While investors continue to clamor for more tech exposure, the companies that engaged with natural resources have been left behind. I like that personally because the best trades come from putting money to work in underinvested parts of the marketplace. If you agree, you may want to consider the Fidelity MSCI Materials Index ETF (NYSEARCA:FMAT). This passively managed fund attempts to track the performance of the low-turnover MSCI USA IMI Materials 25/50 Index. With a low expense ratio of just 0.084%, it’s a good proxy, and basket, for broad exposure.

A Look At the Holdings

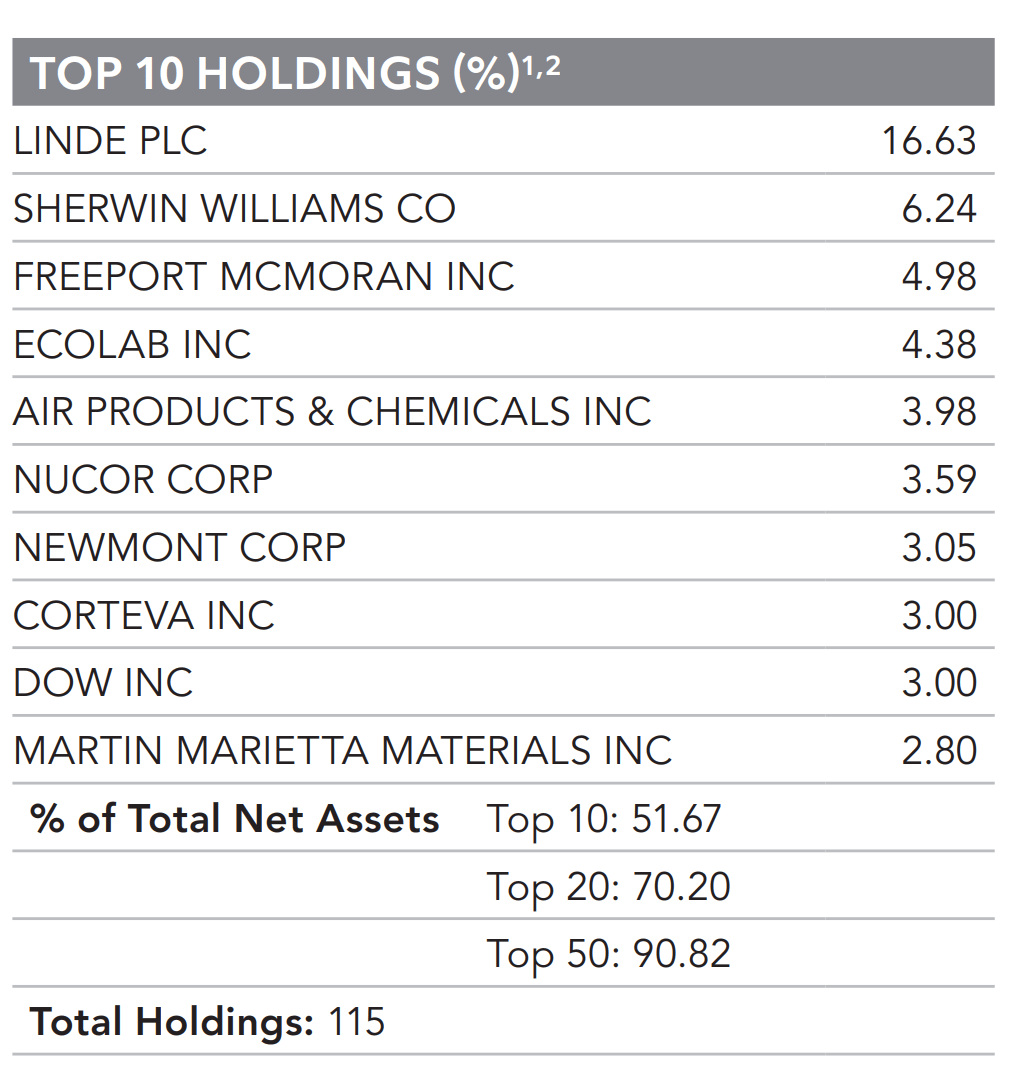

FMAT has about 115 positions, but does have high concentration given that the top 10 holdings make up a little over 50% of the fund.

fidelity.com

The biggest allocation goes to Linde PLC, a multinational industrial gasses and engineering company, with operations from producing atmospheric gasses to designing and constructing plants for the gasification and conversion of coal, natural gas and petrochemicals. The Sherwin-Williams Company comes in second. I’m sure this is a company you’re probably familiar with from the paint and coatings side of your local Home Depot. Coming in at third is mining company Freeport-McMoRan Inc. (FCX). It’s one of the world’s largest producers of copper, gold and molybdenum.

