SoFi Technologies (NASDAQ:SOFI) is a very popular stock with Retail investors. Many investors are true believers in the “disruption of banking” narrative. The thesis is that SOFI is developing superior cost-efficient branchless, digital banking solutions that can attract high-value customers (or members as it calls it) and then the flywheel is set in motion where it can cross-sell multiple products to the same client base and enhance the lifetime value of members and in the process deliver superior returns for shareholders.

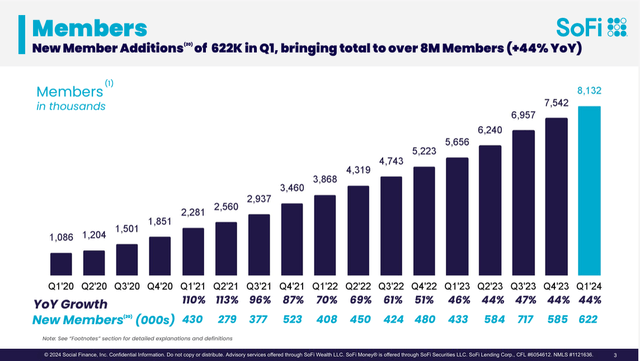

The growth of members has certainly been impressive and is one of the key metrics SOFI discloses in the earnings pack:

SOFI Investor Relations

SOFI also has a Technology division which is comprised of Galileo and Technisys that essentially provides Banking as a Service (BaaS) infrastructure to facilitate client banking and back-end capabilities (such as account setups and funding, direct deposits, payments functionality, etc). Some investors characterize it as the “AWS of Finance” but so far, despite some positive signs of potential contracts with certain large banks, it hasn’t quite lived up to this title.

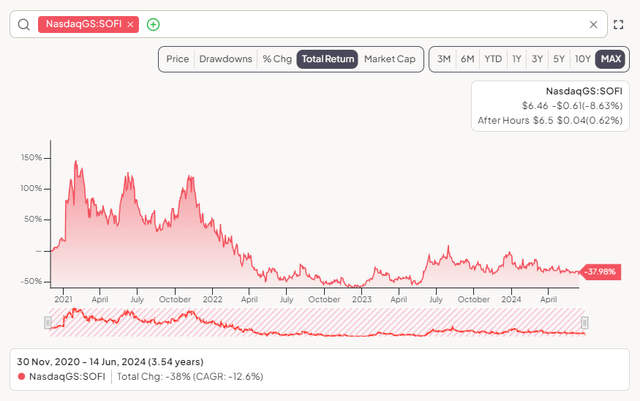

The share price performance since the IPO has been negative despite what appears to be solid progress in executing the SOFI strategy, achieving profitability and strong medium-term guidance for 2026 EPS.

FinChat.io

The “smart money” or the institutional folks, however, are not buying into the SOFI bull narrative. Quite the contrary, many are shorting SOFI as is reflected by the high short interest held in the stock which frequently crosses the 20% threshold. In fact, the smart money is likely to see SOFI as a perfect macro hedge.

I have written in the past several bearish articles on SOFI (for example, this one recommending shorting the stock above $10). In this article, however, I am looking to elaborate on how the stock is likely to be perceived by the institutional players. I will also discuss at what point I am likely to take a long position in the stock.

Why is SOFI a perfect macro hedge?

There is little doubt that if the U.S. economy goes into a hard landing coupled with higher unemployment, consumer-focused banks with a large unsecured book are going to experience materially higher delinquencies. Mr. Market is likely to shoot first and then ask questions later.

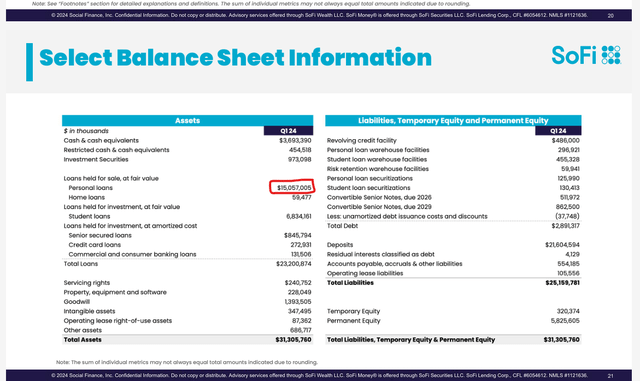

SOFI has almost 70% of its loan book in unsecured personal loans as can be seen below:

SOFI Investors Relations

That is a highly concentrated book but not the end of the story either. SOFI compared to peer banks has disproportionately higher exposure due to what is being perceived as its aggressive accounting practices.

