The Data Center Investment Thesis Remains Robust In VRT – Thanks To The Growing Market Momentum

We previously covered Modine Manufacturing Company (MOD), discussing its rapid upgrade from a small-cap to medium-cap status within a short span of one year, attributed to its well-diversified offerings across thermal management in commercial vehicles, automotive, and data center markets, along with industrial power generation/ transmission.

For this particular article, we will be looking at Vertiv Holdings (NYSE:VRT) and sharing our findings about the stock, continuing the theme surrounding the data center infrastructure sector.

VRT is a company focusing on the design/ manufacturing/ servicing of digital infrastructure for data centers, communication networks, and commercial/ industrial markets.

The company offers rather well-diversified offerings across power management/ storage, thermal management through chilled-water/ liquid cooling solutions, integrated server rack systems, and operating stacks, one that is particularly critical during the ongoing cloud transition and generative AI boom.

Super Micro Computer, Inc. (SMCI) has already reported an “accelerating need for liquid cooling at new data centers” due to the increased efficiency and reduced energy costs for higher-density computing, compared to traditional air-cooled systems.

Most importantly, VRT has been chosen to support Nvidia’s (NVDA) “next-gen accelerated data centers powered by GB200 NVL72 systems,” building upon their multi-year collaboration, along with Intel’s (INTC) next-gen Gaudi 3 AI accelerators.

Reader must also note that more Big Tech companies have announced intensified cloud investments ahead, including Meta Platforms (META), Microsoft (MSFT), Tesla (TSLA), and Google (GOOG), partly leveraging on NVDA’s AI chips.

The combination of its strategic partnerships and promising market trends further underscore why VRT may continue to report accelerating growth ahead. The same has been observed in its double beat FQ1’24 earnings call, with net sales of $1.63B (+7.2% YoY) and adj EPS of $0.43 (+79.1% YoY).

Much of the top-line tailwinds are attributed to excellent product sales of $1.27B (+7.6% YoY) and SaaS revenues of $368.8M (+10.2% YoY), with the Americas accounting for its top-line at $716.1M (+6.3% YoY) and $208.9M (+9.9% YoY), respectively.

Demand appears to be robust internationally as well, in the APAC region at product sales of $224M (+7.2% YoY) and SaaS revenues of $108.3M (+4% YoY), along with EMEA region at $297.3M (+11.1% YoY) and $84.5M (+8.2% YoY), respectively, with NVDA’s prediction of “Sovereign AI” – “a nation’s capabilities to produce artificial intelligence using its own infrastructure, data, workforce and business networks” likely playing out here.

Much of VRT’s bottom-line improvements are attributed to the increasingly rich gross margins of 34.5% (+2 points YoY) in the latest quarter, as supply chain issues moderate, further aided by the higher ASPs.

The same expansion has been observed in its adj operating margins of 15.1% (+3.6 points YoY), thanks to the improved operating scale/ productivity and relatively stable SG&A expenses of $314M (+1.7% YoY).

As a result of these developments, it is unsurprising that VRT has also raised their FY2024 guidance, with net sales of $7.61B (+11.9% YoY), adj operating margin of 17.5% (+2.2 points YoY), adj EPS of $2.32 (+31% YoY) at the midpoint, implying the management’s confidence to consistently deliver profitable growth ahead.

This is up from the original number of $7.58B (+10.4% YoY), 17.1% (+1.8 points YoY), and $2.23 (+25.9% YoY).

We believe that VRT’s raised guidance is not overly aggressive as well, as observed in the robust backlog growth from $5.52B and a book-to-bill ratio of 1.3x in FQ4’23 (+16.2% YoY), to $6.3B (+14.5% QoQ/ +31.2% YoY) and a ratio of 1.5x in FQ1’24 (compared to 1x in FQ1’23), respectively.

This is on top of the raised FY2024 capex guidance of $200M (+56.3% YoY), attributed to the ramp-up of liquid cooling/ power management manufacturing capacity, compared to the original midpoint guidance of $137.5M (+7.5% YoY), allowing the management to strategically tap into its growing backlog.

As a result of the great insights into VRT’s multi-year performance through 2025 and beyond, it is apparent that NVDA’s commentary of a “new era of computing” in the recent earnings call is not overly aggressive indeed.

Lastly, we believe that the company remains well poised to fund its growth opportunities internally, based on the growing Free Cash Flow generation of $101M (+304% YoY) and richer margin of 6.1% (+4.5 points YoY) in FQ1’24, along with the FY2024 FCF guidance of $825M (+6% YoY) and margins of 10.8% (-0.5 points YoY).

VRT’s Premium Valuations Appear To Be Reasonable, Albeit Carrying Moderate Risks

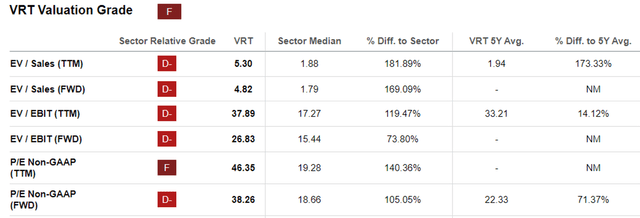

VRT Valuations

Seeking Alpha

As a result of the long-term tailwinds, it appears that the market has temporarily awarded VRT with the premium FWD EV/ EBIT valuations of 26.83x and FWD P/E valuations of 38.26x, compared to the sector median of 15.44x/ 18.66x, respectively.