Overall, good representation here, though the fund does appear to have some significant idiosyncratic risk at the top.

Sector Composition and Weightings

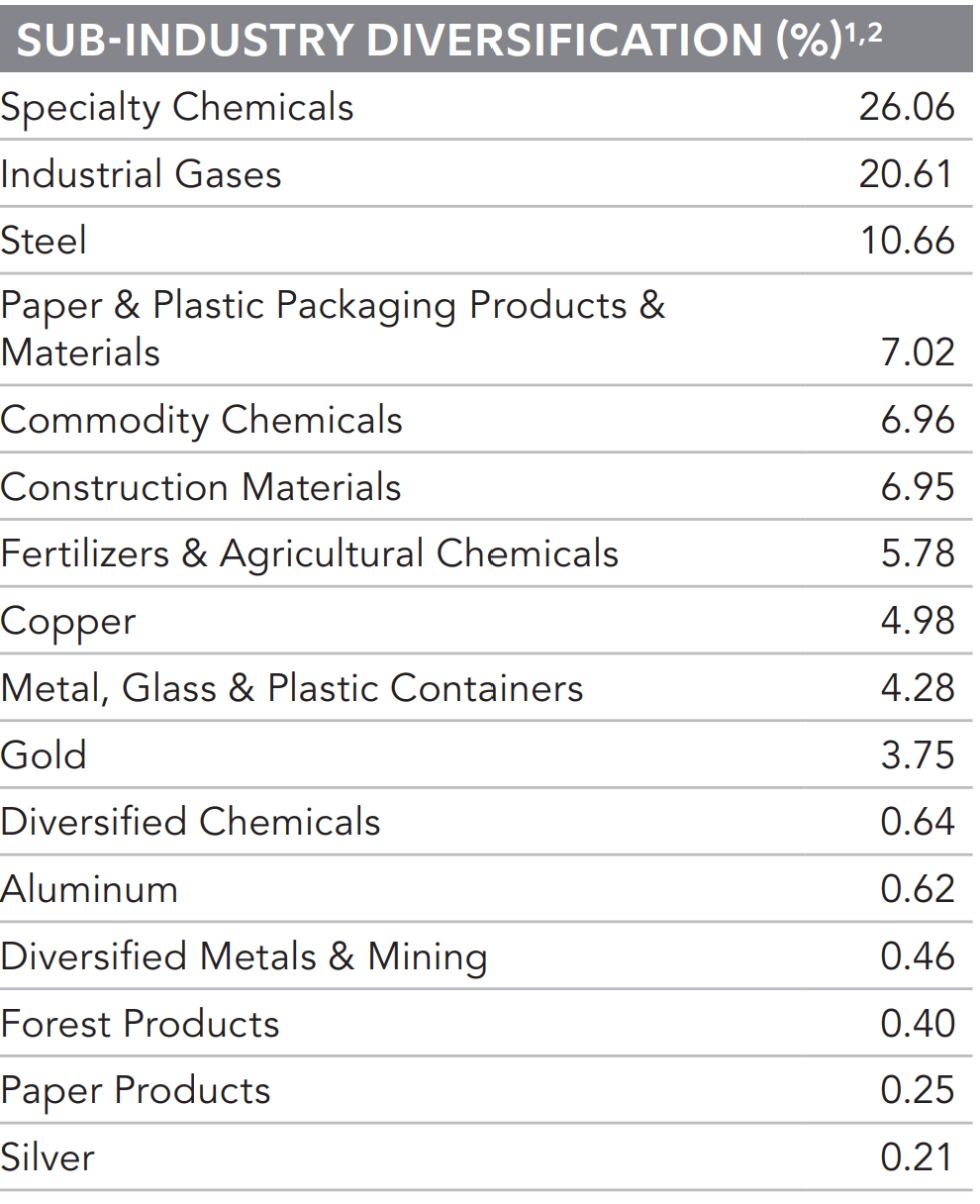

The interesting thing about this as a materials fund is that the largest allocations go to chemicals and gas. Maybe it’s more of a me thing, but when I think of materials, I think of solid commodities like steel and copper. Regardless though, this tracks what you often see in other materials funds as far as industry classifications.

