US stocks suffered a mini correction in April. The dip was hardly anything to write home about, just 6.3% on the Vanguard Total Stock Market Index Fund ETF (NYSEARCA:VTI).

I had a hold rating on the fund at the start of Q2, anticipating a pullback as earnings season approached and considering that inflation indicators were turning a bit less sanguine. Moreover, with US large caps having reached about 20 times forward earnings estimates back then, equities were priced rather close to perfection.

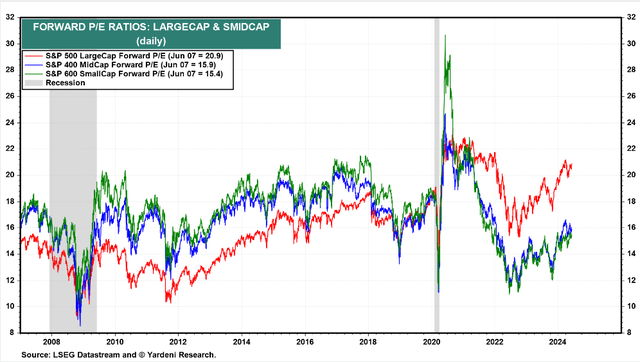

US Equity Valuations: Large Caps 21x Earnings, SMIDs 15-16x

Yardeni Research

I am upgrading VTI from a hold to a buy with seasonal trends now more bullish and with particularly encouraging price action possible ahead given the 4-year presidential election cycle. Fundamentally, earnings growth outperformed expectations during the recent Q1 reporting season too.

Key risks include unknowns about what the Fed may do next and a continued high valuation. Let’s embark on a macro tour of charts that should offer both fundamental and technical clues as to where VTI may go as the summer stretch gets underway and why I am now bullish.

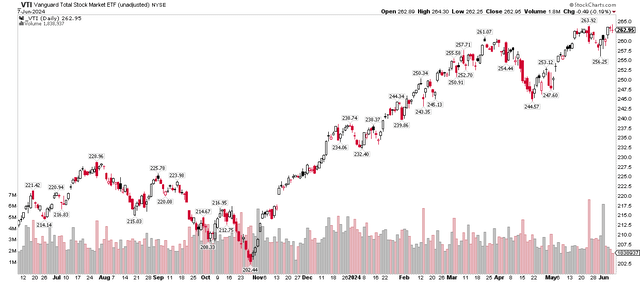

VTI: Near Record Highs Following the Early-Q2 Dip

StockCharts.com

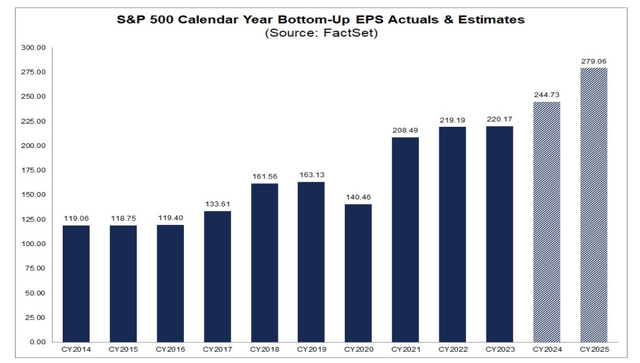

Let’s start with earnings. This is perhaps the biggest bullish factor investors must recognize today. Normally, EPS estimates for the S&P 500 retreat as a year unfolds, but we haven’t seen that in 2024. In fact, there has been a slight upward bias in the per-share earnings outlook in recent weeks. We can thank mega-cap tech for the earnings optimism.

As it stands, analysts expect $245 of current-year operating EPS and $279 in out-year per-share earnings for the S&P 500. Go out to 2026, and the consensus is above $310.

