The Federal Reserve gave an important update about its rate policy on Wednesday and communicated to the market that it expects to only cut the federal fund rate once in FY 2024 as inflation, although moderating, remains above the Fed’s 2% annual inflation goal. This has huge implications for Blackstone Secured Lending (NYSE:BXSL) which is heavily invested in variable rate debt and makes a superior value proposition due to its very low non-accrual percentage. Blackstone Secured Lending is my ‘best bet’ in the BDC sector right now, which relates in part to the company’s variable rate loan investment strategy, but also due to its excellent balance sheet quality!

Previous rating

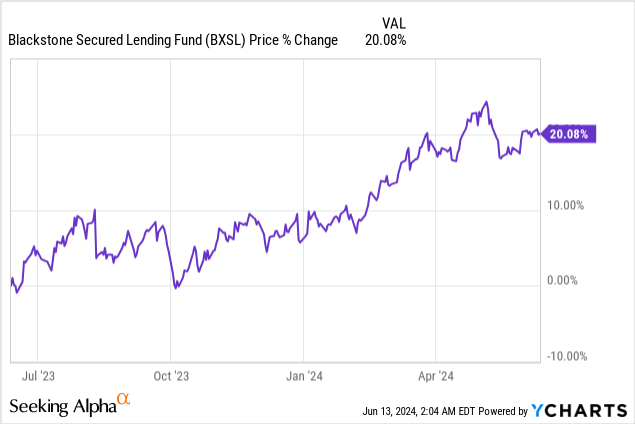

I rated shares of Blackstone Secured Lending a Buy — Boost Your Cash Flow With This 10% Yield — in the first week of April, in large part because the BDC had impressive credit quality. Since this coverage, shares have increased 2% and the BDC itself has broadly met my expectations (consistent distribution coverage, no deterioration in loan quality).

Now with the Federal Reserve back-tracking from its December 2023 guidance to enact up to three rate cuts, variable rate BDCs with low non-accruals, in my opinion, could become much more attractive for investors that seek recurring dividend income. Although shares of Blackstone Secured Lending are not cheap, I believe BXSL makes a superior value proposition for BDC-focused investors in the updated rate context.

Higher-for-longer rate world set to benefit high-quality BDCs like BXSL

Blackstone Secured Lending’s unique selling proposition is that the BDC is chiefly invested in variable rate loan investments, mostly first liens. With inflation for May being reported at 3.3%, a 0.1% decrease compared to the previous month, and the Federal Reserve clarifying its stance on interest rates, Blackstone Secured Lending is a top BDC investors should pay attention to, in my opinion.

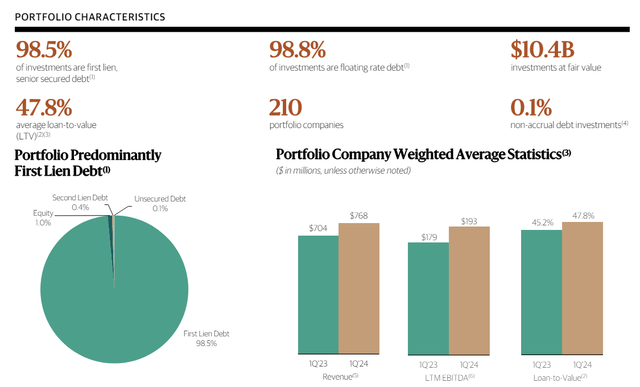

On Wednesday, the Federal Reserve updated the market about its views on the federal fund rate and guided for only one interest rate cut in FY 2024. This is a remarkable departure from the Fed’s earlier stance of intending to pursue up to three rate cuts in December 2023. This higher-for-longer rate world is set to benefit chiefly those BDCs that have a strategic focus on variable rate debt investments, as the odds for sustained net investment income growth have improved. Blackstone Secured Lending’s debt investments were 98.8% variable rate as of the end of the March quarter.

