PPL Corporation (NYSE:PPL) has been a laggard over the past year, rising just 4%. Headwinds from higher rates and slow growth have weighed on its valuation. I last covered PPL in December, rating shares a “hold,” as I felt its geographic footprint created some downside risk to earnings targets. Since this analysis, shares have returned 9%, well below the market’s 19% return. While this performance has been consistent with my ~8% expectations, given the relative underperformance, one could argue a “sell” rating may have been justified. With updated financials and this underperformance, now is a good time to revisit PPL.

Seeking Alpha

In the company’s first quarter reported on May 1st, it earned $0.54 in adjusted EPS, up from $0.48 last year. GAAP EPS was $0.42, and there were $0.12 of one-time items related to Rhode Island integration costs. Revenue fell by 5% to $2.3 billion. However, this was due to the fact that energy purchase costs fell by $214 million. Natural gas prices have been lower than last year, but PPL does not take commodity risk, instead passing this on to customers. Lower energy costs reduce revenue but reduce expenses equally.

Because it does not take energy risk, I prefer to look at volume activity. Pennsylvania volumes rose 2%; Kentucky rose a strong 7.6%. Now, this winter was cooler than last year, and that can cause variations in demand for utilities. PPL attributed about $0.03 of its higher earnings to weather. Excluding this, earnings rose about 6%.

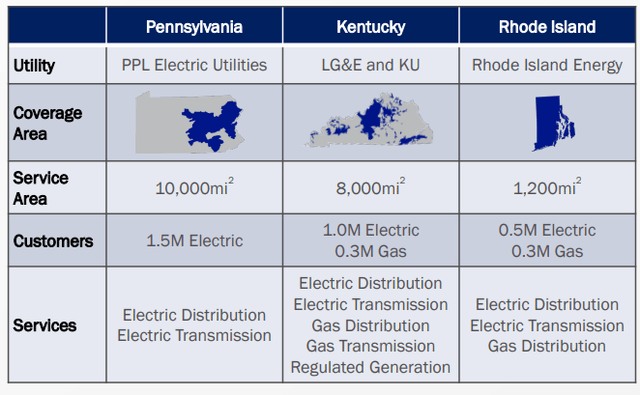

This was still a solid result, as PPL has benefitted from a growing rate base – the value on which it earns a regulator-approved rate of return. As a reminder, PPL has a $25.4 billion rate base across 3.6 million customers. 47% of its rate base is in KY, 38% in PA, and 15% in Rhode Island.

PPL

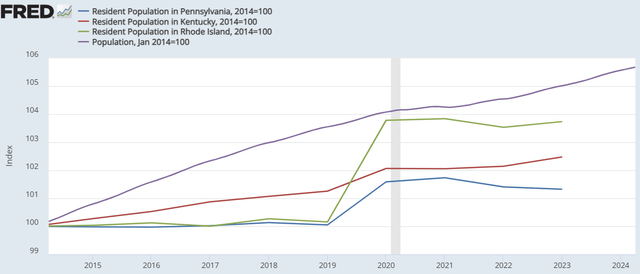

I have generally viewed this geographic exposure cautiously. A growing population and economy are important for a utility’s growth. A rising population means more potential customers for a utility. Additionally, the cost of the rate base is spread across its customer base. A rising customer base reduces the per-customer costs, allowing a utility to grow more easily without raising rates, which regulators obviously prefer.

These states are generally slow growing. From a high level, the Northeast and Appalachian regions have seen population out-migration toward the Sun Belt, given lower tax burdens, more economic opportunity, and warmer weather. As you can see below, over the past 10 years, PA, RI, and KY have each grown more slowly than the US population as a whole. I would also note that RI’s growth was primarily due to the census causing a shift in its estimated population. In other words, RI did not grow that fast in 2020, rather its population was likely higher than reported across 2014-2019. The same is true of PA, to a smaller degree.

St. Louis Federal Reserve

Now, a utility is essentially beholden to local population trends. It cannot exactly pick up and move its electric poles and infrastructure and move to faster growing areas. I would note PPL’s regions are still growing; however, they are growing more slowly than the country as a whole. As such, we are likely to see PPL’s electricity demand be relatively low over time, normalizing for shifts in weather, etc.

For a utility to grow, increasing its rate base is essential. PPL aims to do that with a $14.3 billion capital plan through 2027. Based on this spending, it expects to grow its rate base by 6.3% per year. Its rate base is set to grow 6.3% this year, up from 5.6% in 2023. To achieve this, it will spend $3.1 billion of 2024 capital programs, with a peak in 2025 at $3.8 billion and then $3.7 billion thereafter. 22% of the capital plan is focused on RI, as it diversifies somewhat away from PA & KY.

Importantly, 65% of its capital spending should have contemporaneous recovery, as work is being done to improve energy efficiency, update outdated infrastructure, and increase the reliability of its network. Because it is immediately able to add this spending back into its rate base, there is less risk, rather than the 35% that it will recover months later or via multiyear rate cases in front regulators.

