Elevator Pitch

I award a Hold rating to Infosys Limited (NYSE:INFY) stock.

I have a Neutral view of INFY. On the negative side of things, Infosys’ guidance for the new fiscal year is disappointing due to the unfavorable outlook for its key financial services segment. On the positive side of things, the company’s shift in project mix towards bigger deals has favorable read-throughs relating to customer confidence and demand for certain IT services.

Company Description

Infosys is one of “India’s largest IT services companies” alongside peers such as Tata Consultancy Services [TCS:IN] according to Indian media publication The Economic Times.

INFY’s Key Focus Areas

Infosys’ Investor Presentation Slides

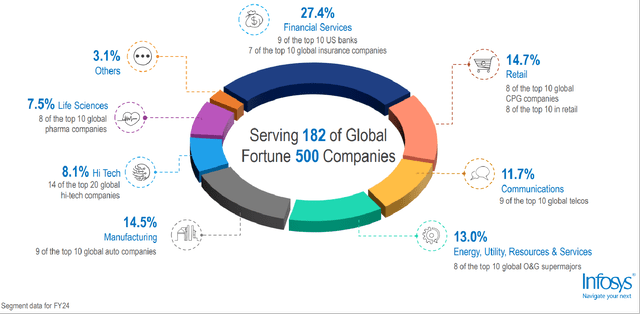

Infosys’ Client Mix BY Industry

Infosys’ Investor Presentation Slides

INFY derived 59.6% and 28.6% of its Q4 FY 2024 (YE March 31, 2024) top line from the North American and European markets, respectively, as disclosed in its corporate factsheet. India and other markets contributed the remaining 2.2% and 9.6% of the company’s latest quarterly revenue, respectively.

The company added 98 new customers in the most recent quarter to bring its total client count to 1,882 (source: corporate factsheet) as of March 31, 2024. In terms of client concentration, Infosys’ 25 biggest customers accounted for 34.3% of the company’s Q4 FY 2024 revenue.

Fiscal 2025 Top Line Growth Outlook Is Unexciting

INFY anticipates that the company’s revenue on a constant-currency basis will expand by a modest +2% in FY 2025 (April 1, 2024 to March 31, 2025) as per the mid-point of its guidance revealed in its FY 2024 earnings release.

Infosys’ top line growth outlook for the new fiscal year is unimpressive, taking into account industry projections and the company’s track record. In its investor presentation slides, INFY cited Gartner’s (IT) forecast of a +9.5% annualized growth in “global IT services spend” for the 2022-2027 time frame. As another comparison, the company’s historical FY 2014-2024 revenue CAGR in local currency or Indian rupee terms is +11.9% based on S&P Capital IQ data. In contrast, INFY’s expectations of a low-single digit percentage increase in its top line in this fiscal year are disappointing.

The weakness of INFY’s key financial services segment is most probably the main reason for the company’s lackluster FY 2025 guidance. In the preceding section, I have already highlighted that the financial services segment represented 27.4% of the company’s full-year FY 2024 top line, which made it the largest revenue contributor.

At its FY 2024 earnings briefing, Infosys noted that “high inflation as well as highest interest rates” have resulted in “cautious spend by clients” in the “BFSI” or Banking, Financial Services, and Insurance vertical.

Separately, Indian brokerage Antique Stock Broking issued a research report (not publicly available) titled “US Banking Results Commentary Indicates Cautionary Tech Investment” on May 30, 2024. US banks “remain conservative in investing in technology” as indicated in this Antique Stock Broking report. Also, Antique Stock Broking’s research suggests that the US banking sector’s technology spending-to-revenue ratio declined from 7.4% in the final quarter of calendar year 2023 to 6.5% for the first quarter of calendar year 2024.

Notably, INFY shared in its investor presentation slides that “9 of the top 10 US banks” are its customers. Therefore, it is realistic to expect Infosys to achieve a slow pace of top line expansion for the near future, considering the potential underperformance of its key financial services segment.

But Project Mix Has Become More Favorable With Bigger Deals

Infosys stressed at its fiscal 2024 earnings call that “we have a healthy pipeline of large and mega deals.” In specific terms, the company’s TCV or Total Contract Value for “large deals” rose significantly by +81% from $9.8 billion for FY 2023 to $17.7 billion (source: investor presentation slides) in FY 2024, which represented a new historical high.

The change in INFY’s project mix has positive read-throughs for the company’s medium-to-long term revenue growth prospects, notwithstanding its uninspiring FY 2025 top line guidance.

One factor is that a higher proportion of bigger deals are indicative of an increase in client confidence.

At the company’s FY 2024 analyst briefing, Infosys noted that deals of a bigger scale represent “very sticky businesses with the client and long-term commitments from the client.” As such, a growing percentage of bigger deals suggests that an increasing number of INFY’s customers have shown the willingness to sign contracts boasting a higher value and a longer duration with the company.

Another factor is that the shift in project mix towards bigger deals means that there is still decent demand in specific segments of the IT services industry.

Specifically, the majority of INFY’s bigger deals are comprised of projects focused on “cost efficiency and consolidation” as per the company’s disclosures at the FY 2024 analyst briefing. This implies that there will still be business opportunities for Infosys in a difficult economic environment, as some of INFY’s customers will place a greater emphasis on expense optimization IT initiatives when economic conditions are unfavorable.

In summary, bigger deals for INFY imply that client confidence in the company is growing and certain IT services relating to expense control and operating efficiency are still in demand.

Stock Is Fairly Valued

Infosys is now trading at 23.5 times consensus next twelve months’ normalized P/E (source: S&P Capital IQ) which I deem to be reasonably fair.

On one hand, INFY’s current P/E ratio is quite close to its historical five-year average consensus forward P/E multiple of 23.9 times as per S&P Capital IQ data.

On the other hand, the market values Infosys at a discount to its peer Tata Consultancy Services, but the latter has more attractive revenue growth prospects than the former.

Tata Consultancy Services shares are currently valued by the market at a relatively higher consensus next twelve months’ normalized P/E of 26.9 times.

It is worth noting that Tata Consultancy Services guided that “FY’25 should be better than FY’24” at its earnings call after achieving a +3.4% top line expansion on a constant-currency basis in FY 2024. In other words, Tata Consultancy Services’ actual FY 2025 revenue growth might be closer to a mid-single digit percentage level and superior to that of Infosys (+2% FY 2025 revenue growth guidance).

Closing Thoughts

The company’s shares are trading at a fair valuation, and there are mixed takeaways from its project mix disclosures and financial guidance. This explains why I have rated Infosys as a Hold.

Read the full article here