BXSL

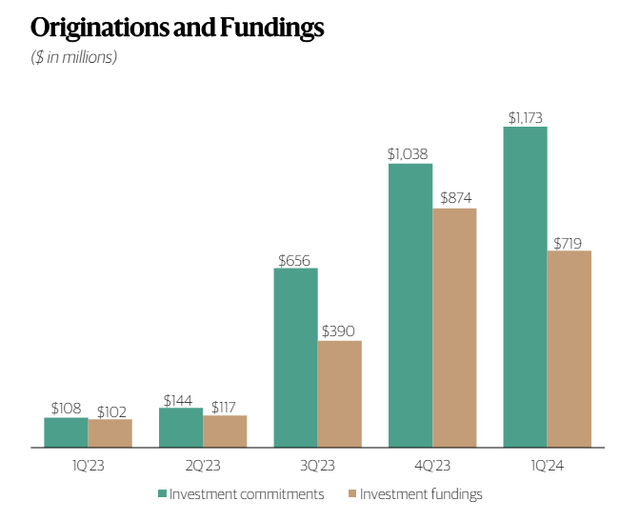

Additionally, the improved rate and NII outlook (from the point of view of a variable rate-positioned BDC) comes at a time when pipeline activity for Blackstone Secured Lending is picking up. In the last quarter, new investment commitments continued to surge to $1.2B, the highest level in at least a year, and Blackstone Secured Lending generated $532M in net funded investments. With a growing investment pipeline, a higher-for-longer rate world and a 99% variable rate portfolio percentage, Blackstone Secured Lending has considerable outperformance potential.

BXSL

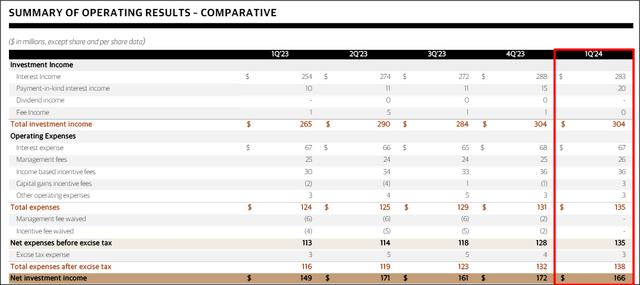

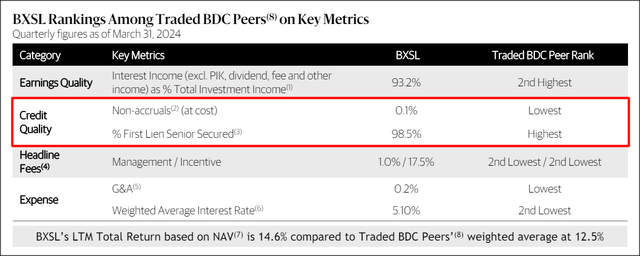

Blackstone Secured Lending generated 93% of its total investment income from interest income in the first-quarter. The BDC’s total investment income increased 15% year over year to $304M, while BXSL’s net investment income gained 11% year over year to $166M. What was remarkable was that the BDC’s quarterly interest expenses remained flat at $67M year over year, meaning Blackstone Secured Lending wholly benefited from higher federal fund rates in the last year.

BXSL

Sector-leading non-accrual percentage adds to superior value proposition

Blackstone Secured Lending’s non-accrual percentage was less than 0.1% at fair value in the most recent (March) quarter which means BXSL leads the sector together with Hercules Capital (HTGC), a BDC that recently achieved record investment results and also had a very low non-accrual percentage in Q1’24. Hercules Capital is by far the most expensive BDC which was the only reason why I down-graded shares after the company’s Q1’24 results. From a performance point of view, however, Hercules Capital is doing an excellent job.