SOFI employs an unusual accounting practice (compared to its banking peers) where it elects held-for-sale accounting designation for its personal loan portfolio. This practically translates to upfronting of profitability from these loans (compared with most peers’ accounting treatment) due to:

- SOFI recognizes fair-market-value (FMV) uplift on day 1 typically of 4% to 5% of the loan assets;

- SOFI also does not provide for future losses as per the CECL methodology employed by most banks.

So comparing apples to apples with peers, on day 1 of originating a personal loan asset, SOFI recognizes a benefit of 11%-12% of asset value compared to peers’ accounting treatment. Since the economic outcome and cash flow are the same, the day 1 “gain” reverses over the life of the asset (i.e. loan losses are recognized as they are incurred and the FMV bleeds back into the P+L over time as an expense). I have explained this in more detail in this article if readers need more context on this.

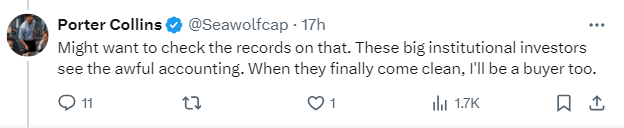

This recent tweet from Colins Porter (Seawolf Capital and known for being portrayed in The Big Short movie) highlights the concerns some professional investors have when it comes to SOFI accounting treatment of personal lending assets.

Colin Porter – Seawolfcap

So What May Happen In A Hard Landing?

The FMV (currently reporting a gain of $607 million) will likely reverse to a large extent or even turn negative. Similarly, the recognition of loan losses will likely be accelerated forward and with a higher loss severity.

In such a scenario, it is not implausible that the share price will plummet. Concerns may also arise about its capital position and that SOFI may need to raise a significant amount of capital to shore up the balance sheet and capital ratios.

The counterargument from the bulls would be that SOFI borrowers have high FICO score on average (in the 740s) and that it has plenty of buffers with a current CET1 ratio of 17%.

While the above counterarguments have some validity, I submit the following:

- In such a scenario, SOFI stock may sell off hard due to uncertainties with respect of FMV and/or the level of reserves needed. Mr. Market tends to shoot first and ask questions later and thus SOFI management may be forced to act by the markets and/or regulators.

- The reported 17% CET1 is somewhat inflated by the abovementioned accounting treatment. Professional investors would adjust that figure for CECL and FMV to reflect a much lower adjusted number. Back-of-the-envelope calculation assuming 6% CECL and reversing $607m of FMV gains yields ~CET1 of 9% and thus arguably too low for such a highly concentrated bet on unsecured personal lending.

Final Thoughts

For some professional investors, shorting SOFI is almost a perfect macro hedge on a consumer recession. SOFI is expensive by traditional metrics of price to tangible book value (TBV) utilized by most bank investors. Currently, SOFI is trading at a >2x multiple of adjusted TBV. Most banks trade at or around 0.7x-1.5x price to tangible book value with some outliers such as JP Morgan (JPM) trading at a premium.

Importantly, in a hard lending scenario, the drawdown in the share price is likely to be significant and there is also an outside risk of further equity dilution. On the flip side, the upside risk is mitigated by the force of gravity exerted by TBV valuation metrics unless of course, SOFI becomes a meme stock.

In the medium to long term, the retail investors may be right and SOFI will successfully execute on the banking disruption model and flourish 5 years from now. Another potential game-changer is the Tech division, if it can grow CAGR at 25%+ for many years then SOFI’s valuation could detach from the gravity force exerted by its TBV.

Near term, however, the dominant narrative for the institutional folks is the risk profile. This is the key reason why the short interest consistently hovers around ~20%.

This is also likely to be the primary reason why SOFI management has slowed down the growth of the personal lending book and raised additional capital recently.

I have been both long and short SOFI in recent years. Currently, I am on the sidelines as I believe downward volatility is likely to manifest as the Fed tries to stick an economic landing (unlikely to succeed in my view). I can envision going long at the right time and valuation. I do not believe now is the right time to rate SOFI as a Buy, hence it is a Hold for me currently.

Read the full article here