Introduction

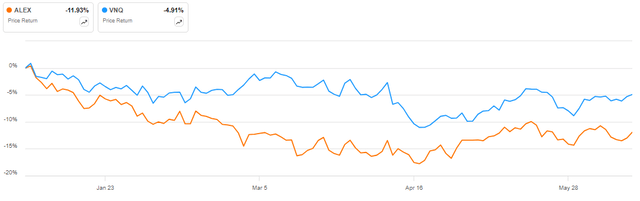

Alexander & Baldwin (NYSE:ALEX) has underperformed the Vanguard Real Estate Index Fund ETF (VNQ) so far in 2024, as the shares are down in the low-double digits against a 5% decline in the benchmark ETF:

ALEX vs VNQ in 2024 (Seeking Alpha)

I think this has pushed the REIT to an undervalued level as the stock offers a high single-digit return potential with really modest leverage. In fact, leverage is so low you may consider it a negative in light of the potential coming shift in Fed monetary policy and the expected boost for the real estate sector as a whole.

Company Overview

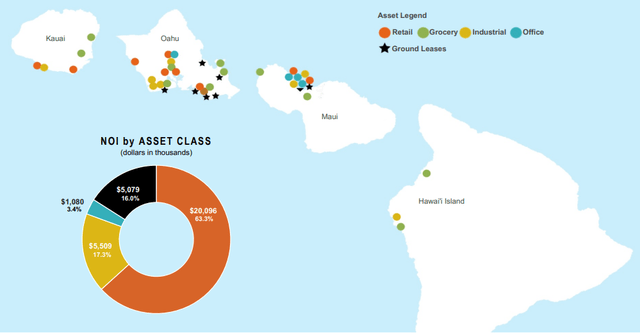

You can access all company results here. Alexander & Baldwin is a diversified REIT with heavy retail exposure and a geographic presence exclusively in the state of Hawaii. From an asset class perspective, Retail accounts for 63.3% of net operating income, or NOI, followed by Industrial at 17.3%, Ground Leases at 16%, and a small 3.4% Office exposure:

Portfolio overview (Alexander & Baldwin Q1 2024 Investor Supplement)

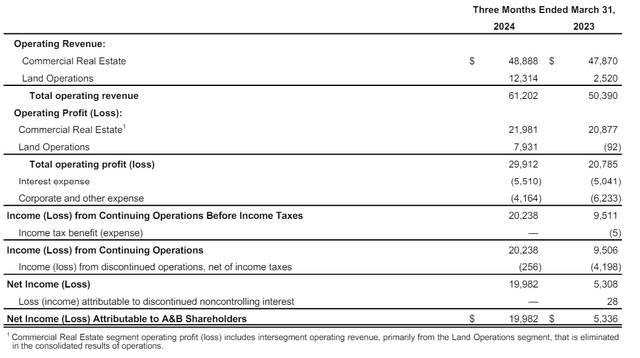

The company reports results in two main segments, Commercial Real Estate (its core segment) and Land Operations (legacy assets):

Segment results (Alexander & Baldwin Q1 2024 Investor Supplement)

Operational Overview

Alexander & Baldwin reported an adjusted FFO of $0.35/share, up 54.5% Y/Y, driven in large part by land sales in the Land Operations segment. Same-store NOI growth was 4.1% Y/Y, boosted by strong demand for retail and industrial properties.

Occupancy stood at 94% at the end of Q1 2024, up 0.1% Y/Y. The retail portfolio was 93.2% occupied, down 0.4% Y/Y, while the industrial portfolio boasted an occupancy of 96.8%, up 1.6% Y/Y.