S&P 500 Earnings Estimates Have Inched Up

FactSet

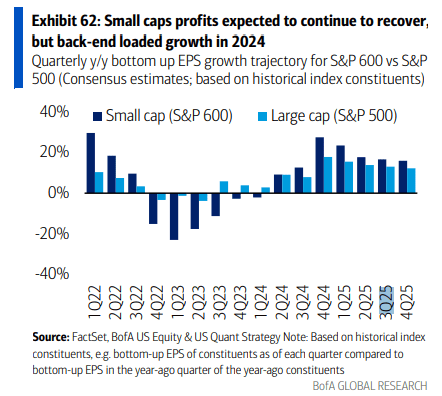

What’s interesting, though, is that profit growth may not be confined just to the biggest of big US companies for very long. US small- and mid-cap stocks are expected to see EPS growth in excess of the S&P 500 over the back half of 2024.

BofA notes that the S&P SmallCap 600 earnings growth rate should eclipse that of the SPX in the quarters. I see this is an upside risk few are taking seriously, let alone pricing into the total US stock market today.

Small-Cap EPS Growth Seen Rising Big in 2H24

BofA Global Research

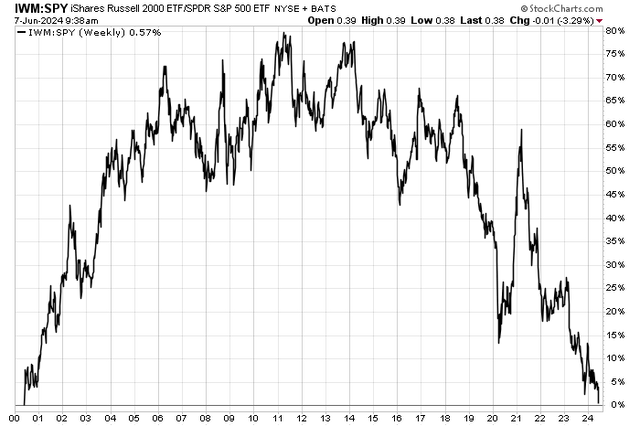

Price action is not lying, however. We’ve seen downright dreadful breadth in markets. Last week on X, I noted that the iShares Russell 2000 ETF (IWM) had reached its lowest relative levels to the S&P 500 ETF (SPY) since its inception in May 2000.

Amid the boom in AI and the raging bull market in chip stocks, money has continued to pour into megacaps, leaving small caps in the dust. I would like to see improved price action away from the Magnificent Seven to help support the case for a broader rally, so this is a risk as well.

US Small Caps Fall to Fresh 24-Year Lows Compared With Large Caps

StockCharts.com

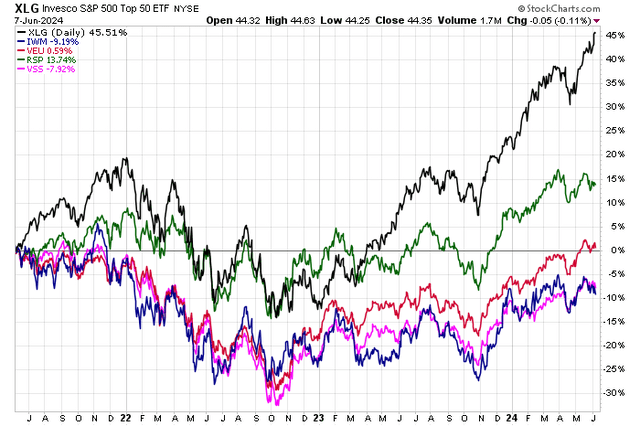

Just how pronounced has the large-cap US rally been? Well, the Russell 2000 is now in year three of its bear market, still close to 20% under its all-time high notched in November 2021. We can stretch the timeframe back a bit further, too.

On a three-year zoom, the Invesco S&P 500 Top 50 ETF (XLG) is up 45. Compare that to lackluster performance numbers in the S&P 500 Equal Weight ETF (RSP), which is up just 14% since June 2021. US small caps, meanwhile, are -9% (total return) in that time, the Vanguard FTSE All-World ex-US Index Fund ETF (VEU) is just fractionally positive, and foreign small caps are down 8%.

All the while, the CPI is up 17% on a real-time basis. So, the bull market has clearly been driven by US blue chips and pretty much nothing else.

