Shares of intracellular treatment concern Entrada Therapeutics, Inc. (NASDAQ:TRDA) are down significantly from their all-time high as a protracted hold on the two IND applications has tempered enthusiasm. Its two clinical assets (one out-licensed) are undergoing early-stage studies in the UK and Canada, data from which should assist in getting the FDA holds lifted. With a novel approach to treatment that should have applications beyond its rare neuromuscular disease indications, the recent insider buying into this busted IPO merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview

Entrada Therapeutics, Inc. is a Boston based clinical-stage biopharmaceutical concern focused on the development of endosomal escape vehicle [EEV] therapies to treat rare neuromuscular diseases. The company has two intracellular assets in the clinic, one of which is in a collaboration with Vertex Pharmaceuticals (VRTX). Entrada commenced operations in 2016 and went public in 2021, raising net proceeds of $190.7 million at $20 per share. Its stock trades just under $16.00 a share, translating to an approximate market cap of just over $500 million.

EEV Platform

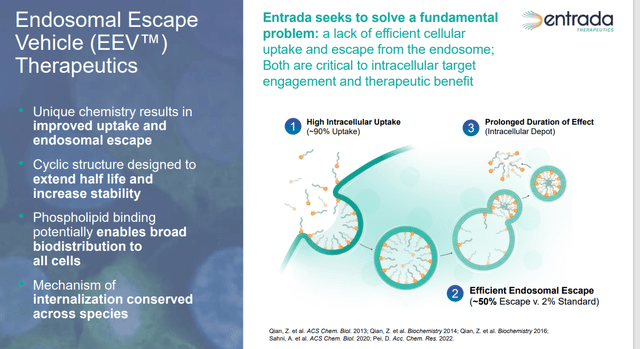

The company’s intracellular therapeutics are designed to target malady-inducing dysfunction inside cells, namely from DNA, RNA, or proteins, which are responsible for facilitation in approximately three-quarters of all diseases. For one of these treatments to be effective, it must penetrate the cell membrane and evade its transportation and sorting mechanism, known as the early endosome, in order to engage its intended target. Small molecule therapies can readily enter the cell, but are subject to rapid clearance by the body. This development necessitates higher dosing for better effectiveness, but often leads to off-site toxicity. Larger molecule biologic remedies are highly specific and potent once their targets are reached, but in many cases, they are unable to efficiently penetrate the cell membrane and/or escape the early endosome.

March 2024 Company Presentation

Entrada believes it has a solution with its EEV platform, which addresses the shortcomings of the aforementioned approaches by creating therapeutics that can reach their intracellular targets with high proficiency. The workaround is accomplished by conjugating endosome-escaping biologics to cell-penetrating peptides that target cell membrane’s phospholipid bilayers. Entrada believes these compounds can achieve entry into any cell in the body with a ~90% success rate, irrespective of administration route. Once inside the cell, approximately half the biologics reach their target, versus ~2% for their unconjugated counterparts; thus enabling more effective treatment of the dysfunction. This extremely high target engagement (therapeutic index) is due to the EEV therapeutic’s novel cyclic structure, which minimizes protease-mediated degradation, engendering a longer half-life. From this approach, which the company believes has both utility across multiple modalities (oligonucleotides, peptides, antibodies, etc.) and applications for many diseases, it has spawned two neuromuscular disease clinical assets.

Pipeline

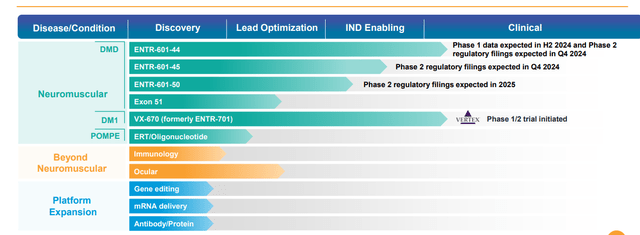

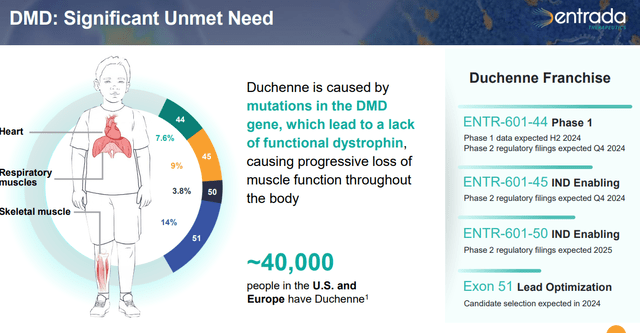

ENTR-601 Family. The company’s lead program is ENTR-601-44, which is an EEV linked to small strands of nucleic acids known as oligonucleotides – in this instance, phosphorodiamidate morpholino oligomers (PMOs) – to treat Duchene’s muscular dystrophy (DMD), a monogenic, X-linked disease caused by mutations that encode for the dystrophin protein. Essential for the structural integrity and function of muscle cells involved in walking, breathing, and cardiac function, dystrophin proteins are reduced or absent in DMD patients due to mutations in the dystrophin gene. Symptoms such as muscle weakness and wasting present in the first few years of life with most patients wheelchair-bound by their teenage years, followed by progression to respiratory and cardiac failure, with nearly all sufferers dead by the age of 30.

