared to the $0.21 in the first quarter of 2023 and 2024 will be relatively weak in general.

That’s because the portfolio is undergoing a redevelopment plan, and Sunstone plans to spend $135-155M on capital expenditures. The majority of the impact will be felt in the next few quarters, but these investments should pay off handsomely in 2025. Short-term pain to unlock a long-term gain, indeed, as Sunstone is aiming for a$20-22M EBITDA lift in 2025.

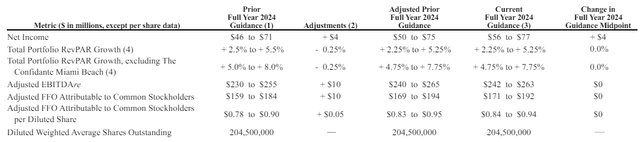

Looking at the full-year guidance (shown below), Sunstone expects a total AFFO of $171-192M, which should result in an AFFO per share of $0.84-0.94. This includes the impact of the remodeling of a few assets.

SHO Investor Relations

Considering the AFFO of $182M (the midpoint of the current guidance) already includes the $14.7M in annualized preferred dividends, the AFFO before preferred dividends is approximately $197M and the preferred dividend payout ratio is just under 8%. This excludes the impact of capital expenditures this year.

How does this impact the preferred equity?

There are currently two series of preferred shares outstanding and as explained in my previous article;

The H-series are trading with (NYSE:SHO.PR.H) as the ticker symbol and offer a 6.125% preferred dividend for a total of $1.53125 per year, while the I-Series are trading with (NYSE:SHO.PR.I) as the ticker symbol offering a 5.7% preferred dividend for a payment of $1.425 per year. Both issues are cumulative and can be called by Sunstone from May 2026 (SHO.PR.H) and July 2026 (SHO.PR.I) on.

As both preferred shares rank equal, it all comes down to buying the one that has the highest yield (as I think the risk for the preferreds to be called is negligible). That’s also why looking at the current yield makes more sense than the yield to call as I think a call is pretty unlikely.

Seeking Alpha

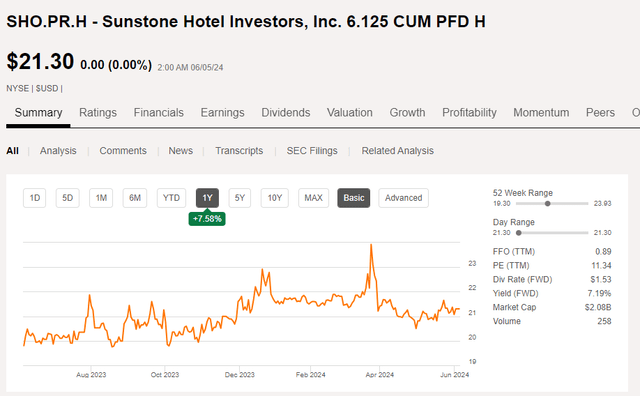

Using Thursday’s closing prices, the H-shares are trading at $21.30 while the I-shares trade at $20.24 for a yield of, respectively, 7.2% and 7.04%. This means that based on the current share prices, the Series H appear to be the better choice due to the higher preferred dividend yield.

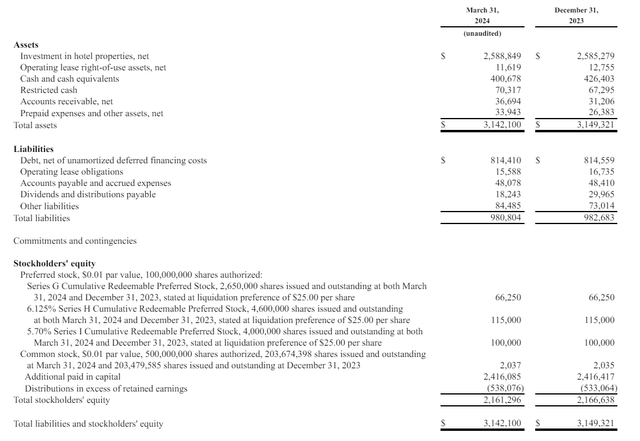

The balance sheet still looks healthy. As you can see below, the REIT has just $980M in total liabilities, while it had access to $471M in cash and restricted cash. Ignoring the restricted cash, the net debt position was just $414M, representing less than 20% of the total $2.59B in assets (which already include an accumulated depreciation of $1.16B).

SHO Investor Relations

There will be a dent in the cash position in the REIT’s next quarterly update, as Sunstone recently acquired the Hyatt Regency San Antonio Riverwalk for $230M. But as this represents a multiple of just 11.1 times the estimated 2024 EBITDA and 12.5 times the NOI, this acquisition will be accretive going forward.

Investment thesis

I sold both series of preferred shares in March of this year, when the Series I was trading above $21/share and the Series H were trading above $23/share. As the Series H is currently trading at just $21.30, the yield has substantially improved compared to the price point I sold my position at.

While Sunstone Hotel Investors definitely doesn’t offer the highest yield in the space, I do think it offers one of the safest preferred dividend yields given the very low LTV ratio in its portfolio. I am giving the preferred shares another serious look and if I re-establish a long position, it will be a position in the series with the highest yield.

Read the full article here