fidelity.com

Peer Comparison: FMAT vs. XLB

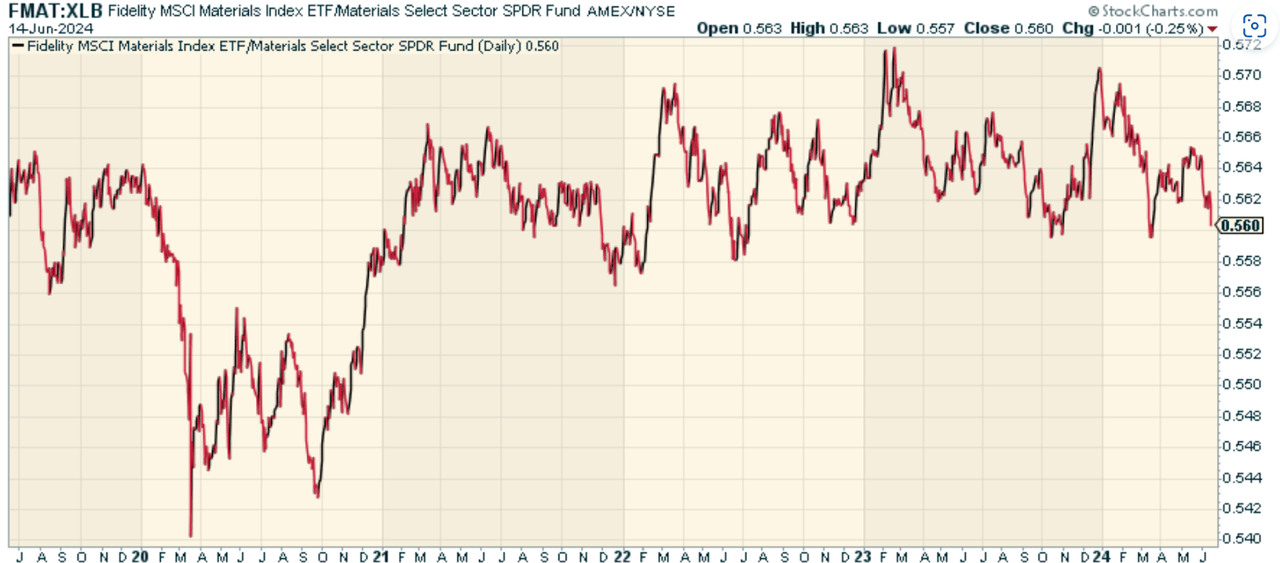

The big dog when it comes to broad investing in the materials sector is the Materials Select Sector SPDR Fund ETF (XLB). That fund has considerably fewer holdings, with just 28 positions. There is a lot of overlap here, with the same top 3 positions in XLB matching those of FMAT, but just with higher weighting. When we look at the price ratio of FMAT to XLB, we find that other than 2020, the two funds have largely stayed in a nice relative range to each other. No clear advantage of choosing one over the other performance-wise here.

stockcharts.com

Pros and Cons

One thing to keep in mind is that the materials sector has traditionally been somewhat cyclical and tends to do well when the economy rebounds. The sector has been lagging over the past year amid recession fears (that never quite come to fruition). As those fears potentially dissipate, the sector could start to perform well as economic growth accelerates. Demand for construction materials and industrial chemicals will likely move up as the economy continues to chug along, which broadly should help with revenue growth.

Separate from near-term dynamics though, over the longer term, the prospects for some of the world’s leading materials stocks are attractive. With strong supply-and-demand fundamentals remaining a major tailwind for commodities more broadly which haven’t participated in the euphoria we’ve seen in US large-cap equity averages.

Having said that, the performance is still not there and relative momentum isn’t that encouraging yet. The main challenge stems from increased interest rates that are still acting with a lag on the broader economy and are starting to directly impact industries reliant on construction and automobile sectors. And while the threat of recession has held back the sector with none yet occurring, the concerns continue to linger and are clearly still impacting investor sentiment when it comes to Materials stocks. I believe there’s opportunity with that, question is how long it takes to pan out.

Conclusion

For those who are bullish on the broader outlook for the economy and expect an economic recovery or expansion, FMAT offers an efficient way to gain exposure to the materials sector. Its broad diversification provides good exposure to cyclical stocks. I do like this part of the marketplace generally because, at some point, investors will favor things over digits and rotate away from Tech. Just be mindful of the concentration risk given how much the top 10 stocks make up of the fund.

Anticipate Crashes, Corrections, and Bear Markets

Anticipate Crashes, Corrections, and Bear Markets

Are you tired of being a passive investor and ready to take control of your financial future? Introducing The Lead-Lag Report, an award-winning research tool designed to give you a competitive edge.

The Lead-Lag Report is your daily source for identifying risk triggers, uncovering high yield ideas, and gaining valuable macro observations. Stay ahead of the game with crucial insights into leaders, laggards, and everything in between.

Go from risk-on to risk-off with ease and confidence. Subscribe to The Lead-Lag Report today.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Read the full article here