March 2024 Company Presentation

DMD afflicts ~12,000 to ~15,000 in the U.S. and ~25,000 in Europe. In addition to PTC Therapeutics’ (PTCT) corticosteroid Emflaza, there are four FDA-approved exon skipping therapies for this affliction. These remedies encourage the cellular machinery to skip over missing, faulty, or misaligned sections (exons) of genetic code, leading to truncated but functional proteins. Sarepta Therapeutics (SRPT) has developed three conditionally approved ‘patches’ that promote skipping of exons 45, 51, 53 of the dystrophin gene. Nippon Shinyaku (OTCPK:NPNKF) markets Viltepso (viltolarsen) for DMD amenable to exon 53 skipping. Additionally, Dyne Therapeutics (DYN) is advancing a Transferrin 1 receptor conjugated PMO for DMD amenable to exon 51 skipping (DYNE-251), while precision medicine concern Edgewise Therapeutics (EWTX) is assessing its oral allosteric (i.e., alteration through binding), myosin (motor protein) inhibitor, EDG-5506. They represent two of six biotechs clinically pursuing the DMD indication.

March 2024 Company Presentation

Returning to ENTR-601-44 – which promotes skipping exon 44 – it is being investigated in a Phase 1 study on ~40 healthy volunteers in the UK, with data from three dose cohorts anticipated in 2H24. The story in the U.S. is starkly different, where the FDA put a clinical hold on Entrada’s IND application in December 2022, requesting additional information on ENTR-601-44. That hold continues to the present day.

March 2024 Company Presentation

While working through that hold, Entrada has selected clinical candidates for DMD amenable to exon 45 and 50 skipping. It plans Phase 2 regulatory submissions (Clinical Trial Applications in the UK and INDs in the U.S.) for ENTR-601-44 and ENTR-601-45 in 4Q24, as well as ENTR-601-50 in 2025. These three DMD exon-skipping indications comprise ~20% of all cases. Furthermore, the company anticipates selecting a clinical candidate for ENTR-601-51 (14% of DMD cases) sometime in 2024.

VX-670. A similar story can be told regarding VX-670 (formerly ENTR-701), an EEV-based therapeutic that is being evaluated for the treatment of myotonic dystrophy type 1 (DM1), a monogenic, autosomal dominant disease characterized through a myriad of manifestations – including myotonia (difficulty relaxing muscles), muscle weakness, cardiac arrhythmias, fatigue, GI issues, cataracts, and cognitive impairment – resulting from damage to skeletal, cardiac, and smooth muscles. It is caused by an increase in the number of CTG triplet repeats found in the 3’ non-coding region of the DMPK gene. The number of repeats in healthy subjects is ~35 versus thousands in DM1 patients. The abnormal expansion of the gene forms hairpin loops that entrap the pre-mRNA in the nucleus, driving toxic activity known as a gain-of-function mutation. The toxic mRNA forms foci (RNA repeats) in the nucleus that bind to splicing proteins. With the splicing proteins unable to perform their role in translation, other mis-spliced proteins are created, causing the aforementioned presentations of DM1.

DM1 afflicts more than 40,000 in the U.S. and ~74,000 in Europe, with about two-thirds presenting symptoms between their early teens to 50 years of age. There are no approved therapies, although Dyne is pursuing this indication in a Phase 1/2 study evaluating its DMPK degrader (DYNE-101).

Returning to VX-670, it is undergoing evaluation in a Phase 1/2 trial in Canada (and in the UK shortly) that initiated in January 2024 but has yet to enter study in the U.S. as Vertex’s IND application is also under clinical hold pending the receipt and evaluation of additional information. Vertex did make a $75 million milestone payment to Entrada in March.

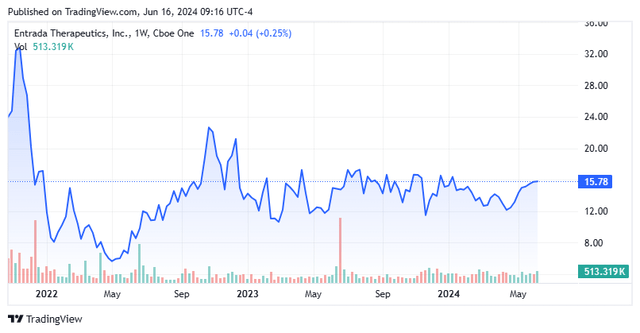

The holds are largely responsible for shares of TRDA falling substantially from its peak trade of $36.85, achieved shortly after its IPO in November 2021.

For VX-670, Vertex paid Entrada $250 million upfront, consisting of $223.7 million in cash and $26.3 million of TRDA shares at $16.26 per in December 2022, only weeks before ENTR-601-44’s application was placed on clinical hold. Entrada is also eligible to receive research, development, regulatory, and commercial milestones up to $485 million, as well as tiered royalties. To date, Vertex has paid out $92.5 million in milestones.

Balance Sheet & Analyst Commentary

Thanks in large measure to the Vertex agreement, Entrada’s coffers are well padded, reflecting cash and marketable securities of $327 million at the end of the first quarter, providing it an operating runway through at least mid-year 2026.

Despite its ongoing issues with the FDA, Street analysts are unanimously optimistic on the company’s prospects, featuring one outperform and three buy ratings, with price targets proffered between $20 to $22 a share.

Board member Peter Kim shares the Street’s outlook, having purchased 15,892 shares at an average price of $13.46 since mid-March 2024.

Verdict

It is abundantly clear that the reason for Entrada’s IPO being busted is the clinical holds on the INDs for ENTR-601-44 and VX-670. It would stand to reason that those holds will be lifted after initial data from ENTR-601-44 in healthy subjects are released in 2H24, assuming no surprises. Although there is substantial competition for the DMD indication, the novel EEV platform could spawn a new class of therapies, with many collaborators likely to line up if its proof-of-concept is clinically validated.

There isn’t much in the way of catalysts until the UK trial data in 2H24, but that could unlock significant value. There is still downside risk, but the upside via future collaborations makes the risk/reward profile significantly tilted to the upside. Trading at only a ~$175 million premium to cash, Entrada is worth a small roll of the dice only for long-term and aggressive investors.

Read the full article here