OTC Markets (OTCQX:OTCM) is interesting stock to take a moment and consider, if only because this is the company that chiefly makes “over the counter” stock trading possible.

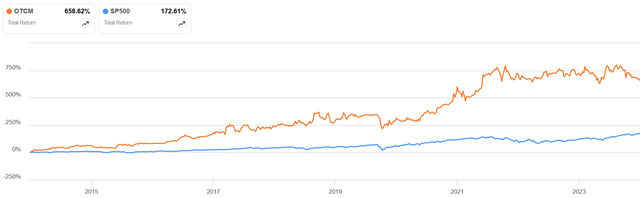

OTCM vs. S&P 500 Total Returns (Seeking Alpha)

Over the past decade, it’s also proved to be a great investment too, vastly outperforming the market. Yet, earnings have slowed down in recent years, and it’s worth considering if the current price reflects another future of growth. Personally, I think the price isn’t quite right and have rated it a Hold.

Financial History

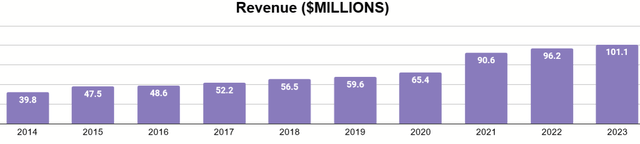

The growth of the stock during the time I quoted above time tracks the growth of the underlying business.

Author’s display of 10K data

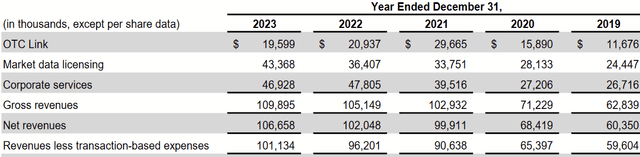

From 2014 to 2023, annual revenues more than doubled from $39.8M to $101.1M.

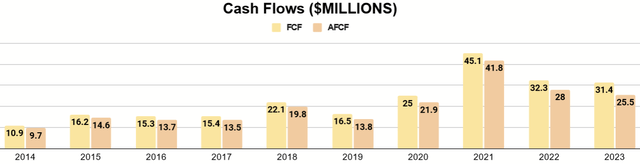

Author’s display of 10K data

Looking at the impact to free cash flow, this is similarly reflected, with more bumps. I also included an adjusted FCF, taking into account stock-based compensation, which is historically near-equal to cash spent on buybacks and (as such) represents an effective cash expense.

Author’s display of 10K data

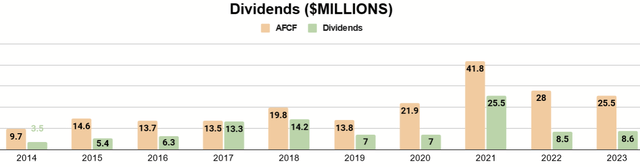

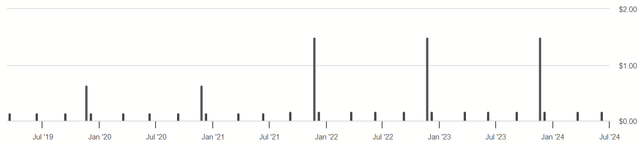

This growing cash flow has allowed much of OTCM’s value to be returned to shareholders by way of dividends, but we can see that that is also a lumpy figure. Importantly, even after the bull market of 2021 subsided, AFCF stands above pre-pandemic levels.

Dividend History (Seeking Alpha)

For individual shares, this has been realized by four small quarterly distributions, along with a large special dividend declared once per year. Where the quarterly dividend has steadily increased, the special dividend varies depending on preferences in capital allocation for the year.

Business Model

Let’s talk about how the company makes this money by running the OTC market (which includes stocks and many other securities). First, let’s review its three subsidiaries:

- OTC Link, LLC

- OTC Markets Group International Ltd

- Edgar Online LLC

OTC Link is a FINRA member broker-dealer that manages trading activity for OTC issues in the U.S. International functions in a similar manner for outside the U.S. Edgar Online, acquired in 2022, provides market data and information about OTC securities.