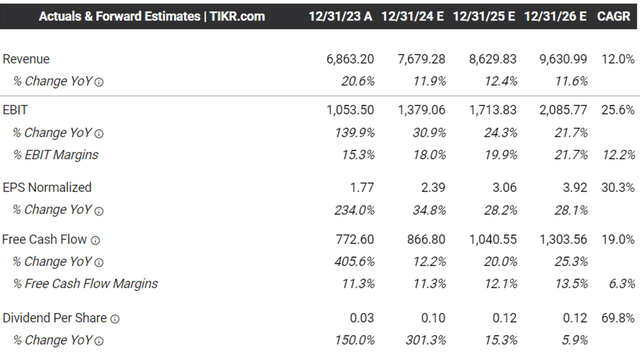

The Consensus Forward Estimates

Tikr Terminal

Perhaps part of the optimism is attributed to VRT’s promising consensus forward estimates, with it expected to generate an accelerated top/ bottom line growth at a CAGR of +12%/ +30.3% through FY2026.

This is compared to the historical top-line growth at a CAGR of +8.2% between FY2016 and FY2023.

The same optimistic valuation has also been notably embedded in other thermal management/ power technology stocks, such as MOD at FWD EV/ EBIT valuations of 18.21x/ FWD P/E valuations of 25.25x, Lennox International Inc. (LII) at 20.84x/ 25.41x, and AAON, Inc. (AAON) at 24.91x/ 32.94x, respectively.

Based on MOD’s projected top/ bottom line growth of +8.4%/ +19.2% through FY2026, LII at +5.8%/ +12.1%, and AAON at +9.5%/ +12.2%, it appears that VRT is reasonably valued given the higher profitable growth projections.

On the other hand, readers must also note that VRT reports a relatively higher net-debt-to-EBITDA ratio of 2.44x in FQ1’24, compared to MOD at 1.36x, LII at 1.51x, and AAON at 0.03x, with the former’s premium valuations likely posing a certain level of risks, despite the debts only maturing in 2027 and 2028.

This is based on the former’s cash/ equivalents of $275.8M (inline YoY), current/ long-term debts of $2.93B (-7.5% YoY), and annualized adj EBITDA of $1.09B in the latest quarter (+28.9 YoY).

While the VRT management has guided lower net leverage ratio of below 2x by FQ3’24, skewing the risk/ reward ratio to the attractive, interested investors may also want to size their portfolios according to their risk appetite.

So, Is VRT Stock A Buy, Sell, or Hold?

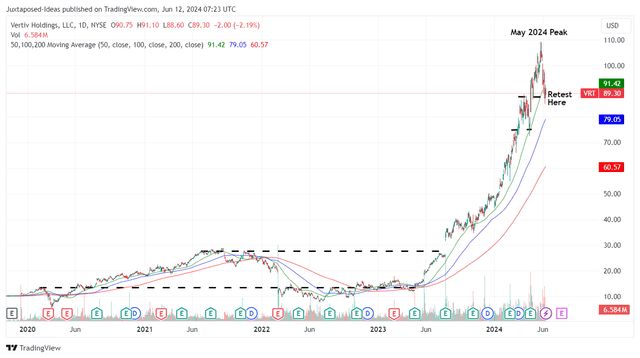

VRT 4Y Stock Price

Trading View

For now, VRT has already charted new peaks in May 2024 while running away from its 100/ 200 day moving averages.

Based on the LTM adj EPS of $1.96 and the FWD P/E valuations of 38.26x, it is apparent that the stock has pulled forward part of its upside potential to our fair value estimates of $74.90.

Then again, there appears to be an excellent upside potential of +67.8% to our long-term price target of $149.90, based on the consensus FY2026 adj EPS estimates of $3.92 and the same FWD P/E valuations of 38.26x.

While minimal, VRT also offers quarterly dividends of $0.025 per share, offering interested investors with a decent income moving forward.

As a result of robust capital appreciation prospects and decent dividend incomes, we are initiating a Buy rating for the stock, though with no specific entry point.

Based on the VRT stock’s movement thus far, it may be prudent to observe for a little longer, since it is currently also retesting its previous support level of $89s. Otherwise, interested investors may consider waiting for a moderate pullback to its previous trading ranges of $75s and $80s, with those levels also nearing our fair value estimates.

At the same time, readers must note that insiders have been unlocking great gains at these inflated levels, with $1.62B of shares already sold within the last twelve months (compared to $77M in the twelve months prior), though well-balanced by the management’s prudent share repurchases of $606.1M over the LTM (+13,675% sequentially) and stable share count of 379.13M in FQ1’24 (-2.5M YoY).

Read the full article here