BXSL

Blackstone Secured Lending’s valuation

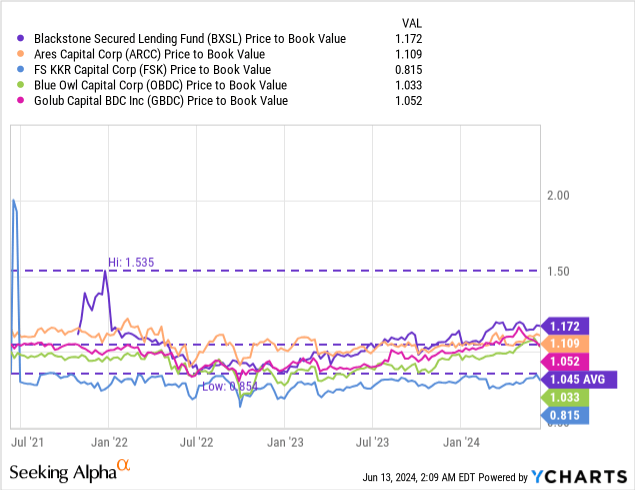

Blackstone Secured Lending is trading at a higher than average premium to net asset value, which traces back to the quality of BXSL’s first lien portfolio. The BDC is currently trading at a price-to-NAV ratio of 1.17X which is way above the industry group P/NAV ratio of 1.04X. The industry group in this case includes the five largest BDCs in the sector including Ares Capital (ARCC), FS KKR Capital (FSK), Blue Owl Capital (OBDC) and Golub Capital BDC (GBDC)… and BXSL.

I believe that BXSL could trade at a 1.25X price-to-NAV ratio based off of the strength in pipeline activity, the double-digit growth in NII as well as the fact that the Federal Reserve just delivered a strong tailwind for BDCs with variable rate investments. The main reason why I think that BXSL could trade at such a high premium is that the BDC has excellent balance sheet quality, meaning almost all of its investments are performing and generating income on a recurring basis. Because of the tailwinds discussed in this article (Fed, NII growth), I am more optimistic about the possibility for multiplier expansion compared to the time my initial work on BXSL was published. In March, I was of the opinion that BXSL could trade at 1.20X given the BDC’s portfolio and coverage strength. This multiplier has now almost been reached, and I believe Blackstone Secured Lending has continual revaluation potential.

A 1.25X price-to-NAV ratio calculates to a fair value of $33.60 per-share (up from $32.20 per-share), implying 7% upside. Shares currently pay investors a 10% yield as well and the Q1’24 distribution coverage ratio was 1.13X (for past distribution coverage ratios see my initial work on BXSL earlier this year).

Risks with Blackstone Secured Lending

The Federal Reserve, in my opinion, has provided a lot of earnings and NII visibility for Blackstone Secured Lending this week. Specifically, I believe that the combination of a sector-leading non-accrual ratio with prolonged NII tailwinds could make BXSL an outperformance candidate for dividend investors.

A higher-for-longer rate environment may pose a challenge to the BDC in case it were to more recklessly originate variable rate loans in order to benefit from the cyclically-inflated federal fund rate. If the company’s portfolio quality were to suffer as a result, BXSL could potentially create NII headwinds and NAV risks for itself. Given that the BDC has a strong track record in non-accruals, I believe this is unlikely.

If Blackstone Secured Lending were to see an increase in the non-accrual percentage, however, or the Federal Reserve were to cut rates more drastically in FY 2025, then I would likely change my rating on BXSL.

Closing thoughts

Wednesday’s Fed statement had big implications for the BDC sector and specifically for those BDCs that have strategically allocated investment dollars to high-quality variable rate first liens, like BXSL. Blackstone Secured Lending is leading the sector in terms of balance sheet quality (low non-accrual percentage) which means BXSL could especially benefit from a higher-for-longer rate world. Since the BDC generates NII chiefly from its 98.8% variable rate investments, Blackstone Secured Lending has attractive NII growth prospects. The improved outlook for NII growth paired with above-average investment performance translate into a rating upgrade to strong buy!

Read the full article here