Across these subsidiaries, OTCM reports its operations in three segments:

- OTC Link (typically ~20% of gross revenues)

- Market Data Licensing (~40% of gross revenues)

- Corporate Services (~40% of gross revenues)

Revenue Breakdown History (2023 Annual Report)

In their 2023 Annual Report (pg. 45), OTCM reported that about 85% of gross revenues were subscription-based, while about 15% were transaction-based. Transaction-based expenses, which they also incur, are resolved to their final revenue tally, indicating that subscriptions are the dominant source of cash flow for this business.

OTC Link

Revenues from this segment come from monthly subscriptions to OTC ATS and transaction-based fees for using OTC ECN. Both their ATS and ECN complement each other allowing subscribers (who are other registered broker-dealers) to receive quotes, negotiate trades with counterparties, and execute orders.

Market Data Licensing

This segment licenses its market data through subscription to other broker-deals, as well as many other customers, which OTCM describes as professional and non-professional. The former group more steadily grows, but non-professional subscriptions to this service tend to change, based on activity in the market among retail investors. In 2023, they reported a 6% rise in professional revenues and a 27% dip in non-professional revenues.

Corporate Services

Revenue comes from the fees public companies pay to have their securities included on OTCM’s three markets:

- OTCQX (Best Market)

- OTCQB (Venture Market)

- Pink Sheets (Open Market)

Inclusion in these markets requires the issuer to meet certain standards, with OTCQX having the highest-quality issuers, meeting standards set by OTCM. (Humorously, this is where their own shares trade.) Pink Sheets either meet no standards or do not apply to meet those of OTCQX and OTCQB and considered the market with the lowest-quality issuers.

Overall, I don’t think OTCM is a very complex business. It basically does what NYSE, NASDAQ, and their foreign equivalents don’t do. It provides trading services for the securities of minor issuers, and it leverages that position to provide curated market data to customers who can make more informed trades and investments with it.

Future Outlook

OTCM basically is the over-the-counter market. Thus, what helps or hurts the business is going to be based on what happens in this arena specifically.

Competition

I am not sure we can say the company truly competes with major exchanges. Their financial history certainly doesn’t show them sacrificing margin to compete.

While OTC issuers aspire to be listed on a national exchange, this is also a selling point for inclusion on OTCM’s markets, making them a natural stepping stone to NYSE or NASDAQ. Similarly, if a company falls off NYSE or NASDAQ, due to a decline in share price or regulatory snafus, OTCM provides a second home for their securities.

Where there might be competition is with the market data service, which could be made available from a wide variety of sources and driven by better technology. This is the only truly competitive threat that stood out to me in their risk factors, and it’s not one we could pin on any particular entity.

OTC Cycles

Since they have the OTC market under lock and key, the real question is what outside forces could affect the demand for their subscriptions. Many of them are on monthly or quarterly bases, and this means they could be cancelled easily and potentially not renewed until a lot of time has passed.

OTC Link Trends (2023 Annual Report)

Seen above, OTC Link’s subscribers have been steady and growing. This is unsurprising, given their focus is broker-dealers. If OTCM is the place to be for OTC trading, any broker-dealer that wants to provide good service needs to join and stay.

OTC Market Securities (2023 Annual Report)

Yet, OTC Link is a small piece of the revenues. Corporate services, meanwhile, is subject to whatever hurts their issuer customers. CEO Cromwell Coulson spoke to this during Q1 earnings:

In the corporate services business, our OTCQX annual renewal percentage dropped slightly from prior years, leading to a lower number of companies on OTCQX at the start of the year. An increase in new OTCQX sales during the quarter presents a positive short-term trend, similar to other public venture and small-cap markets. OTCQB has seen a number of financially stressed smaller companies unable to maintain compliance, and therefore, dropped from the market.