US Megacap Dominance: XLG Sports Big Alpha Last 3 Years

StockCharts.com

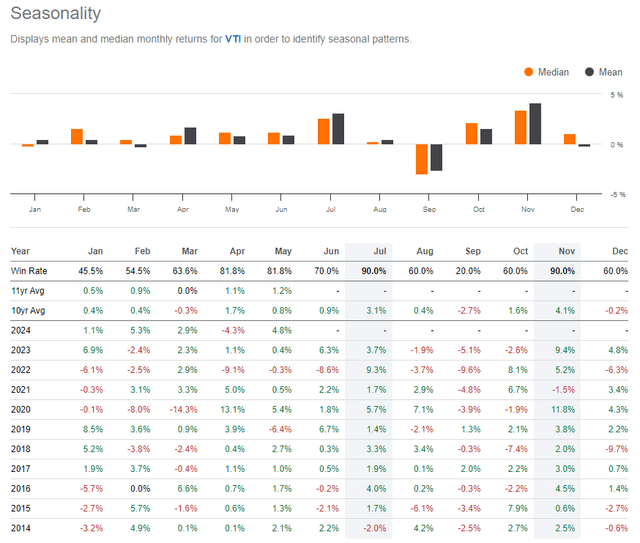

But after the April equity drawdown and an impressive earnings season, VTI looks poised for more gains heading into the summer. I noticed that June and July, and even into early August, is typically a great time to be long and overweight.

According to Seeking Alpha’s seasonality data, June has averaged a 0.9% gain in the past 10 years, up 70% of the time. July has been even more bullish with a typical rise of 3.1% and a strong 90% positivity rate.

VTI: Bullish Seasonal Stretch June-Early August

Seeking Alpha

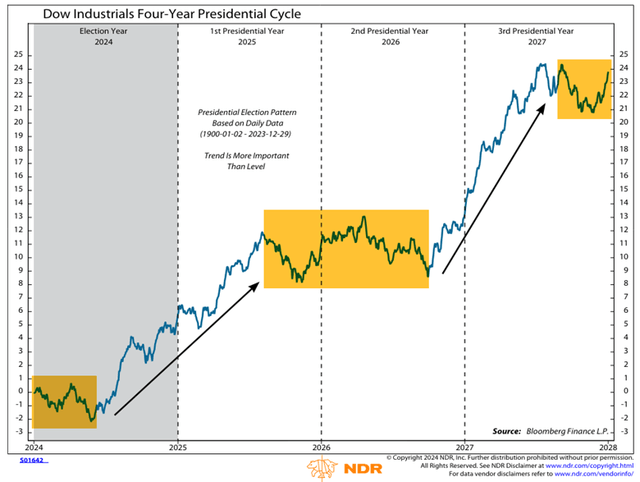

Let’s now zoom out to view where things stand in the vaunted Presidential Election Cycle. Ned Davis Research pointed out last week that right now is just about the optimal time to be aggressive in a long US stock allocation. Mid-year of the election year through the second quarter of the post-election year is the strongest period in the cycle in data from 1900 through 2023 for the Dow Jones Industrial Average.

And while VTI trades at a historically high earnings multiple, one-year forward returns usually have little to do with the current P/E, so calling a top simply on the 20x P/E is not a sound premise.