As PPL is engaged in this large capital program, one clear positive is its solid balance sheet. PPL believes no equity issuance is needed to fund its plan, given relatively low debt levels, with funds from operations/debt likely to stay in the 16-18% area. Now, in Q1, PPL generated $707 million of operating cash flow, excluding working capital. Its dividend costs $177 million, leaving it with $530 million of retained cash flow. For the full year, PPL should generate about $2.2 billion of retained cash flow, which it can use for cap-ex.

In Q1, it spent just $596 million in cap-ex. Given its $3.1 billion 2024 budget, I expect cap-ex to ramp to $800-900 million per quarter. PPL can fund about 70% of its cap-ex spending this year with cash and rely on debt financing for the remaining 30%. In 2025-2027, debt funding will likely make up about 40% of capital spending. To ensure financial sustainability and to avoid overburdening balance sheets, I generally view less than 50% debt financing as ideal for utility cap-ex spending, and so PPL is well positioned within this range.

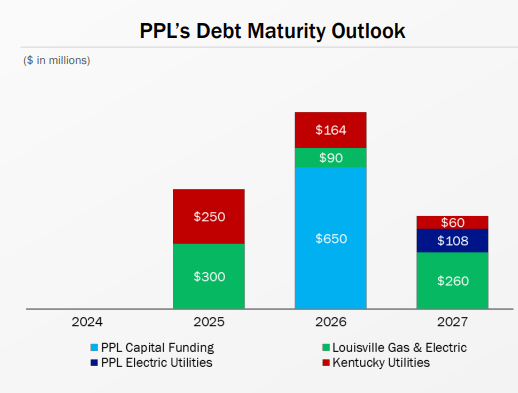

Still, we will see debt levels rise. Higher debt and increased rates caused interest expense to rise 9% to $179 million in Q1. Importantly, of its $15.9 billion of debt, 80% matures five years or later. This reduces the need to roll over low-yielding debt in today’s high interest rate environment. As you can see below, it has limited 2024 maturities, with a more material $900 million due next year that it will need to roll over. This will lead to somewhat higher borrowing costs in all likelihood.

PPL

Now, PPL may have timed its 2025 ramp in cap-ex spending quite well. Its net debt issuance needs are likely to be higher in 2025-2027 than they are in 2024, given a higher level of capital investment. While the exact timing of Federal Reserve rate cuts is unknowable, I do expect 1-2 cuts this year and likely ongoing reductions thereafter. While inflation is persisting above 2% for longer, it is gradually converging towards target. This should mean that PPL’s financing costs will be lower in 2025-2027 than they would be if it had to issue more debt today.

Alongside Q1 results, PPL affirmed its $1.63-$1.75 earnings forecast for this year, as well as its 6-8% earnings and dividend growth target through 2027. In March, it increased its dividend to $0.2575 from $0.24, a 7% increase, in keeping with this target. PPL earned $1.60 in 2023 on an adjusted basis, so the midpoint of guidance represents 5.6% growth. After a solid Q1, where weather is of outsized performance, I view guidance as credible, as there should be limited volatility in results, given its rate base is largely set, and there is limited incremental debt issuance needed in calendar 2024.

One area of focus will be improved efficiency. PPL aims to cut operating and maintenance spending by 2.5% per year. Management believes it achieved $75 million in 2023 cost cuts, ahead of its $50-60 million target. However, there was 12% growth in operating and maintenance expense in Q1. This is largely tied to integration costs, which it views as one-time. These can persist for longer, and I do view this target as somewhat ambitious, particularly in what remains an above-average inflation environment.

Given most of its capital spending is immediately recovered, I do believe PPL should be able to achieve most if not all of its 6.3% medium-term rate base growth. I see upside risk to this forecast as limited given the slower growth in its regions. However, as before, I still see some risk to its EPS grow targets. Even if the Fed does begin to reduce rates as expected, its weighted average cost of debt is likely to rise, due to gradual refinancings and increased debt issuance needs in 2025 to 2027. Increased expenses will offset some of this rate base growth and make it difficult for EPS to grow faster than the rate base. Additionally, given slow population growth, the 35% of its cap-ex spending that takes longer to recover could face some risk.

As such, I continue to view 5-6% growth as more likely than 7-8%. Indeed, I would note that even with less 2024 debt needs and a 6.3% rate base increase, it expects just 5.6% EPS growth, which speaks to the challenges of growing EPS more quickly than the rate base. To be clear, I view the risk to PPL as one of growth being a bit slower, not of the business facing decline. Accordingly, its 3.7% dividend yield is very secure.

With growth in the 5-6% area, I continue to see PPL positioned for about 8-9.5% long-term returns. Now, PPL is unlikely to keep up in a large bull market, as we have seen, but I would not expect the pace of underperformance to continue. Shares do not have quite enough upside to merit a “buy,” where I target 10+% returns, and I prefer better geographically positioned utilities like Atmos (ATO). Still, I view PPL as a hold, and a suitable name for income oriented investors, seeking a secure dividend with moderate growth potential over time.

Read the full article here