2024 Outlook

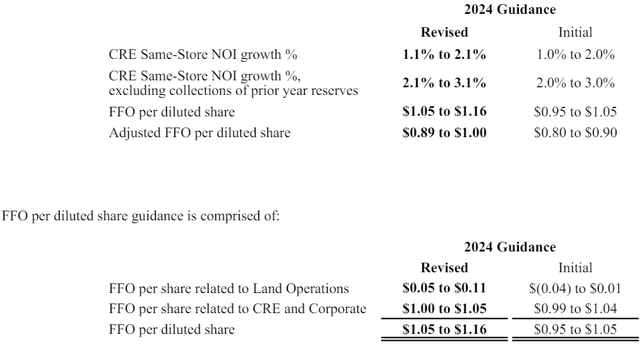

Alexander & Baldwin boosted its full-year outlook to reflect the strong results in Land Operations, as well as the above-expectations NOI growth so far in 2024. As a result, Same-store NOI growth is seen at about 1.6% Y/Y, or 2.6% if you exclude the collection of prior year reserves:

Updated 2024 Outlook (Alexander & Baldwin Q1 2024 Earnings Release)

I believe the 2.6% NOI growth is more indicative of the underlying trend observed at the company. Adjusted FFO is seen at about $0.95/share, up 9% Y/Y.

Capital Structure

Alexander & Baldwin ended Q1 2024 with a net debt of $442 million, implying that net debt accounts for just 27% of enterprise value, which is one of the lowest leverage levels you can find in the REIT industry. The weighted average cost of debt is only 4.43%, but the company is facing a maturity wall in 2024 and 2025 – some 51% of debt matures in these two years. As a result, I expect the average cost of debt to creep up as funding available on the company’s revolver currently carries an interest of 6.48%.

Market-Implied Cap Rate

I anticipate Alexander & Baldwin to generate some $124 million in same-store NOI in 2024 which against an enterprise value of $1.64 billion represents a market cap rate of 7.6%, which is quite attractive given the strong occupancy and NOI growth in the low single digits.

The company reports recurring maintenance capex, running at about $14 million annually, representing a 0.9% drag on the 7.6% market cap rate.

From a management overhead standpoint, administrative expenses were $7 million in 2023, a further 0.5% impact on the 7.6% market cap rate, but an efficient level of management overhead nevertheless.

Land Portfolio

What differentiates Alexander & Baldwin is its substantial 142-acre ground lease portfolio, which generated $5.1 million in NOI in Q1 2024. These results are recorded in the Commercial Real Estate segment. Furthermore, the company has a legacy land portfolio recorded in the Land Operations segment. After the 300-acre sale in Q1 2024, the remaining legacy portfolio encompasses some 3,405 acres. As discussed on the conference call, when the remaining legacy land portfolio will be sold is hard to forecast.

Risks

While the maturity structure of the company’s debts is very short-term, Alexander & Baldwin has ample capacity on its revolving credit facility and will easily address upcoming maturities. In fact, the company currently has a net debt-to-EBITDA of just 3.8, while its target is generally in the 5 to 6 times range. Given the expectations for Federal Reserve rate cuts starting in the next few months (futures pricing indicates a Fed funds rate of 4.00-4.25% in July 2025), Alexander & Baldwin may well have missed an opportunity to buy additional assets at the bottom of the real estate cycle. As such, we may even argue that the capital structure of the company is too conservative in light of monetary policy expectations and the potential for additional liquidity from land sales down the line.

The other risk I would highlight is that the REIT invests exclusively in Hawaii, which diminishes diversification and exposes investors to the economic dynamics of one state alone. This risk, however, is easily eliminated if you hold Alexander & Baldwin as part of a larger REIT portfolio.

Conclusion

Alexander & Baldwin recorded a strong start to 2024, with NOI growth running above full-year expectations and an opportunistic land sale boosting liquidity at the company. With a high single-digit return potential and very low leverage, I think the company is an excellent pick for conservative investors. But if you are looking for a REIT to really benefit from the coming shift in Fed policy, this is not the company for you. As always, whether to invest depends on your idiosyncratic risk preference.

Thank you for reading.

Read the full article here