Strong Historical Trends Based on the Presidential Cycle

NDR

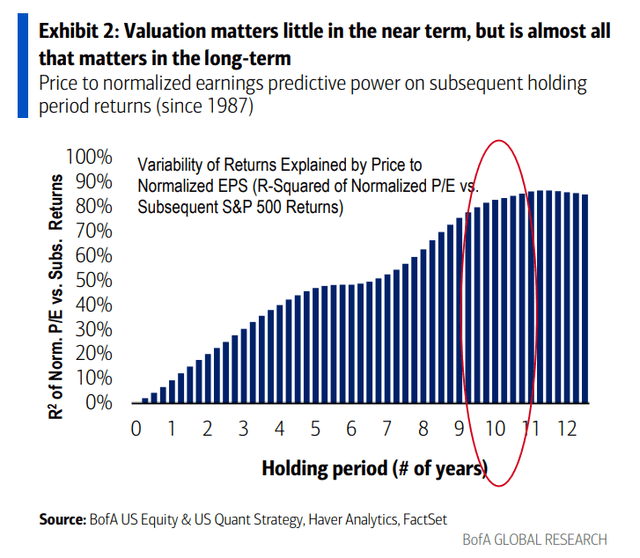

Valuation Has Just A Minor Influence on Performance in the Short Term

BofA Global Research

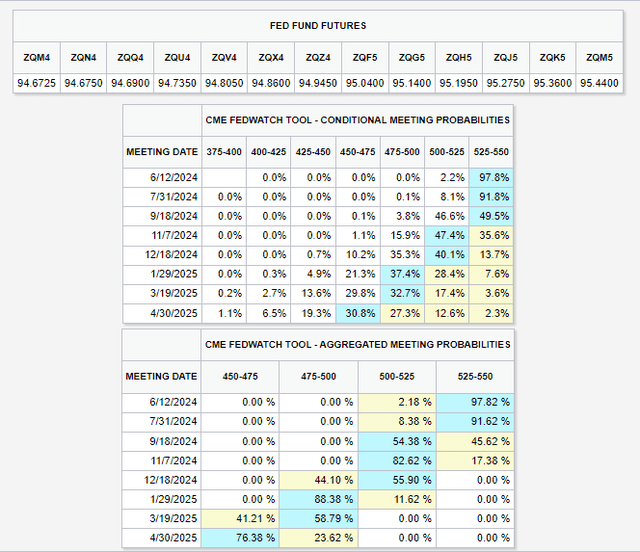

Finally, let’s check in on expectations for rate cuts by the Federal Reserve. Following last Friday’s robust May employment report, which showed a strong 272,000 jobs gain, significantly above economists’ expectations, the chance of the first quarter-point ease happening anytime soon diminished. As it stands, there’s just an 8% probability of a July cut and about a 50/50 chance of an ease ahead of the US general election.

We might have to wait until December for the first cut if healthy employment trends persist and if PCE inflation remains above the Fed’s 2% target. We will get a CPI update this Wednesday right before the Fed’s interest rate decision at 2 p.m. ET.

Chair Powell will have the May CPI report in hand the night before, so Wednesday afternoon’s press conference will be particularly interesting to see how the Fed chief sees monetary policy unfolding in the coming months.

27 Basis Points of Cuts Priced Into 2024

CME FedWatch Tool

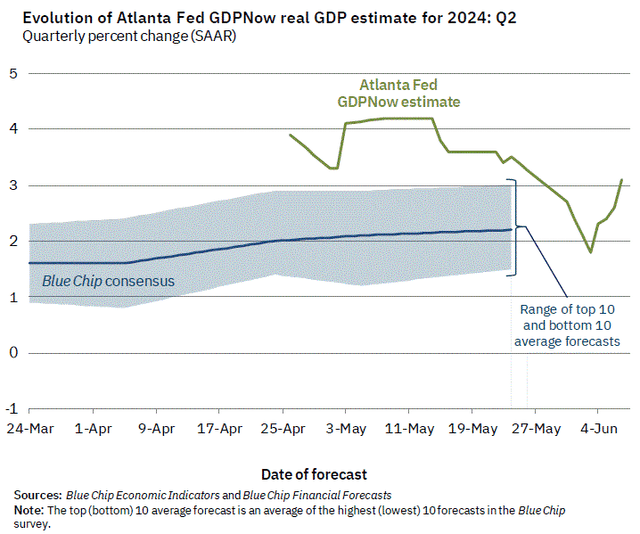

Atlanta Fed GDPNow Jumps Back Above 3% for Q2

Atlanta Federal Reserve

The Bottom Line

I am upgrading VTI from a hold to a buy. We indeed got an April swoon in stocks that I had expected, but the bulls quickly regained control of the total US stock market. A strong earnings season and generally favorable trends in macro data with leadership from big-cap tech helped lift equities.

While VTI continues to trade at about 20x forward operating earnings estimates, I see positive seasonal trends amid a healthy macro backdrop.

Read the full article here