OTCM is supposed to be the easier hurdle than a national exchange in terms of standards, and therefore these customers have somewhat of a heightened risk of not only falling of their market but never returning because financial distress can mean they go out of business. Coulson also provided more remarks to this effect during Q&A:

…smaller companies are struggling on exchanges and we’re seeing de-listings across those as they run to the end of their story ramp. And I think that’s a really important thing for capitalism. You listen to the Canadian exchanges talk about venture markets, and they’ll say, 95% of the companies don’t make it. But it’s a really important piece for the 5% that do.

So not only is the death of an account expected, Coulson views it as the nature of the game. This means there can be cycles in the world of OTC issuers dying off, with new ones formed afterward.

Market Data User History (2023 Annual Report)

Similarly, for Market Data, non-professional users were over 28K during the bull market of 2021 but fell to almost a third of that once the fun was over. Professional users grow incrementally (again, financial services want to have tools for their customers).

Thus, both the Corporate Services and Market Data segments will be exposed to these cycles and affect cash flows.

Seasonality

One thing I wanted to highlight is that the cash flows seem to be subject to seasonality each year, with Q1 typically being one of the worst for operating cash flows.

Quarterly Cash Flow History (Seeking Alpha)

I looked for why this might be in the company’s disclosures but didn’t see any particular reason. Whatever the case, zero-ish OCF seems to be normal for Q1, and those results this past quarter do not appear to be cause for alarm. I believe the trend into positive cash flow will occur in the remaining quarters.

International Market

I think the international trading market will be increasingly important here. Coulson indicated such:

The trend towards international trading activity has continued with trading in ADRs in ordinary shares of non-US companies comprising over 80% of dollar volume across our OTCQX, OTCQB and pink markets. Trading these global companies in US market hours is a unique value proposition with dollar volumes growing for both European and Asian-listed issuers.

Trading Volume History (2023 Annual Report)

Annual volume was down from $713.8B in 2021 to $386.4B in 2023.

Volume of Q1 2024 vs. Q1 2023 (Q1 2024 Form 10Q)

Yet, Q1 2024 featured a reversal. As such, not everything that affects OTCM is going be based on what happens with the U.S. market and financial system. Over time, foreign issuers and international broker-dealers may create counter-cyclicality to American macro-trends.

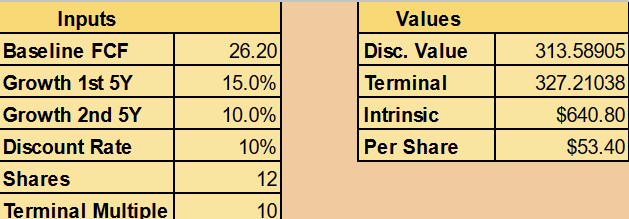

Valuation

To value these shares, I will use a Discounted Cash Flow model, substituting my AFCF for FCF. I will use the following assumptions:

- $26.2M as baseline FCF

- 15% annual growth first 5 years

- 10% the next 5

- Terminal multiple of 10

$26.2M is the average AFCF for the last five years. CAGR of AFCF from 2019 to 2023 was 16.6%, so I’m projecting somewhat slower growth in the next five years and that it will continue to decelerate farther into the decade, with a multiple of 10 to reflect the potentially weaker growth prospects.

Author’s calculation

Priced for a 10% discount rate (typical return of a broad market index), that suggests OTCM’s intrinsic value is about $640M, about $53 per share, close to the current share price.

For my part, the semi-cyclical nature of its subscription revenues makes me want a better discount. Consider how relatively flat the shares are since the bull run of 2021.

Seeking Alpha

Moreover, I’m not aware of any catalysts to grow FCF more ambitiously. With much of their capital used for dividends over the years, combined with the absence of leverage on their balance sheet, it seems to me that management isn’t chasing dead-obvious growth either.

Conclusion

OTC Markets Groups is a fine business that provides a key role in the capital markets with an over-the-counter platform and services it provides. As their CEO said, it is a domain where capitalism is tested, and there will always be a need for it. For that reason, I expect they are here to stay.

While I think cash flows will average toward growth, I also recognize there is cyclicality and perhaps room for a better discount and to limit potential downside. Otherwise, it seems to me like the shares, invested for the long-term, make for a reasonable Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here